- LME prices close below $3,000/t

- Zinc futures drop 1.29% on MCX

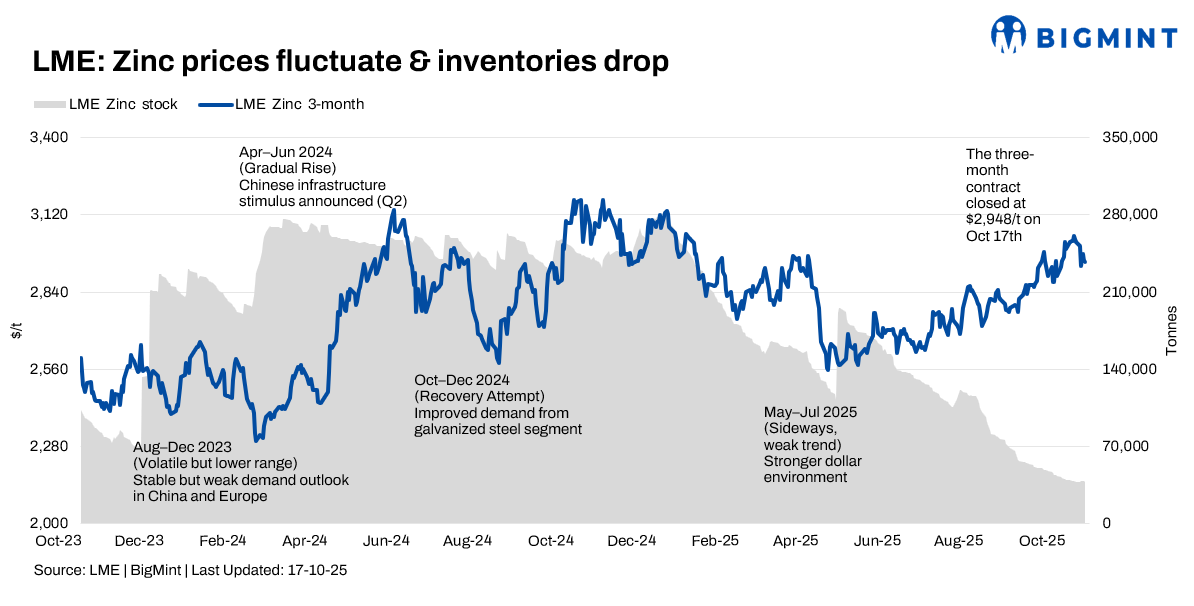

The London Metal Exchange (LME) zinc market experienced significant price volatility during Week 41 (13-17 October 2025), influenced by conflicting signals from geopolitical tensions, macroeconomic data, and inventory shifts. Prices fluctuated widely, ultimately closing the week lower despite strong early-week gains. The market navigated concerns over renewed US-China trade tensions and a historic stock drawdown in LME warehouses.

Price trends

LME zinc cash-settlement prices showed sharp fluctuations throughout the week. Prices opened higher at $3,119/t on 13 October, continuing the previous week’s upward momentum. However, they were hit by profit-booking and heightened concerns over renewed US-China trade tensions, dropping significantly mid-week. Prices closed lower at $3,100/t on 16 October and saw further pressure on 17 October, with one source noting a closing price of $2,941.40/t. This volatility reflects a mixed market sentiment, with prices initially pushing higher before being weighed down by profit-taking and macroeconomic fears.

Inventory analysis

LME zinc inventories continued their declining trend during the week, despite a small mid-week increase, reaching critically low levels and raising market concerns ahead of LME Week. On 16 October, LME zinc inventory increased by 50 t to 38,300 t. However, this small uptick occurred within the context of a historic stock drawdown, as inventories fell by 475 t to 37,475 t just before the start of the week and continued their long-term trend of declining globally. This indicates a tightening global supply of readily available zinc and provides a base of support for prices.

MCX zinc trends (13-17 October)

MCX zinc futures (October 2025 expiry) corrected 1.29% this week, from INR 294,250 (13 October close) to INR 290,450 (17 October close). Prices traded between INR 287,800 and INR 296,400. Volume and open interest fell, indicating profit booking. Market sentiment was mildly bearish, with resistance at INR 296,000 and support at INR 288,000/t. Technical indicators show overbought signals, suggesting a cautious approach as the uptrend momentum slows. The Indian market was influenced by global trends, including intensified US-China trade tensions, a slightly hawkish US Fed tone, and continued inventory drawdown.

SHFE zinc trend

SHFE zinc prices were influenced by the global market trend but also by domestic factors. The most-traded SHFE zinc contract for November (ZN2511) fluctuated during the week, closing up 0.27% at RMB 22,010/t on October 17th. Despite some fluctuations, concerns over tepid domestic demand and the overall supply-demand balance persisted, capping SHFE gains.

Outlook

The short-term outlook for zinc remains cautiously bearish, as global oversupply and macroeconomic headwinds offset support from low inventories. Prices may remain range-bound until demand recovery from the construction and galvanising sectors gains traction. Traders should watch for developments in US-China trade relations, LME Week announcements, and inventory movements for clearer market direction.

Leave a Reply