- Tier 1 mills raise HRC, BF rebar list prices

- IF rebar tags rise as active trades continue

- HRC, plate imports decline by 12 % m-o-m

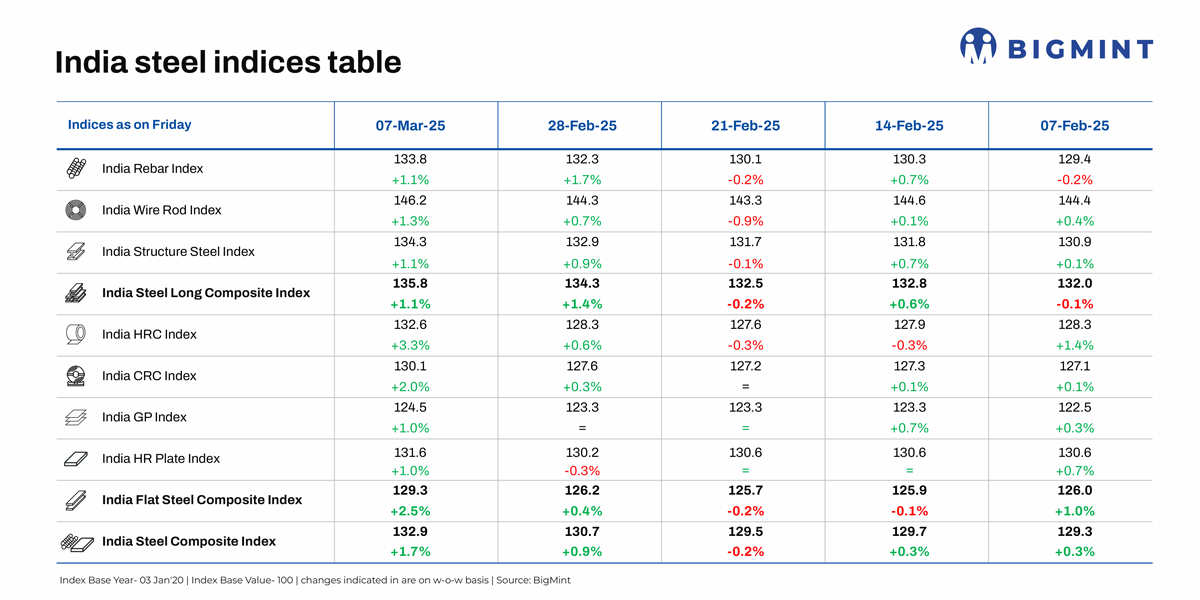

Morning Brief: BigMint’s India Steel Composite Index climbed up by 1.7% w-o-w to 132.9 points on 7 March 2025, a level last seen in early-October 2024. Suppliers substantially increased offers, spurred by speculation over the imminent announcement of a safeguard duty and persistent material undersupply in certain segments.

Both the flats and longs indices increased w-o-w, the former by a robust 2.5%. Hot-rolled coils (HRCs) witnessed the highest rise of 3.3%, and cold-rolled coils (CRCs) were up by 2.2%. The longs index climbed up by 1.1%, driven by an increase of 1.1-1.2% in the rebar, wire rod, and structure steel indices.

Notably, the index is currently placed at mid-November 2024 levels, a four-month high.

Factors driving index last week

Mills raise HRC list prices: Leading steelmakers officially raised list prices of HRCs and CRCs by INR 1,100-1,500/tonne (t) ($13-17/t) for March sales.

A number of factors spurred the hike: First, the market was abuzz with speculation over the imminent announcement of the proposed safeguard duty on steel imports. Market participants believe that such a measure could push up prices by a significant INR 2,000-3,000/t ($23-34/t). Some mills even delayed their list price announcements, waiting for official communication. Although the duty announcement is still awaited, mills have, nevertheless, gone ahead with the hike.

Secondly, the HRC supply crunch continued, especially in north India where trade-level prices moved up significantly. Meanwhile, in other regions, the supply issue alleviated to a certain degree. However, the CRC segment saw material scarcity across India.

As a result, trade-level prices for HRC (IS2062, Gr E250, 2.5-8 mm/CTL, ex-GST) were higher by INR 700/t ($8/t) w-o-w at INR 49,000/t ($562/t) ex-Mumbai.

Notably, while suppliers pushed up offers, signs of buyer resistance also emerged.

Supply shortages boost BF rebar prices: The Tier 1 mills raised rebar list prices by up to INR 2,000/t ($23/t) for early-March deliveries compared to end-February levels, sources informed BigMint.

Supply constraints were the main push behind the mills’ decisions to raise list prices. Notably, rebar inventories at mills declined by around 6% m-o-m in early-March.

Additionally, amid surging demand from the project segment, the trade channel continued to face a supply squeeze across sizes, especially in north India, which pushed up trade-level prices. Reports of logistics issues in some regions also propelled tags higher.

Trade-level prices of BF rebars in Mumbai stood at INR 54,300/t ($623/t), exclusive of GST at 18%, up by INR 1,100/t ($13/t) w-o-w. In the projects segment, prices rose w-o-w to around INR 52,500-53,500/t ($602-614/t) FOR Mumbai.

IF rebar tags rise as trades improve: Induction furnace (IF) route rebar prices increased by INR 300/t ($3/t) to INR 49,400/t ($567/t) in Mumbai, with other regions witnessing a hike of INR 100-600/t ($1-7/t).

Trade momentum continued amid healthy demand. Buyers procured decent volumes, while dispatches of previously booked material continued smoothly. As a result, there was no selling pressure on suppliers, which prompted them to lift offers or reduce trade discounts. However, some buyers were unwilling to trade at these levels.

HRC imports continue to drop m-o-m: The downtrend in India’s bulk imports of HRCs and plates continued, with February registering 413,020 t compared to 471,623 t in January and 473,222 t in December 2024, according to BigMint’s vessel line-up data. Imports declined by 12% m-o-m in February, much steeper than the m-o-m drop between December and January.

India’s HRC export offers trend down w-o-w: BigMint’s India HRC (SAE 1006) export index (for the Middle East and Vietnam) dropped by $10/t w-o-w to $495/t FOB east coast India. This followed a sharp drop of $15/t w-o-w in Indian HRC export offers to the Middle East to $515/t CFR UAE amid recent deals, though demand picked up slightly.

Indian mills continued to stay on the sidelines of the European market amid ongoing anti-dumping investigations.

Outlook

The positive price momentum may continue in the near term across both flats and longs, with suppliers unwilling to lose ground following weeks of range-bound trading.

In the HRC segment, however, downstream demand still lags, and if the safeguard duty buzz fizzles out, prices may moderate. Another factor to consider is that suppliers may reduce offers to liquidate stocks in case of a cash crunch. Additionally, given that the fiscal year-end is approaching, there is increasing pressure to maintain proper balance sheets. This may weigh on prices.

Meanwhile, tight supply is expected to continue, which will prop up HRC, CRC, and BF rebar tags to a certain degree. BF rebars will continue to see robust demand from the projects segment. In fact, BF mills are planning to raise list prices a few more times this month, according to sources.

While Holi will lead to a lull in construction and manufacturing activity across the country, expectations are that rebar prices, especially in the IF segment, may further rise because of labour shortages and logistical challenges.

India Steel Composite Index

The India Steel Composite Index is assessed on a weekly basis, every Friday at 18:30 IST, as per the weighted average prices based on manufacturing capacity and production.

BigMint considers the Composite Index with the base year being 3 January 2020 (financial year 2019-2020) and the base value as 100. The Composite Index does not give the absolute price but a trend of the market. The Indian steel industry is broadly classified into the BF-BOF and the electric/induction furnace routes. Keeping this broad classification in view, BigMint proposes to release the Composite Index by considering both production routes by manufacturing capacity and the production weighted method to compute the index for India.

Leave a Reply