- IF rebar prices drop in the range of INR 100-900/t w-o-w

- HRC, CRC trade prices trend down amid festive slowdown

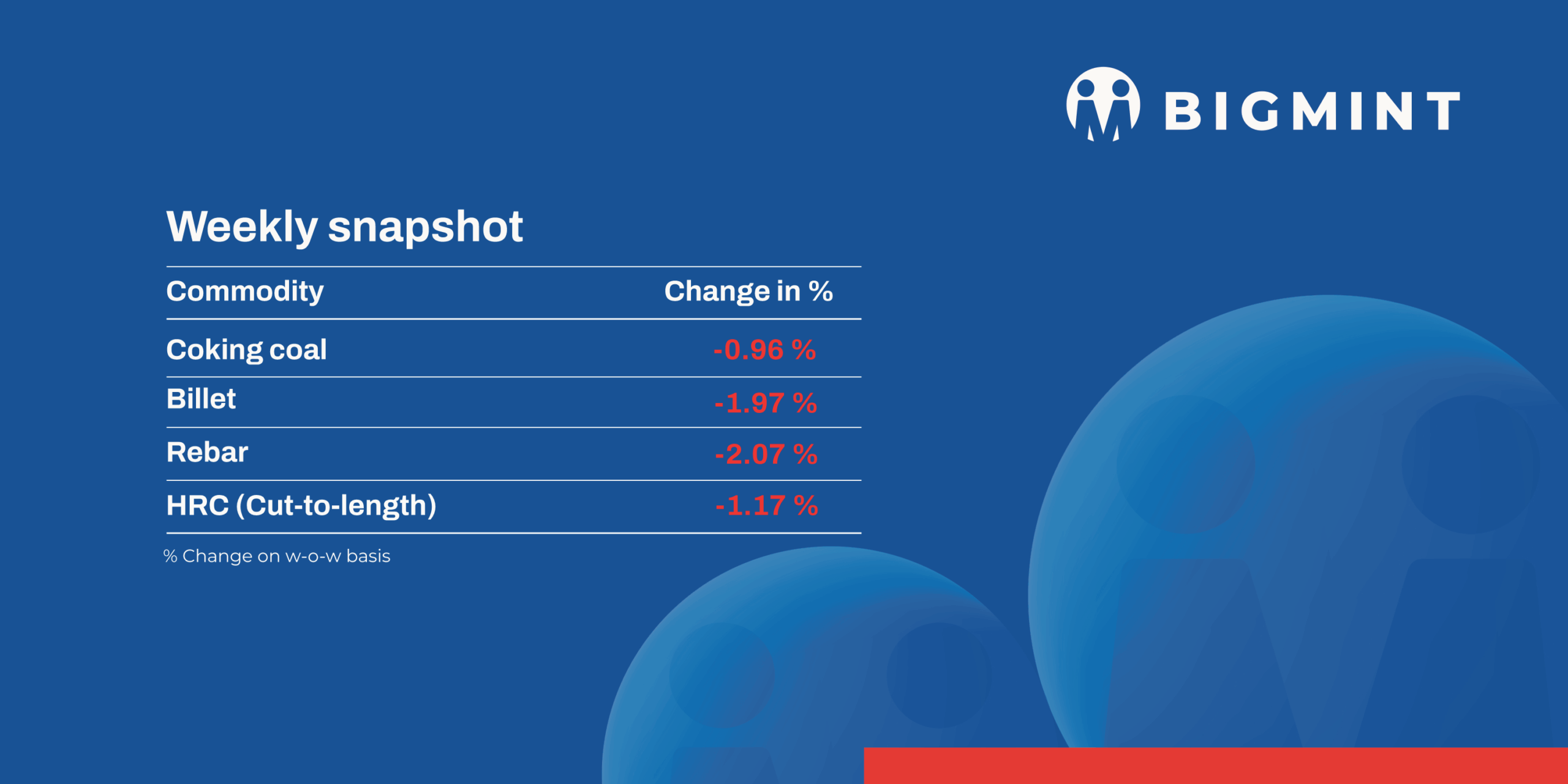

The domestic steel market saw mixed trends during week 42 (13 – 17 October 2025). Iron ore and pellet prices remained firm w-o-w amid tight supply, while the semi-finished and long steel segments remained under pressure due to weak demand and festive slowdown. Flat steel prices were largely stable.

Iron ore & pellet

In OMC’s 17 October auction, 1.82 mnt (97%) of 1.871 mnt iron ore fines (Fe 51–62%) were booked at INR 2,500–5,700/t, with bids up INR 50/t m-o-m amid tight supply and low output due to extended monsoons. In the lumps auction (0.954 mnt, Fe 60–65%), all lots were sold at INR 5,450–7,750/t, fetching premiums of INR 550–2,550/t. Despite a base price cut of INR 550/t m-o-m, bids remained firm on supply constraints even as steel prices fell.

BigMint’s bi-weekly export index for Indian low-grade iron ore fines (Fe 57%) rose by $2/t w-o-w to $71/t FOB east coast as of 16 October , an eight-month high. Around 450,000 t of fines were traded recently, with Odisha-based miners securing premiums on Fe 57% cargoes amid tight supply and steady demand.

BigMint’s India pellet (Fe 63%, 3–3.5% Al) export index increased by $2.5/t w-o-w to $106/t FOB east coast on 15 October, supported by active Chinese demand and limited supply. Indian producers sold 200,000 t of Fe 62/64% pellets, with one deal heard at $119/t CFR China for end-October loading. The market stayed firm after the Chinese holiday but softened slightly as global sentiment weakened with falling Chinese iron ore indices.

Coal

South African portside coal offers in India remained steady this week, with RB2 assessed at INR 8,200/t and RB3 at INR 7,100/t across Paradip, Vizag, and Gangavaram. Portside thermal coal inventories increased 9% w-o-w to 13.26 mnt in week 41, up from 12.22 mnt in week 40, as vessel arrivals improved and stock inflows strengthened at major east coast ports.

India’s metallurgical coke (met coke) market stayed largely stable w-o-w during the week ending 16 October 2025, with limited buying activity observed ahead of the festive holidays. Imported met coke (low-phosporous) of Colombian origin was indicated as stable w-o-w at $265-275/t CFR India this week, with a deal for nearly 40,000 t heard. China’s metallurgical coke market remained balanced, with tightened supplies offset by weak steel demand.

BigMint’s premium hard coking coal (PHCC) index was assessed at $206/tonne (t) CNF Paradip, India, on 17 October, up by $1/t w-o-w. The market remained active with decent trade activities seen this week.

Ferrous scrap

India’s imported scrap market remained under pressure through the week as weak steel demand and tight liquidity curbed buying interest. Ahead of Diwali, trading slowed further as mills focused on managing cash flow and reducing costs. Prices stayed stable but low, reflecting quiet market conditions, with recovery unlikely until post-festival demand improves.

Imported scrap prices to India were reported at $355/t for shredded, $325/t for HMS 80:20 with most bids at least $5-10/t below offers.

In the last seven days, around 2,500 t of imported scrap were booked, including 1,500 t of HMS 80:20 at $315-320/t, while the rest comprised HMS 90:10, and turning scrap.

Ferro alloys

Silico manganese

Indian silico manganese (60-14) prices rose by INR 700/t ($8/t) w-o-w to INR 71,100–71,600/t ($808-814/t) in Durgapur, Raipur, and Vizag, driven by higher domestic steel mill procurement amid rising manganese ore and coke costs, and pre-festive inventory buildup to avoid supply disruptions.

Ferro manganese

Indian ferro manganese (HC 70%) prices rose slightly by INR 400/t ($4/t) w-o-w to INR 71,300/t ($811/t) exw-Durgapur. Meanwhile, exw-Raipur prices inched up by INR 300/t ($3/t) to INR 71,300/t ($811t). Prices remained largely stable on regular trades, with minor gains amid material shortages.

Ferro silicon

Indian ferro silicon (Si 70%) prices increased by INR 1,700/t ($19/t) w-o-w to INR 88,700/t ($1,009/t) exw-Guwahati, while Bhutan prices rose by INR 1,500/t ($17/t) to INR 88,500/t ($1,006/t), supported by steady export demand, prolonged rains in Bhutan, and slightly tight supply due to SAIL tender commitments.

Ferro chrome

Indian high-carbon ferro chrome (HC 60%, Si 4%) prices remained steady w-o-w at INR 120,400/t ($1,369/t) exw-Jajpur. Prices stayed firm at elevated levels following higher bids in the Vedanta-FACOR auction, as sellers maintained strong offers, while buyers remained cautious.

Meanwhile, at OMC’s chrome ore auction held yesterday, 83,100 t was sold out of the 86,400 t offered. Bids rose by 0.4–18% (INR 40–5,550/t) for most grades, while a few gardes declined by 8–10% (INR 1,894–2,764/t) m-o-m. Additionally, OMC has scheduled a HC ferro chrome auction on 23 Oct’25 for 3,200 t of material, with the base price for the larger lot (Cr: 60–64%, 10–100 mm) set at INR 120,400/t ($1,369/t) exw.

Semi-finished steel

Indian semi-finished steel prices extended declines this week, as per BigMint’s assessment. Domestic billet prices across markets fell by INR 300-1,000/t ($3-11/t) w-o-w, with the sharpest declines of INR 750-1,000/t ($8.5-11/t) recorded in Raipur, Raigarh, and Durgapur. The persistent weakness in demand and limited offtake in both semi-finished and finished steel segments weighed on spot prices, prompting significant corrections across regions.

Sponge iron prices also dropped by INR 400-800/t ($4.5-9/t) across key producing regions as sellers reduced offers to conclude deals amid weaker enquiries. With the upcoming festive holidays, buying activity has slowed considerably, as dispatches and transportation are expected to face disruptions due to reduced manpower availability.

Indian DRI (Direct Reduced Iron) export offers dropped further by $3-5/t to $320/t CPT Raxaul and $326/t CPT Benapole. Export enquiries from Nepal and Bangladesh remained muted, reflecting a broader slowdown in trading activity ahead of the festive holidays.

Finished long steel

IF-rebar: India’s Induction Furnace (IF) route rebar market witnessed a downtrend this week as trading activity slowed ahead of the upcoming Diwali festival. Transactions were concluded at lower price levels, reflecting cautious buying behaviour and need-based purchases resulting in subdued market sentiment across regions. Industry participants are expecting market sentiment to turn slightly positive post-Diwali, supported by the resumption of construction projects and an anticipated recovery in buying interest.

On a weekly basis, rebar prices witnessed a declined in the range of INR 100-900/t across regions, as per BigMint assessment.

The trade reference price of Fe 500 grade rebar manufactured via the IF route for 10-25 mm size was assessed at INR 37,600-38,000/t exw Raipur, INR 42,000-42,600/t exw Jalna.

Trade reference price of heavy structural steel for base size 150mm channel stands at INR 39,800-40,200/t exw Raipur.

Trade reference prices of wire rod are hovering at INR 37,500-38,000/t ex Raipur.

BF-rebar: India’s trade-level blast furnace (BF) rebar prices declined w-o-w across markets. The major primary mills either offered discounts or reduced list prices this week amid subdued market sentiment. Buying activity remained weak across regions ahead of the festive season.

Trade-level BF rebar prices edged down by INR 200/t ($2/t) w-o-w to INR 46,900/t ($533/t) exy-Mumbai, as per BigMint’s assessment on 17 October. Prices are exclusive of GST at 18%.

In the projects segment, prices remained in the range of INR 46,000-47,000/t ($523-535/t) FOR Mumbai. Market activity stayed subdued as buyers continued to adopt a wait-and-watch approach.

Flat steel

Trade-level prices of hot-rolled coils (HRCs) in India showed a downtrend w-o-w to reach INR 47,000-49,500/t ($529-557/t). Additionally, cold-rolled coil (CRC) prices fell w-o-w, with prices ranging between INR 53,300-57,800/t ($600-651/t).

The domestic trade market remained slow because demand is weak and the festive season has added to the slowdown. Moreover, market participants believe that activity will pick up after the festivals this week.

India’s bulk imports of HRCs touched 149,540 t as of 11 October, based on vessel line-up data. Around 174,813 t of additional cargoes are expected by the end-October. India’s bulk exports of HRCs touched 233,982 t as of 11 October.

BigMint’s Indian hot-rolled coil (HRC, S275) export index for Europe held steady w-o-w at $545/t FOB main port, with trading activity subdued and no significant discussions underway, likely due to the EU’s Carbon Border Adjustment Mechanism (CBAM). The India HRC (SAE 1006) export index for the Middle East and Vietnam remained stable w-o-w. Notably, “Middle East customers are likely to maintain minimal inventory levels as they approach the close of their financial year (FY) in December,” as per sources.

Leave a Reply