- Billet, sponge iron prices rise INR 1,000-3,000/t w-o-w on cost push

- Scrap trade weak amid high freights, coal and petcoke prices remain firm

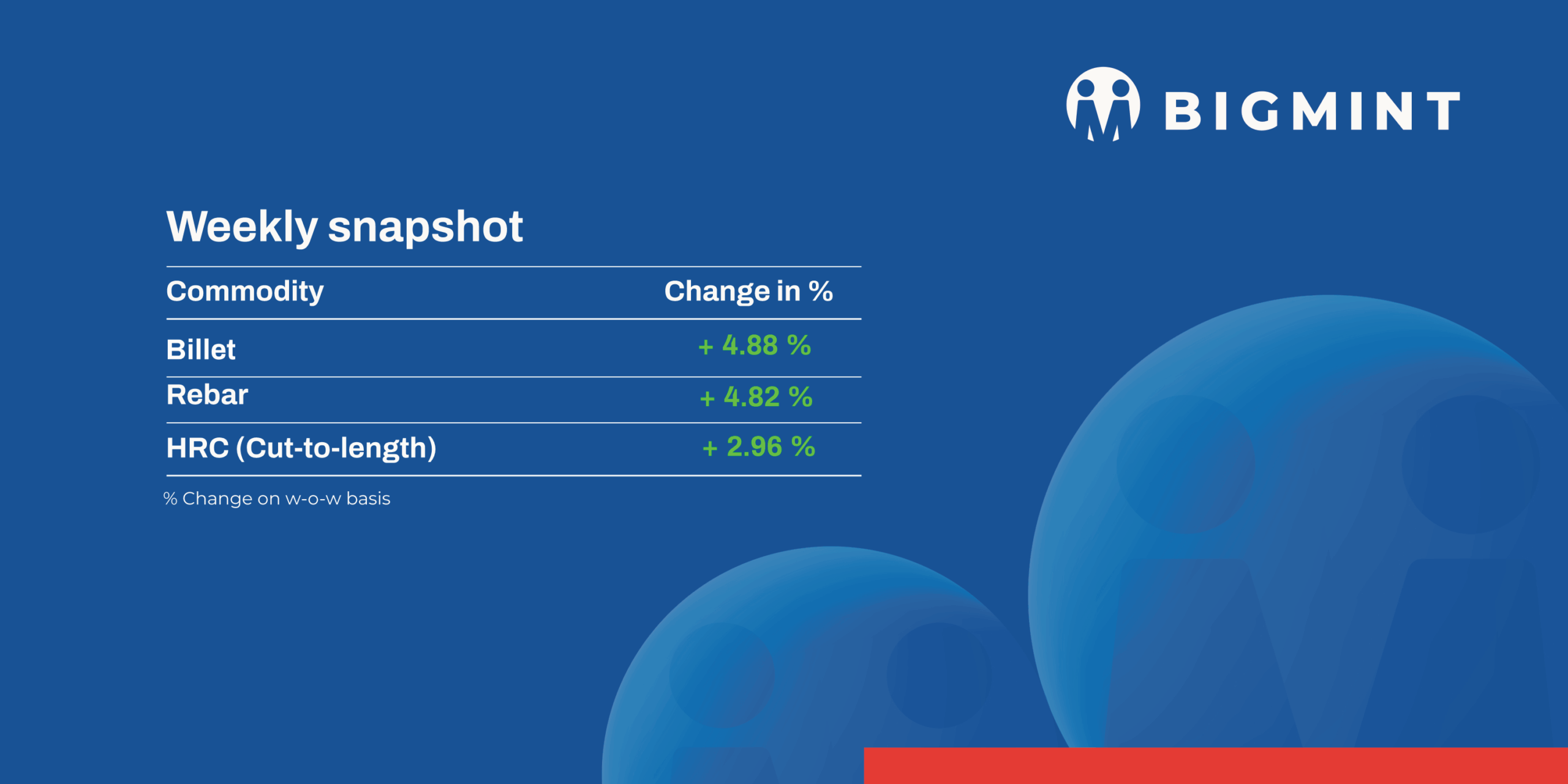

The domestic steel and raw materials market strengthened in the week ended 4 April, supported by rising input costs and improved order bookings. Semis and finished steel prices moved higher, while trading activity remained cautious due to elevated prices, freight volatility, and ongoing geopolitical uncertainties.

Iron ore and pellet

Odisha-based iron ore auctions witnessed moderate participation, with around 95,700 t booked out of the 328,900 t offered. Among key transactions, AM/NS on 30 March 2026, sold 40,000 t of lumps (5–18 mm, Fe 60.5%) at INR 6,850/t, 8,000 t of low TI CLO (10–40 mm, Fe 58.58%) at INR 4,125/t, and 12,000 t of lumps (10–40 mm, Fe 59%) at INR 4,300/t from Sagasahi and Thakurani mines. Meanwhile, JSW secured 23,700 t of CLO (5–18 mm, Fe 63%) at INR 7,900/t on 28 March, while SAIL-Bolani booked 12,000 t of CLO (10–40 mm, Fe 61%) at INR 6,650/t, inclusive of royalty, on 30 March 2026.

BigMint’s India pellet export index rose by around $1.5/t w-o-w to $101.5/t FOB east coast, supported by the largely stable global iron ore fines benchmark. Meanwhile, a temporary easing in freight rates along with improved vessel availability helped revive buyer interest, pushing up CFR levels. Despite these supportive factors, overall market sentiment remained cautious, with no confirmed export deals reported over the past couple of weeks.

PELLEX, BigMint’s bi-weekly domestic pellet (Fe 63%) index for Raipur, stood at around INR 10,650/t DAP on 3 April, dipping by INR 150/t ($2/t) w-o-w. Offers for Fe 62.5-63% (+/-0.5%) grade pellets were heard in the range of INR 10,500-10,600/t exw Raipur with 75,000 t deals concluded.

Coal

South African thermal coal prices declined sharply w-o-w, with RB2 (5,500 NAR) down by INR 350/t to INR 11,200/t and RB3 falling by INR 250/t to INR 10,200/t. The drop was driven by weak demand during FY-end, rising portside inventories (up 5.8% to 13.10 mnt), and fresh cargo arrivals. Buyers remained inactive amid weak sponge iron demand, while sellers lowered offers to clear stocks. However, firm seaborne offers may support prices if demand recovers.

Domestic thermal coal prices increased w-o-w, with 5,000 GCV rising by INR 200/t to INR 6,600/t and 4,500 GCV up by INR 50/t to INR 5,200/t. The increase was supported by shifting interest shown by cement-makers for domestic coal in auctions along with sponge iron and industrial users. Additionally, imported coal prices were elevated due to geopolitical tensions supporting price levels despite cautious market sentiment.

US NAPP coal prices remained firm in India, with ex-port levels at INR 17,000-18,000/t, supported by tight availability and limited cargo inflows. Stocks at Kandla are largely exhausted, while supply pipelines remain thin compared to last year. Freight costs have increased sharply due to bunker fuel shortages and vessel delays, raising delivered costs. Despite firm pricing, buying remains selective, although demand for high-CV coal continues due to its better calorific efficiency.

Domestic metallurgical coke prices remained largely stable, with BF-grade coke at INR 36,000/t ex-Jajpur and INR 31,000/t ex-Gandhidham. Foundry-grade prices rose slightly to INR 36,200/t. The market remained balanced but cautious, supported by firm import parity (around $290/t CFR) and rising coking coal costs (~$237/t FOB Australia). While pig iron prices improved sharply, overall downstream demand remained inconsistent, limiting strong upward movement in coke prices.

Imported petcoke prices surged to $160-170/t CFR India in March-early April, driven by supply disruptions and higher freight amid geopolitical tensions. However, buying activity remained weak as cement players resisted higher prices and shifted toward coal, which is cheaper by $10–15/t. India’s imports dropped 33% m-o-m to 0.6 mnt, reflecting cautious procurement. Meanwhile, Nayara raised prices sharply to INR 18,670/t (+INR 1,630), supported by tight domestic supply and strong cost pressures.

Ferrous scrap

Imported scrap prices remained weak through the week as the rupee depreciated to around INR 95/$ and higher freight rates pushed up landed costs to an 18-month high making imports largely unviable. Offers stayed firm, with HMS 80:20 around $380/t CFR and shredded near $390-400/t, but buying interest was limited, widening the bid-offer gap.

Prices were supported by tight vessel availability, global scrap shortages, and rising freight amid geopolitical tensions, though most offers from the UK, Europe, and other origins remained unworkable. The shredded-HMS spread also widened to $25-30/t, reflecting stronger sentiment in higher-grade scrap.

Around 2,500-3,000 t of imported scrap was booked during the week, including Senegal-origin HMS 80:20 at $375/t CFR Mundra, LMS bundles at $320-330/t, and Costa Rica-origin HMS 60:40 at $350-353/t CFR Chennai, indicating steady buying across grades.

Ferro alloys

Silico Manganese

Indian silico manganese (60-14) prices surged by INR 10,950/t ($118/t) w-o-w to INR 84,500 -86,600/t ($908-930/t) across Durgapur, Raipur, Vizag, and Raigarh. Amid persistent market volatility and surging manganese ore prices, rising imports and rupee depreciation have elevated smelter costs, reinforcing stronger alloy pricing trends. Meanwhile, HC 65-16 silico manganese prices sharply rose by $48/t to $979/t FOB Vizag/Haldia.

Additionally, state-owned MOIL Limited has raised manganese ore prices sharply, effective 1 April. This marks the highest increase in two years. Prices of ferro grades with over 44% Mn content have been increased by 15%, while grades below 44% saw a 17.5% hike. Within the SMGR segment, prices of Mn 30%, Mn 25%, fines, and chemical grades were also raised by 17.5%.

Ferro Manganese

Indian ferro manganese (70%) prices rose w-o-w by INR 10,000/t ($108/t) to INR 82,500/t ($886/t) in Durgapur while increasing by INR 9,300/t ($100/t) to INR 81,700/t ($802/t) in Raipur. Supply tightness, strong domestic demand, higher production costs, limited inventories, and improved export realizations supported the continued rise in prices. Meanwhile, export prices for 75 grade saw a sharp increase by $39/t w-o-w to $979/t FOB Vizag/Haldia.

Ferro Silicon

Indian ferro silicon (Si 70%) prices were mostly stable with a slight rise by INR 3,000/t ($32/t) w-o-w to INR 106,000/t ($1,138/t) exw Guwahati, while Bhutan prices also edged up by INR 2,600/t ($28/t) at INR 106,000/t ($1,138/t).Ferro silicon offers from Bhutan for April have been announced at INR 106,000/t ($1,138/t) exw, up by INR 6,000/t ($64/t) m-o-m. The increase is likely due to recent hike in power tariffs, tight spot availability, and rising logistics costs. Indian sellers, particularly in the northeast, are expected to align with the revised offer levels.

Ferro Chrome

Indian high-carbon ferro chrome (HC 60%, Si 4%) prices dipped slightly by INR 800/t ($9/t) to INR 117,000/t ($1,257/t) exw Jajpur. Prices fell as domestic demand was limited, and sellers mainly focused on export orders.

Semi-finished steel

India’s semi-finished steel market witnessed a notable uptick last week. Domestic billet prices surged by INR 1,000-3,000/t ($11-32/t) w-o-w across key regions, supported by raw material tightness and improved regional demand. However, buyers remained cautious, as elevated offer levels are yet to gain full acceptance. Meanwhile, producers were compelled to raise spot offers following a sharp rise in input costs in recent weeks.

The sponge iron market also recorded a significant increase across major regions. Pan-India DRI prices rose by INR 1,000-2,000/t ($11-21/t) w-o-w, influenced by geopolitical tensions and tightening raw material availability, which pushed sellers to hike offers. Despite the uptrend, buying activity remained moderate, with market participants adopting a cautious approach and seeking more favourable price levels before committing to bulk bookings.

On the export front, DRI offers increased sharply this week, even as overseas demand remained limited. Export offers to Nepal rose by $14/t w-o-w to $346/t CPT Raxaul, while offers to Bangladesh surged by $20/t to $359/t CPT Benapole. The rise was primarily due to sharp increase in domestic sponge iron prices, which in turn, restrained buying interest from overseas buyers.

NMDC’s Nagarnar Steel Plant auctioned 3,000 t of steel-grade pig iron on 30 March, with the entire quantity getting booked at an average price of INR 36,950/t. Bids increased by INR 1,350/t from the 26 March auction, when 7,200 t was sold out of 9,600 t at INR 35,600/t. The outcome reflects strong buying interest and a clear strengthening in market sentiment.

SAIL’s Rourkela Steel Plant (RSP) auctioned 2,200 t of steel-grade pig iron on 31 March, with the entire quantity sold at an average price of INR 39,850/t exw. Bids increased by INR 1,650/t compared with the 6 March auction, where 2,200 t were booked at an average price of INR 38,200/t exw.

SAIL-BSL Bokaro conducted a steel-grade pig iron auction on 1 April, offering 3,500 t, with the entire quantity being booked at an average price of INR 38,350/t. Prices increased by INR 2,800/t compared to the 25 March auction, where 7,000 t were sold at INR 35,550/t, reflecting improved market sentiment and firmer demand conditions.

Finished long steel

IF-rebar: IF rebar trade prices increased across major markets this week, supported by firm fundamentals. Early in the week, prices moved up as manufacturers revised gauge parity, driven by raw material shortages particularly scrap and sponge iron amid ongoing geopolitical tensions. Strong order bookings further reinforced the upward momentum.

However, as the week progressed, trading activity shifted to largely need-based buying due to elevated price levels and cautious market sentiment. Mills continued to prioritise dispatches, while inventory levels remained controlled at around 8–12 days.

In the near term, the market outlook remains supportive, with no significant pressure on mills. Prices are expected to stay on the higher side in the coming weeks. On a w-o-w basis, rebar prices increased by INR 1,300-3,100/t across key regions.

Trade reference prices of Fe 500 grade rebars manufactured via the IF route (10-25 mm size) were assessed at INR 53,800-54,300/t exw Jalna , INR 47,600-48,000/t exw Raipur.

Trade reference prices of heavy structural steel for the base size 150 mm channel stood at INR 48,500-49,000/t exw-Raipur. Trade reference prices of wire rod stood at INR 47,000-47,700/t ex-Raipur.

BF-rebar: Indian primary steelmakers increased rebar list prices by up to INR 2,000/t ($22/t) for early April from end-March levels, sources informed BigMint. Post-revision, list prices stood at INR 60,000-61,000/t ($647-658/t) on landed basis.

Trade-level BF-rebar prices (distributor to dealer) rose by INR 600/t ($6/t) w-o-w to INR 60,600/t ($654/t) exy-Mumbai, as per BigMint’s assessment on 3 April.

Rebar inventories at primary mills dropped by 20-25% m-o-m in early-April. The reduction in inventory was due to strong lifting of previously booked materials last month. Mills reported healthy order bookings last month and continue to focus on fulfilling pending project-linked orders, according to sources.

Flat steel

Trade-level prices of hot-rolled coils (HRC) in India strengthened across regions, touching a 3-year peak, with HRC prices assessed in the range of INR 55,500-59,600/t ($591-635/t) and cold-rolled coil (CRC) prices assessed at INR 59,800-67,000/t ($637-714/t).

BigMint’s bi-weekly benchmark assessment for HRC (IS2062, Gr E250, 2.5-8 mm/CTL) rose by INR 2,000/t ($21/t) w-o-w to INR 59,500/t ($634/t) as of 31 March, compared to INR 57,500/t ($613/t) on 24 March, likewise, CRC (IS513, Gr O, 0.9 mm/CTL) prices were assessed at INR 67,000/t ($713/t) on 31 March 2026, marking a w-o-w increase of INR 2,000/t ($21/t) from INR 65,000/t ($692/t) on 24 March.

India’s trade level HRC prices surged to 3-year high amid tight supply, while bullish sentiment, geopolitical tensions and inventory buildup supported sharp weekly gains and expectations of further upside.

India’s bulk imports of HRCs touched 183,326 t as on 27 March. Around 2,08,601 t of additional cargoes are expected.

India’s bulk exports of HRCs touched 156,394 t as on 27 March. Around 15,500 t of additional cargoes are expected.

Indian hot-rolled coil (HRC) export activity remained subdued during 24-31 March across key overseas markets, as escalating geopolitical tensions continued to disrupt major shipping corridors.

Market participants have adopted a cautious stance, with no firm offers reported during the week. Elevated freight-related uncertainty, coupled with limited near-term visibility and persistent logistical challenges.

Leave a Reply