- ADC12 imports from Malaysia likely to resume soon

- GST slashed on cars, bikes in bid to revive auto sector

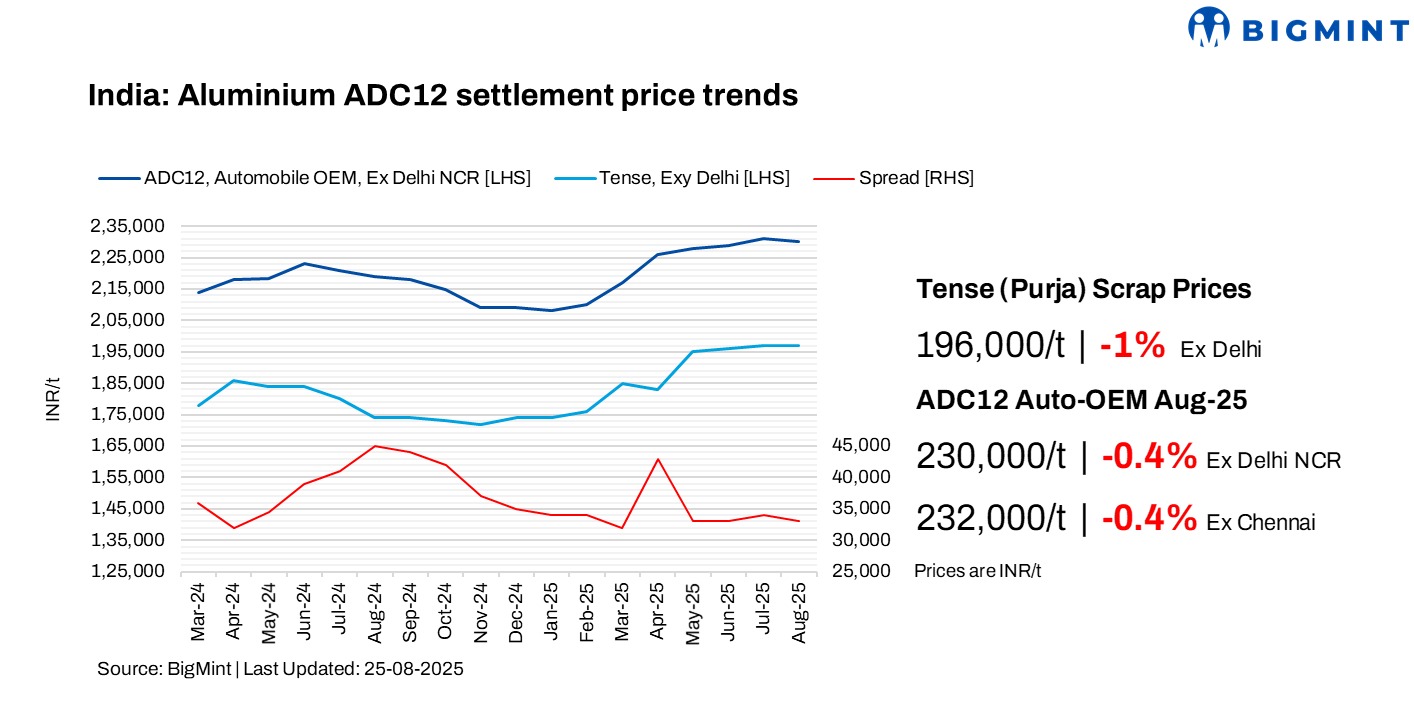

India’s secondary aluminium market witnessed a slight dip in August 2025 after continuous gains in alloy ingot prices through the first half of the year. The fall came despite strong demand from die-casting and auto component manufacturers, along with elevated input costs.

According to BigMint’s assessments, average automobile OEM ADC12 prices for August fell by up to INR 1,500/tonne (t) m-o-m to INR 230,000/t in Delhi and INR 232,000/t in Chennai. The scrap-to-semi-finished spread held steady in the INR 32,000-33,000/t range, reflecting the steady cost of sourcing raw materials.

Additionally, a major Indian automaker marginally reduced its ADC12 settlement prices by INR 150/t m-o-m to INR 229,600/t for September, marking the first drop after seven consecutive months of gains. The slight dip is attributed to a correction in scrap prices amid falling LME levels and an expected improvement in ADC12 imports. The scrap-to-ADC12 spread remained stable at INR 32,000-33,000/t as of August.

Market dynamics in early Sep’25

Offers for ADC12 remained on the higher side in both north and south India, hovering between INR 232,000-233,000/t in Delhi and INR 233,000-234,000/t in Chennai.

Bids in the north were heard at INR 228,000-229,000/t and in the south at INR 230,000-231,000/t.

Offers for ADC12 in Chennai stood at around INR 236,000/t for 45-day credit payment terms.

An alloy maker from the south informed BigMint, “ADC12 prices are expected to stabilise or see a mild correction, with Malaysian imports likely to resume soon. Notably, 4-5 key Malaysian alloy suppliers have already secured BIS certification, and additional producers are steadily gaining approval, strengthening the overall supply outlook.”

Raw material trends

In August, both imported and domestic aluminium scrap prices witnessed a slight decline, in line with a 0.42% drop in LME aluminium, which averaged $2,594/t for the month. This downtrend was largely influenced by ongoing tariff uncertainties and evolving market conditions in China.

Among key imported grades, US-origin Tense fell by $60/t m-o-m to $1,980/t, while UK-origin Wheels dropped by $15/t to $2,570/t. On the domestic front, Tense scrap prices decreased by INR 1,000/t, with BigMint’s end-July assessment placing prices at INR 196,000/t in Delhi and INR 199,000/t in Chennai.

Additionally, Chinese silicon 553 prices slipped by $5/t m-o-m, settling at $1,368/t CFR Mundra, weighed down by elevated inventory levels.

Tracking India’s scrap, ingot import flow in 7MCY’25

In 7MCY’25, India’s aluminium scrap imports increased by 10% y-o-y, to 1.07 mnt from 0.98 mnt in 7MCY’24. Taint Tabor remained the most imported scrap grade, which saw a gain of 11% y-o-y to 241,714 t from 217,964 t. The US continued as the leading supplier, exporting 201,061 t to India, reflecting a 14% decrease from 7MCY’24 primarily due to the strong domestic demand for scrap and tariff-related uncertainties in the US.

India’s ADC12 alloy market witnessed a dramatic contraction in imports during the first seven months of 2025 (7MCY’25), with inbound volumes plunging by 79% y-o-y. Total ADC12 imports stood at just 3,308 t, down sharply from 15,421 t in 7MCY’24.

Auto sector performance

According to FADA’s retail data, passenger vehicle sales rose 10% m-o-m to 328,613 units in July, up from 297,722 units in June. The segment benefited from strong urban demand and improved availability of popular models. In contrast, two-wheeler sales slipped 6% m-o-m to 1,355,504 units, reflecting weaker rural sentiment and the impact of erratic monsoon rains.

On the wholesale side, SIAM data showed a slightly different picture. Passenger vehicle sales grew 9% m-o-m to 340,772 units, aligning with the retail uptrend. Two-wheeler sales inched up 0.5% to 1,567,267 units, indicating that OEM dispatches remained stable despite weak retail traction. Three-wheeler sales recorded a sharp 12.3% increase to 69,403 units, while commercial vehicle sales were largely flat at 75,000 units.

GST slashed on cars, bikes; govt aims to revive auto sector

GST rationalisation is set to boost demand in the auto sector, especially among entry-level buyers who stayed away due to price hikes and subdued income growth. Small cars under four metres and with engine capacities below 1200 cc (petrol) and 1500 cc (diesel) will now attract 18% GST from 22 September, down from 29-31%, potentially reducing prices by 12-13%. Motorcycles below 350 cc will also see GST cut to 18% from 28%. The government has scrapped 12% and 28% slabs and withdrawn the compensation cess. Industry leaders have welcomed the move but seek clarity on cess utilisation for unsold vehicles.

However, some alloy ingot makers remain cautious, noting uncertainty regarding whether the GST rate on scrap will be lowered to the 5% slab, which could influence price dynamics.

Outlook

ADC12 prices for September in both north and south India are expected to remain range-bound, despite a decline in scrap tags, supported by anticipated festive season demand. A sharp correction in ADC12 prices appears unlikely. Moreover, while a major automaker has made minor price reductions for September settlements for ADC12, the absence of significant cuts is likely to keep domestic prices stable.

Notably, the recent GST cut on vehicles is expected to boost demand in the automotive sector, increasing consumption of aluminium alloy ADC12 used in die-casting, especially as aluminium gradually replaces steel. Market anticipations estimate a demand increase of around 5-8%.

Leave a Reply