- Prices recover mid-week, stocks continue downtrend

- MCX lead trades volatile, closes lower w-o-w

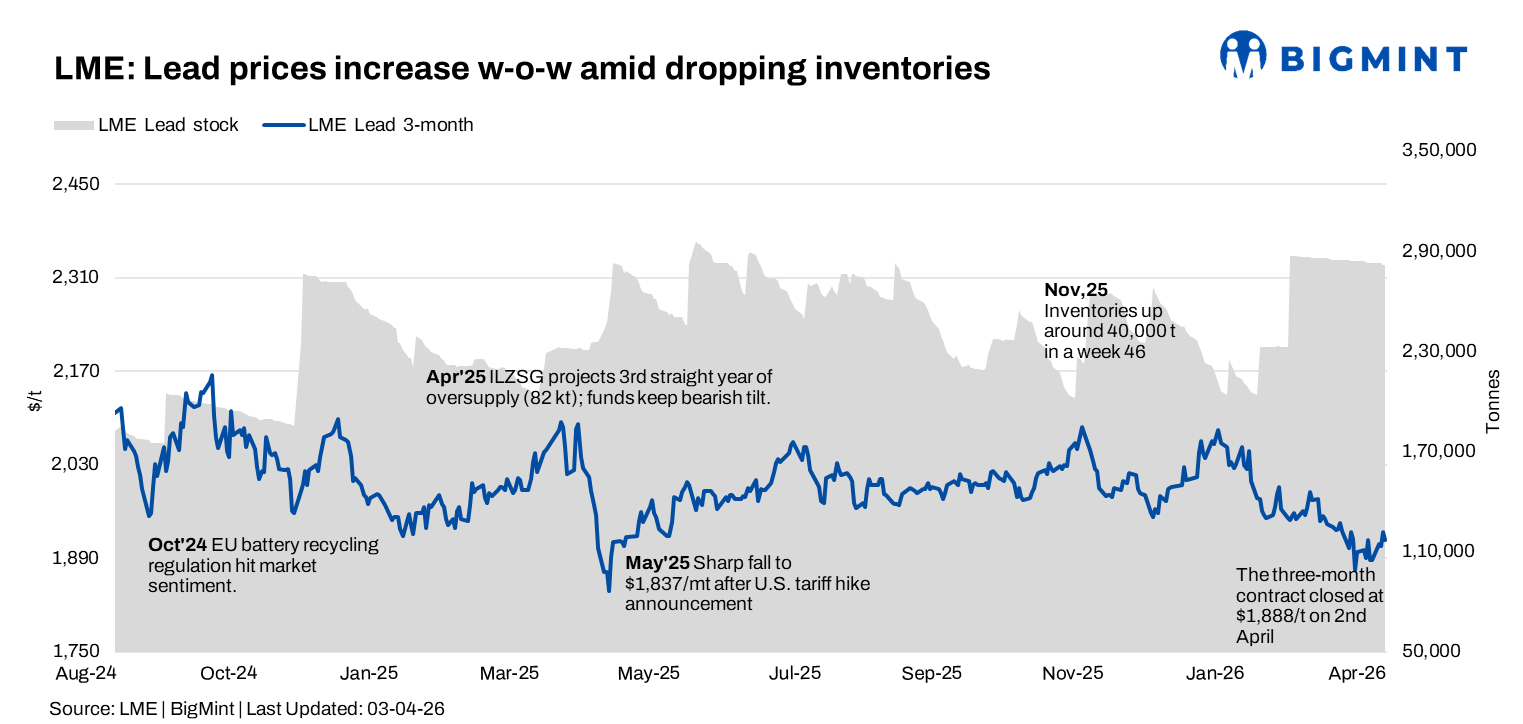

Lead prices on the London Metal Exchange (LME) moved slightly higher in the week ended 4 April 2026, supported by mid-week gains and continued inventory drawdowns. Despite early weakness, prices recovered during the middle of the week before easing slightly, reflecting cautious sentiment and limited follow-through buying. The three-month contract followed a similar trajectory, indicating a range-bound yet marginally firmer market structure.

Price trends

The LME three-month lead contract opened at $1,911.5/t on 30 March and edged lower to $1,909/t on 31 March. Prices then climbed to a weekly high of $1,929/t on 1 April before softening to $1,918/t on 2 April, highlighting mid-week strength followed by mild correction.

On a w-o-w basis, prices increased by around 1%, compared with $1,899/t on 27 March, indicating modest upward momentum supported by intermittent buying interest.

Overall, prices remained within a narrow band, with resistance observed around the $1,920-1,930/t range, while downside remained supported near the $1,900/t level.

Inventory analysis

LME lead inventories continued their declining trend during the week, falling from 283,000 t on 30 March to 281,650 t by 2 April, marking a net drawdown of 1,350 t.

The consistent reduction in stocks points to steady consumption, though the pace remains gradual. Despite ongoing declines, the absence of any sharp inventory drop limited stronger bullish sentiment.

Inventory trends continue to reflect broadly balanced market fundamentals, with no major supply disruptions influencing price direction.

SHFE lead trends

On the Shanghai Futures Exchange (SHFE), lead prices showed a gradual upward trend through the week. Prices remained stable at $2,363/t between 30 March and 1 April before rising to $2,366/t on 2 April and further to $2,382/t on 3 April.

The steady increase toward the end of the week indicates improving sentiment in the Chinese market, supported by mild downstream demand recovery, although overall gains remained moderate.

MCX price movements

On the Multi Commodity Exchange (MCX), lead futures displayed a volatile but slightly weaker trend during the week.

The April 2026 contract opened at INR 198,600/t on 30 March and declined to INR 195,250/t on 2 April, registering a w-o-w drop of around 1.1%.

Prices traded within a range of INR 192,600/t to INR 198,600/t during the week. While early sessions saw selling pressure, mid-week recovery attempts were not sustained. Open interest increased steadily, indicating continued participation despite price correction.

Domestic prices underperformed global trends, reflecting cautious buying and some profit booking at higher levels.

Outlook

Lead prices are expected to remain range-bound between $1,880-1,950/t in the near term, as moderate inventory drawdowns and mixed trends across global exchanges point to stable but directionless fundamentals.

While continued stock declines may provide some support, subdued demand-particularly from the battery segment-is likely to restrict significant upside, keeping prices within a narrow band.

Leave a Reply