- Brazilian shipments rise 16% on active fixtures

- Freights recover amid limited vessel supply

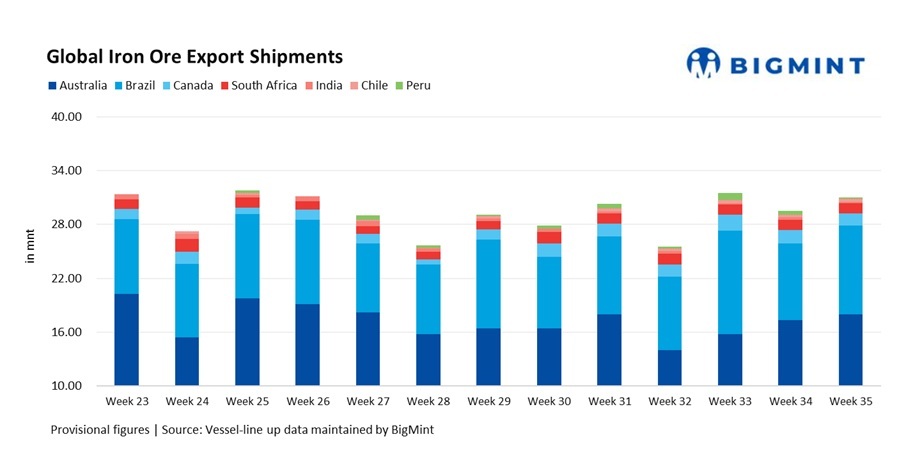

Global iron ore exports climbed up by 5.1% to 31.02 million tonnes (mnt) in Week 35 (23-29 August 2025), from 29.50 mnt in Week 34. The increase marks a return to growth after last week’s dip, underpinned by stronger flows from Australia and Brazil. The improvement was driven by steadier vessel activity at key ports, healthier loading schedules, and firmer demand from Chinese mills, which encouraged dispatches despite fragile steel margins.

Market participants noted that the rebound came at a time when freight sentiment turned bullish, with shipowners maintaining firm offers and vessel supply tightening as carriers were diverted towards grain trades. Firmer iron ore futures and spot pricing in China further encouraged some buying interest, lending additional support to export momentum.

Country-wise exports

Australia’s iron ore exports reached a new weekly high for August in Week 35, rising 3.5% w-o-w to 17.96 mnt from 17.35 mnt in Week 34.

The growth was supported by stronger vessel activity at Pilbara ports, with Port Hedland handling about 11 mnt, Dampier 3.5 mnt, and Cape Walcott close to 3 mnt. Among the major miners, Rio Tinto shipped 6.5 mnt, BHP 4.8 mnt, and FMG 4.8 mnt, highlighting steady operations.

China remained the dominant destination with 15 mnt, while South Korea (1.0 mnt) and Japan (0.7 mnt) took smaller volumes. With weather conditions improving and loading schedules normalising, Australia’s reliable flows once again anchored supply in the Pacific basin.

Brazil’s iron ore exports rebounded sharply in Week 35, rising 15.6% w-o-w to 9.89 mnt from 8.55 mnt in the previous week. The increase was driven by higher loadings at Ponta da Madeira (4.6 mnt) and at Itaguai and Tubarao ports (2.2 mnt each).

Vale led the recovery, contributing around 5.2 mnt of total dispatches. China remained the primary destination with 4.4 mnt, while limited parcels moved to European mills.

The rebound reflected both operational catch-up after earlier slowdowns and steady demand for Brazil’s high-grade ores, which continue to find support in Chinese blending strategies despite the added cost of long-haul shipments.

Canada’s iron ore exports, on the contrary, declined by 4.7% in Week 35 to 1.38 mnt, compared with 1.45 mnt in the prior week. Loadings eased at Milne Inlet (0.3 mnt) and Port Cartier (0.2 mnt), while Sept-Iles contributed the bulk at around 0.9 mnt. Europe remained the key destination, with Belgium and Germany each taking about 0.2 mnt.

Canada’s high-grade concentrates continue to attract steady demand, but seasonal weather challenges and navigation constraints limited overall export momentum, BigMint observed.

South Africa’s iron ore exports also slipped by 4.8% to 1.14 mnt in Week 35 from 1.19 mnt previously.

Shipments from Saldanha Bay eased slightly to around 1.1 mnt, with China taking 0.4 mnt, while The Netherlands and Slovenia absorbed about 0.2 mnt each.

South Africa continues to serve as a supplementary supplier to Asian and European markets, but recurring logistical bottlenecks and infrastructure inefficiencies remain a drag on export reliability. Market participants viewed South Africa-China freights as elevated and held back from active bookings, sources said.

India’s iron ore exports fell sharply by 42% w-o-w to 0.16 mnt in Week 35 from 0.28 mnt in the prior week, as heavy monsoon rains disrupted mining operations and inland transportation. Notably, India’s iron ore exports, including pellets, dropped to a nearly three-year low — the lowest since export duties were lifted in November 2022, data maintained with BigMint shows.

Shipments were largely directed to China (0.04 mnt), where mid- and low-grade fines continued to find demand among cost-sensitive mills. The steep decline highlights India’s seasonal vulnerability and its supplementary role in global seaborne supply.

Chile’s exports increased by nearly 10% w-o-w to 0.32 mnt compared with 0.29 mnt in Week 34, providing some support to overall export shipments. Loadings from port Huasco (0.2 mnt) and Totoralillo (0.1 mnt) supported the rise.

Chile continues to play a niche role in supplying Asian buyers, though its export ceiling remains capped by limited production and logistical infrastructure.

Peru’s shipments slumped by 55% w-o-w to 0.17 mnt from 0.38 mnt in the prior week.

Loadings at San Nicolas dropped significantly to 0.2 mnt, reflecting the country’s dependence on a single export hub. The volatility highlighted the fragile nature of Peru’s supply, which adds flexibility to the market but remains vulnerable to operational shifts.

Dry bulk iron ore freights rebound w-o-w amid active fixtures, rise in FFA rates

Dry bulk iron ore freights rebounded in Week 35 as stronger fixture activity, firmer derivatives, and rising bunker costs lifted sentiment across both Pacific and Atlantic basins.

Shipowners held the upper hand, particularly on the Australia-China route, where miners actively sought tonnage. Atlantic markets followed the firming trend despite lighter activity.

The rally was further supported by vessel diversions towards grain shipments ahead of the harvest season, which tightened supply. Firmer iron ore prices and futures in China added to optimism, encouraging some short-term restocking demand, despite lingering caution around steel margins.

Outlook

Export momentum is expected to remain steady in the near term, with Australia maintaining elevated loadings and Brazil sustaining its recovery. Seasonal disruptions in India and logistical challenges in South Africa may continue to cap flows, while Canada and Peru are likely to see fluctuating dispatches.

Freights are likely to remain under pressure, with muted demand from China and ample vessel availability capping upside momentum. While occasional fixtures may lend temporary support, sentiment is expected to stay cautious as charterers resist higher offers and freight derivatives continue to signal weakness.

Leave a Reply