- Mexico, India see sharp declines in scrap imports in CY’24

- US exporters may hold firm, impacting trade volumes in Q1CY’25

US ferrous scrap exports hit their lowest level since 2020, dropping 20% y-o-y to 14.52 million tonnes (mnt) in CY’24 from 15.74 mnt in CY’23. Most months saw weaker shipments, with January down 20% y-o-y to 0.97 mnt and March falling by 22% to 1.12 mnt. May (1.5 mnt) and December (0.85 mnt) recorded steep declines of 23%, driven by slowing demand from key buyers like Turkiye, Mexico, and Canada.

Despite the overall downturn, some months showed resilience. July rebounded sharply by 39% y-o-y to 1.24 mnt from 0.89 mnt in CY’23 followed by gains in August and November. June remained relatively stable, with only a slight increase.

The decline in ferrous scrap exports was primarily due to reduced shipments to India, Mexico, and Taiwan, while sponge iron imports rose by 8% y-o-y.

US scrap export and domestic prices:

- Shredded scrap prices: $376/t in 2024, down from $391/t in 2023 ($15/t decline).

- HMS prices: $356/t in 2024, down from $371/t in 2023 ($15/t drop).

US domestic ferrous scrap prices remained weak in 2024, weighed down by sluggish mill demand and soft HRC prices. While regions like the Ohio Valley and Southeast saw a brief price uptick in October, benchmark markets like Chicago and Detroit stayed flat all year.

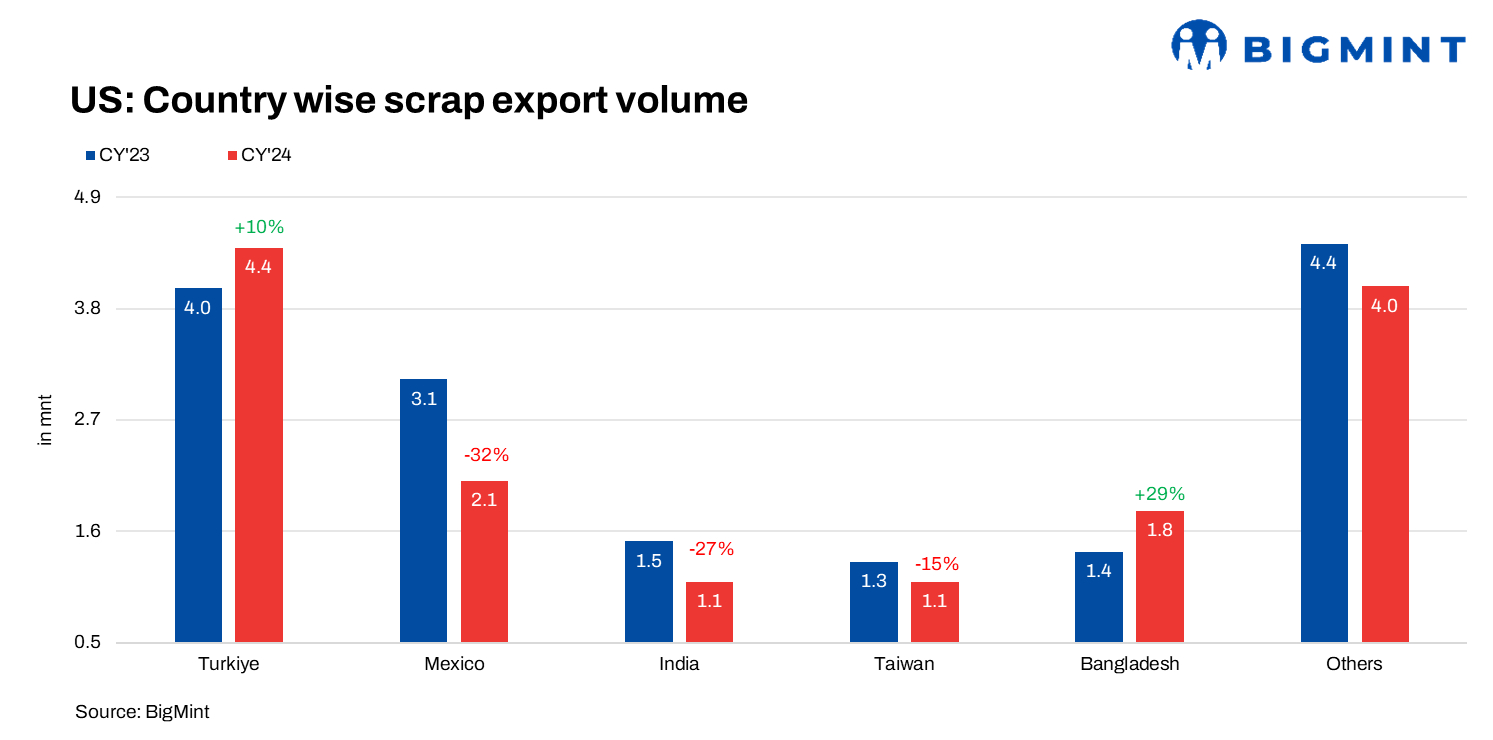

Country wise

Turkiye: Scrap imports rose by 9% to 4.4 mnt in 2024, up from 4.0 mnt in 2023, reflecting higher intake.

Mexico: Scrap imports fell 32% to 0.21 mnt in CY’24 from 0.31 mnt in CY’23, due to weaker demand and reduced steel production.

India: Scrap imports declined 25% to 1.1 mnt in 2024 from 1.5 mnt in CY’23, driven by lower steel demand and higher domestic scrap availability.

Taiwan: Scrap imports dropped 11% to 1.1 mnt in 2024 from 1.3 mnt in CY’23, reflecting weaker steel production and a shift toward alternative raw materials.

Bangladesh: Scrap imports surged 28% to 1.8 mnt in 2024 from 1.4 mnt in CY’23, driven by strong demand from the shipbreaking and steel sectors despite economic uncertainties.

Other updates

Crude steel production held steady at 80.7 mnt in CY’24, barely changing from 80.75 mnt in CY’23.

US scrap imports: US scrap imports declined y-o-y to 4.49 mnt in CY’24, down from 4.89 mnt in CY’23, matching the 2022 levels (4.48 mnt), due to reduced shipments from Canada (-8% to 3.18 mnt). However, imports from Mexico surged 36% to 0.9 mnt.

US pig iron imports: Pig iron imports hit a three-year high at 4.7 million mt (+8% y-o-y) in CY’24 up from 4.35 mnt in CY’23, with Brazil supplying over 70% and supported by steady demand from steel mills.

Outlook

Some market insiders believe the US has enough scrap to sustain local steel production without imports, which could push domestic scrap prices higher as mills compete for supply. This could force Canadian and Mexican exporters to find new buyers, likely in Asia, potentially driving prices down there. Meanwhile, strong domestic demand may lead US exporters to hold firm, impacting trade volumes in Q1.

Some US mills are holding off on orders, waiting for clearer market signals, while overseas buyers like Turkiye are rushing to secure supply. The White House touts the move as a win for domestic producers, but manufacturers worry about rising costs and a repeat of 2018’s price surge.

Leave a Reply