- Global oversupply, US-China trade tensions weigh on market

- India launches Mumbai-Pune electric corridor boosting EV adoption

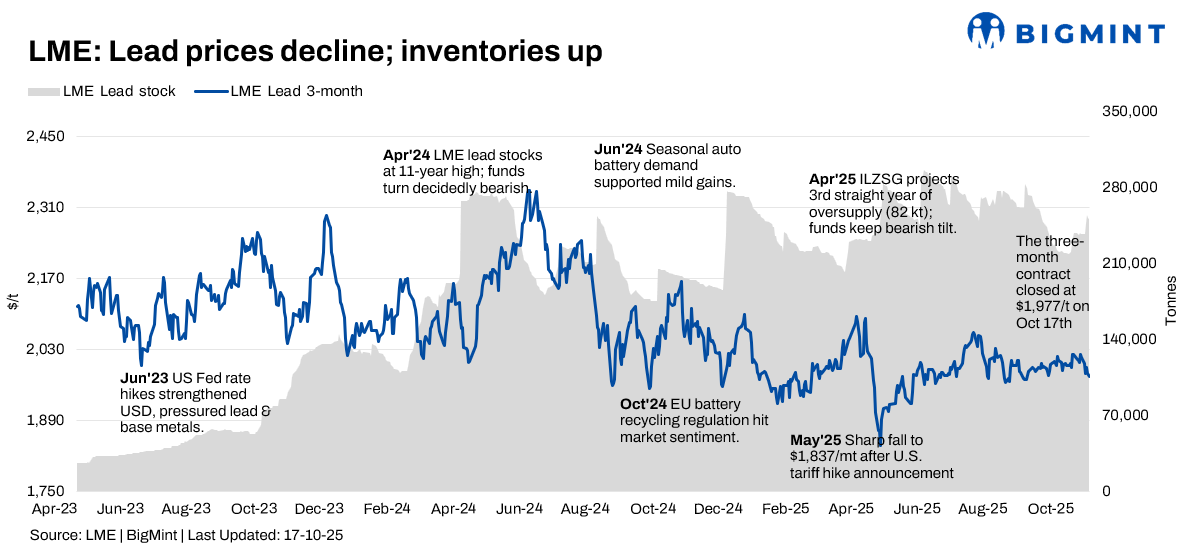

The London Metal Exchange (LME) market experienced a volatile and downward week (October 13-17, 2025), largely driven by negative macroeconomic sentiment and heightened geopolitical tensions. Despite a brief rally earlier in the week, prices were consistently under pressure amid potential US-China trade escalation and weak US economic signals.

Price, inventory trends

LME lead cash-settlement prices opened at $1,956.50/t on 13 October, down to to $1,940/t on 14 October, and closed at $1,971.5/t on 16 October, down $14.5/t (0.73%). The three-month contract also declined to $1,971.5/t, reflecting bearish sentiment. LME inventories rose from 237,000 t to 252,000 t over the week, signaling supply is not as tight as previously perceived. Chinese social inventories showed regional declines but generally sufficient spot supply.

MCX lead trends (13-17 October)

MCX Lead futures (October 2025 contract) closed lower at INR 177,200/t on 17 October, reflecting global weakness. Prices traded between INR 177,00-180,000/t during the week. Profit-booking was observed amid global cues, while domestic supply-demand dynamics and the rupee influenced price stability.

SHFE lead weekly update

SHFE lead prices mirrored global trends, closing at 17,045 yuan/t on 17 October (most-traded 2511 contract). Despite minor regional supply tightening, weak domestic demand and oversupply concerns capped gains, keeping prices under pressure throughout the week.

India’s first electric highway

Maharashtra CM Devendra Fadnavis inaugurated India’s first electric corridor on the Mumbai-Pune highway, enabling seamless EV travel. The launch featured an electric heavy-duty truck by Blue Energy Motors with battery-swapping technology at Chakan. Maharashtra plans to expand similar corridors across major national highways over the next three years, advancing India’s clean mobility ambitions.

Outlook

The lead market is likely to remain cautiously bearish in the near term due to global oversupply, weak US macro signals, and trade tensions. Prices may find support from domestic demand and regional inventory tightness, while EV adoption and sustainable battery initiatives provide long-term structural support.

Leave a Reply