- HMS processed prices fall; but premium yards price remain firm

- Slower bookings likely till clearer market signals emerge

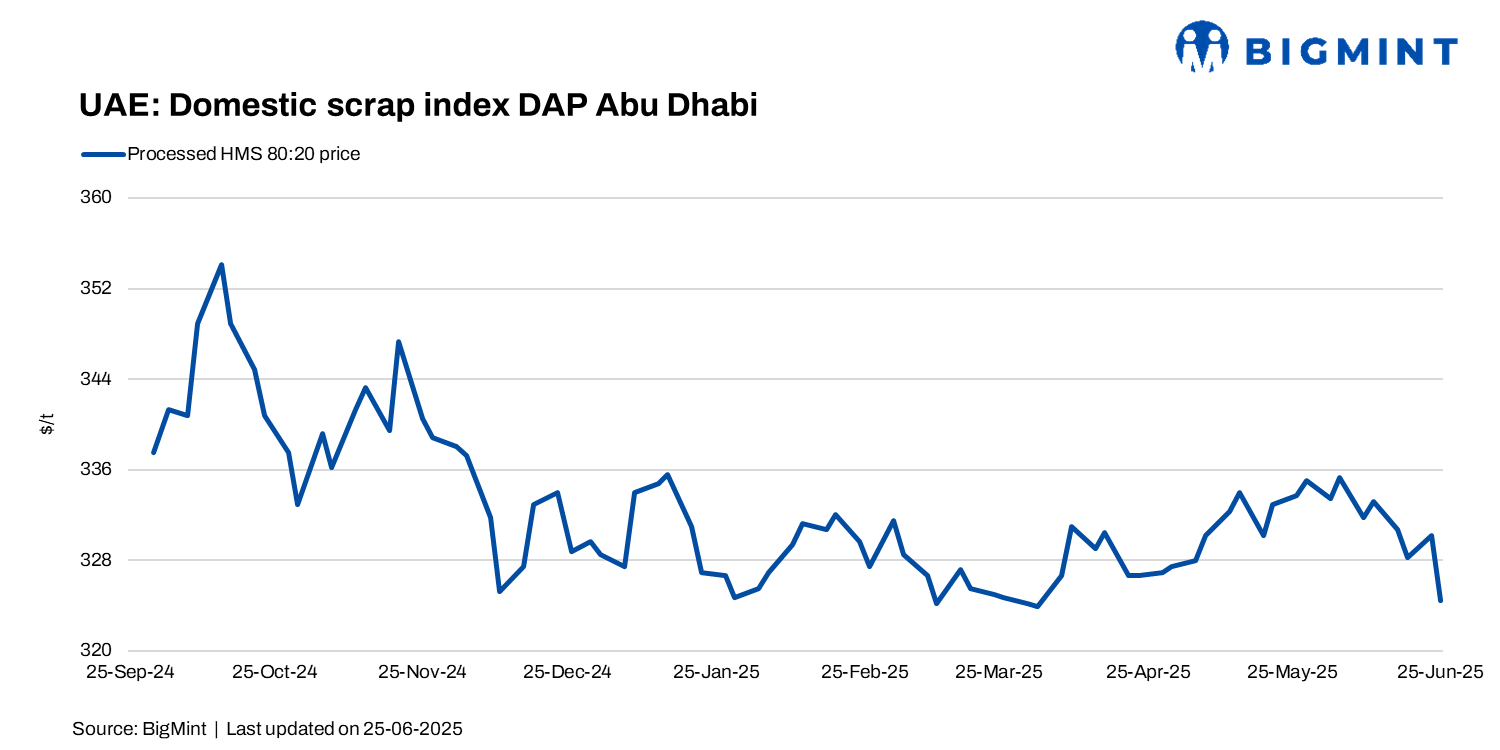

BigMint‘s UAE domestic processed HMS index declined by AED 14/tonne ($4/t) w-o-w to AED 1,192/t ($325/t), as local demand softened amid oversupply and weak mill procurement. Mills remain cautious due to ongoing geopolitical uncertainty and the absence of any fresh buying triggers.

Market activity has slowed significantly, with mills deferring new bookings. Traders are also treading carefully, anticipating a potential fuel price hike and monitoring the Strait of Hormuz situation, which could disrupt logistics and dent sentiment.

Recent trades include 3,000 t of HMS processed sold at AED 1,225/t and 1,500 t of shredded at AED 1,300/t–both from premium yards on a DAP Abu Dhabi basis.

Mills are reportedly willing to pay around AED 1,175/t ($320/t) for HMS processed on a DAP basis, while container loading offers are hovering at AED 1,150/t ($313/t).

Pure LMS was offered at AED 830-850/t ($226-231/t) and HMS 80:20 at AED 1,160-1,170/t ($316-318/t). HMS processed workable levels have dropped to AED 1,170-1,180/t ($319-321/t), PNS (processed) remains firm at AED 1,220-1,230/t ($332-335/t), while fabrication scrap is slightly lower at AED 1,240-1,250/t ($338-340/t). Rebar end-cut scrap declined to AED 1,270-1,280/t ($346-348/t).

Market scenario

A Dubai-based trader shared, “The market is still under pressure–mills are not in a rush. We were offering HMS processed at AED 1,200-1,210/t, but there’s no real interest. Even our major buyers have not responded. Oversupply is real, and no one wants to stock unnecessarily.”

An Abu Dhabi-based trader added, “Uncertainty is keeping everyone cautious. If fuel prices rise or there is a disruption at the Strait of Hormuz, we could see a sudden buying push. We managed deals at AED 1,225/t for HMS processed and AED 1,300/t for shredded, but overall demand remains weak.”

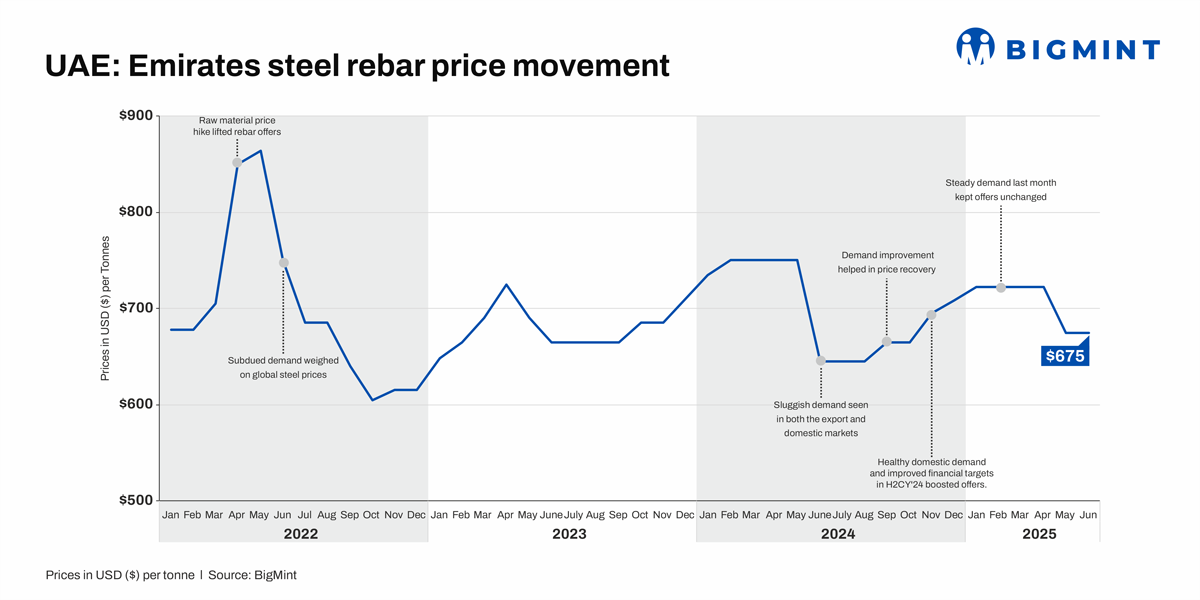

Emirates Steel rolled over rebar offers for Jul’25 at $675/t (AED 2,479/t) exw-Abu Dhabi. June activity slowed due to Eid holidays, summer break, and regional tensions, prompting buyer caution.

Export market update

Shredded scrap offers from the UAE rose to $385-390/t CFR Qasim, up from $375-380/t last week.

UAE material saw higher demand due to quicker lead times and easier logistics, while Western shipments continue to face delays.

UAE-origin HMS is priced at $360-364/t CFR. Meanwhile, Pakistan’s revised customs policy removed duties on melting scrap and billets but imposed a 5% duty on re-rollable scrap. Further clarity on other levies is awaited.

Middle East tensions: steel market impact minimal

The recent Iran-Israel tensions led to Iran launching missiles at the US Al Udeid Air Base in Qatar on 23 June, 2025. Although most were intercepted with no casualties, Gulf nations briefly closed their airspace as a precaution. Despite the escalation, steel operations across Qatar, Saudi Arabia, and other GCC states remain unaffected, with logistics and production continuing smoothly.

Steel market players are monitoring maritime routes, particularly the Strait of Hormuz. While shipments remain on schedule, freight rates have risen by 20-30% and insurance premiums have increased. Some shipping lines have started limiting voyages as a precaution.

Outlook

The UAE scrap market may stay weak in the near term as oversupply and cautious mill buying persist. Mills are likely to delay purchases as finished steel demand remains below expectations.

Leave a Reply