- 2-3 coking cargo bookings heard this week

- Domestic met coke tags remain stable w-o-w

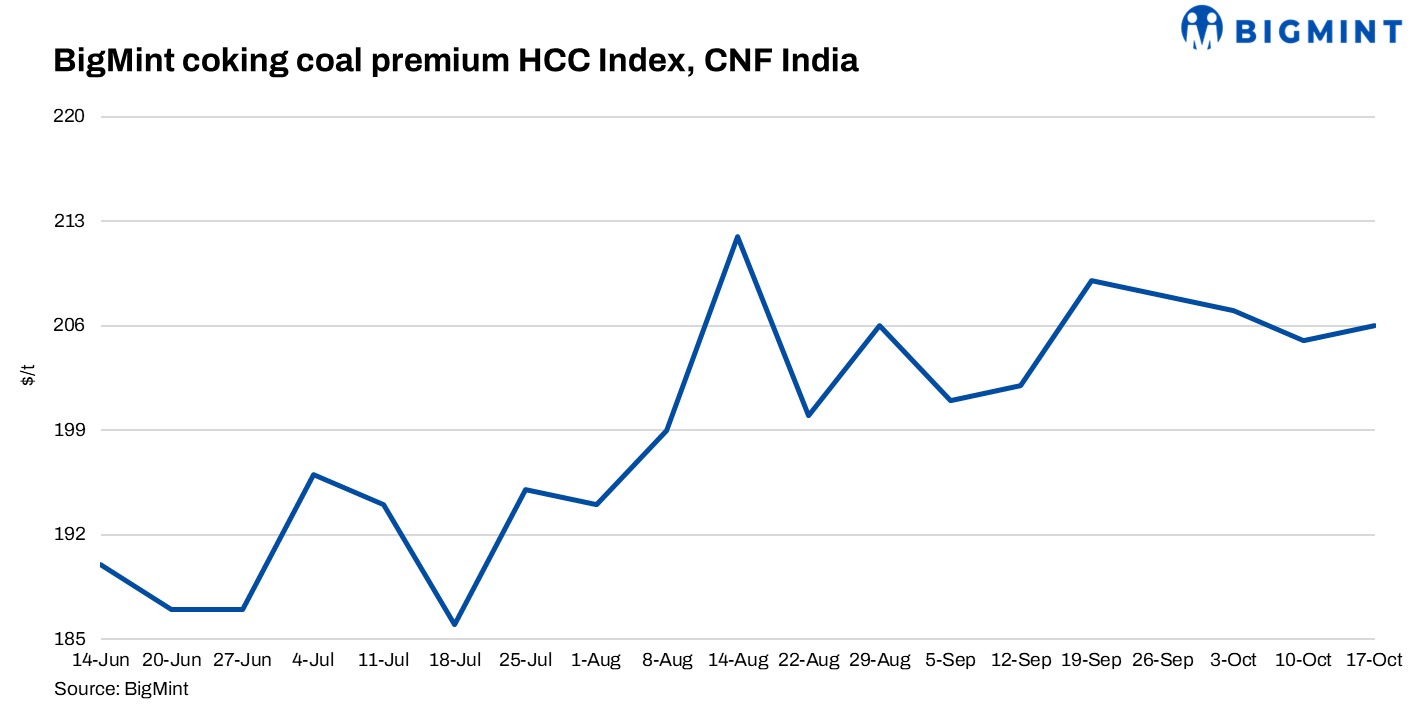

BigMint’s premium hard coking coal (PHCC) index was assessed at $206/tonne (t) CNF Paradip, India, on 17 October 2025, up by $1/t against the previous assessment on 10 October.

The market remained active with decent trade activities seen this week. A western India-based steel mill booked part of a 30,000-t cargo of Australian PHCC for November shipment at an index-linked basis, which will translate to around $206-207/t CFR India. In another deal, an eastern India-based mill booked 25,000 t of Australian cargo at $203/t CFR India. However, the deal could not be confirmed at the time of publishing this report.

Rationale

BigMint’s coking coal index is derived using data points, i.e., trades, offers, bids, and indicative prices.

One deal was heard concluded. Hence, it was considered for index computation and given a weightage of 50%.

Ten (10) firm offers, bids, and indicative prices were heard. Out of these, nine (9) were considered for price calculation and given 50% weightage.

BigMint has consolidated its Prime Hard Coking Coal (PHCC) CFR India Index to include material of all origins, including US, Canada, Mozambique, Australia – normalised for quality and freight. With India steadily reducing its reliance on Australian PHCC and increasing imports from alternative sources, this update ensures the index accurately reflects evolving market dynamics and trade flows.

Factors impacting imported coking coal prices

1. Indian met coke prices hold firm w-o-w: India’s metallurgical coke (met coke) market stayed largely stable w-o-w during the week ending 16 October 2025, with limited buying activity observed ahead of the festive holidays. In eastern India, BF-grade (25-90 mm) met coke was assessed at INR 29,900/t ex-Jajpur, while in western India, ex-works Gandhidham tags hovered at INR 30,000/t. Market sentiment remained steady but cautious, as industrial activity slowed due to the upcoming festive period. Domestic prices showed no significant movement compared to last week.

2. Chinese met coke prices remain stable: China’s metallurgical coke market remained balanced, with tightened supplies offset by weak steel demand. Production curtailments of around 30% in Tangshan, driven by stricter environmental controls, slightly constrained high-quality coke availability.

3. India BF-rebar trade prices drop by INR 200/t ($2/t) w-o-w: India’s trade-level blast furnace (BF) rebar prices declined on a w-o-w basis across major markets. Major primary mills either offered discounts or reduced list prices this week amid subdued market sentiment. Buying activity remained weak across regions ahead of the festive season. Trade-level BF rebar prices edged down by INR 200/t ($2/t) w-o-w to INR 46,900/t ($533/t) exy-Mumbai, as per BigMint’s assessment on 17 October 2025. Prices are exclusive of GST at 18%.

Leave a Reply