- Mandatory BIS certification affects cathode imports

- Competitive prices, rising secondary production boost scrap imports

- Refined copper deficit pegged at ~300,000 t despite rising smelter capacity

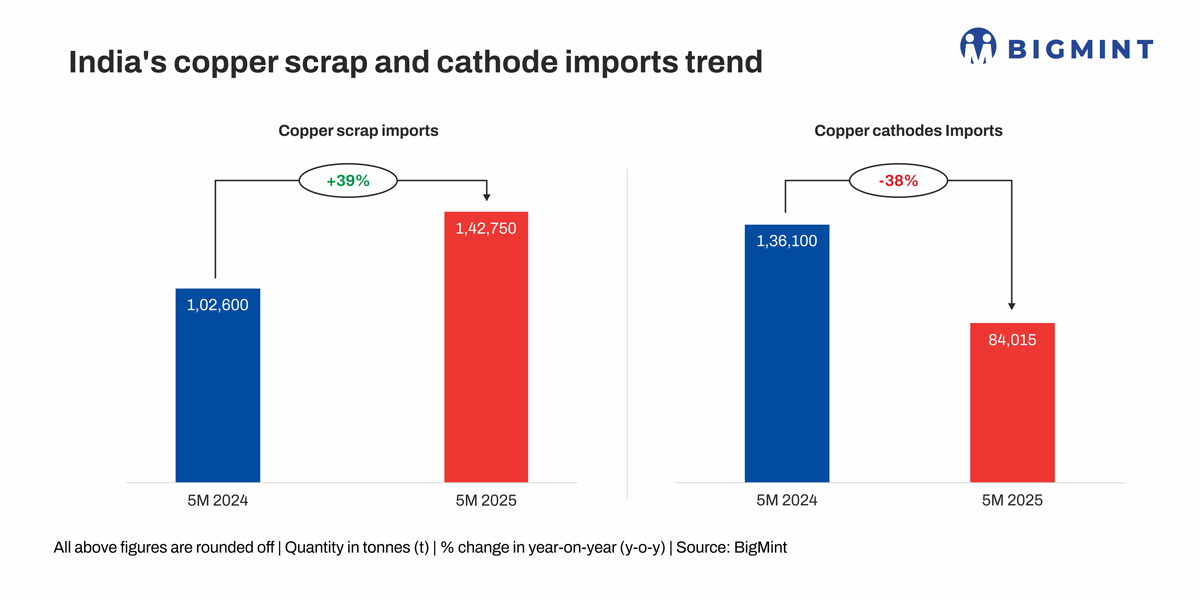

Morning Brief: India’s copper import mix witnessed a significant shift in the first five months of 2025, with copper scrap imports rising 39.1% y-o-y to 142,756 tonnes (t), while cathode imports dropped sharply by 38.3% to 84,015 t, according to data compiled by BigMint.

This reversal in trend shows a growing reliance on secondary copper sources as users move away from higher-cost primary materials.

Why copper scrap imports spiralled in 5MCY’25?

In the 2025-26 Union Budget the government removed the import duty on non-ferrous scrap, including copper. This made imported scrap significantly cheaper for Indian buyers, especially compared to copper cathodes, which still attract duties and other compliance costs.

Globally, copper cathode prices remained high in early 2025 due to tight concentrate supply and rising smelting charges. In contrast, high-grade copper scrap (like Millberry) offered nearly similar copper content at a much lower cost. As a result, many wire rod producers and foundries in India started using scrap instead of cathodes to cut production costs without compromising on metal quality.

Globally, copper cathode prices remained high in early 2025 due to tight concentrate supply and rising smelting charges. In contrast, high-grade copper scrap (like Millberry) offered nearly similar copper content at a much lower cost. As a result, many wire rod producers and foundries in India started using scrap instead of cathodes to cut production costs without compromising on metal quality.There was a noticeable uptick in production from India’s secondary copper rod segment, especially in states like Gujarat, Maharashtra, and Punjab. These manufacturers rely heavily on imported copper scrap as their main raw material.

With strong demand from electrical, construction, and export sectors, scrap importers sourced larger volumes from markets like the UAE, Malaysia, and Saudi Arabia, where premium grades are available at competitive rates.

According to a source, “Faster customs clearance for scrap compared to cathodes-owing to fewer BIS and Quality Control Order (QCO) requirements—have also made scrap more attractive. Indian importers increasingly prefer scrap due to quicker port handling and fewer documentation hurdles”.

Why cathode imports declined?

Since December 2024, India has made it mandatory through a QCO for both domestic copper cathode and imports to obtain necessary certification under BIS (IS 191:2007). Many foreign suppliers could not meet the new certification in time, so shipments dropped drastically. In January this year imports fell by nearly 95% y-o-y. Trade bodies even raised legal concerns, saying the rules were hurting competition.

This regulatory shift has disrupted shipments, particularly from Japanese producers—who account for nearly two-thirds of India’s refined copper imports—as many struggled to meet the new compliance standards, leading to a steep decline in inbound volumes.

India’s domestic copper production has been picking up. Adani’s new Kutch Copper smelter started operations recently and JSW plans to open a large copper plant by 2028. With more copper being produced locally, there would be less need going forward to import cathodes, especially when global supply remains tight and expensive.

Many importers had anticipated the new QCO rules and rushed to bring in extra copper cathodes in late 2024. In April-November 2024, India imported about 27,000 t per month, building large inventories. Because of this stockpiling, companies did not need to import as much in early 2025, leading to a sharp fall in shipments.

Product import profile

India’s copper import profile in the first five months of 2025 shows a strong rise in flat product imports, up 40% y-o-y to 89,050 t, led by a near-doubling of imports of plates, sheets and strips (up 97%) and a 38% jump in pipes and tubes. In contrast, long products like bars and wires saw a mild contraction.

As cathode supplies were disrupted by BIS – QCO enforcement, buyers turned to downstream flat products-which do not require cathode-level purity and can be recertified locally.

Country-wise share in scrap imports

Copper scrap shipments from the UAE to India surged 184%, driven by traders capitalising on short transit routes and access to clean, high-grade material. The US followed with a 65% rise, supported by strong containerised exports of high-grade scrap. Saudi Arabia also expanded its share by 35%, continuing as a reliable supplier of Berry/Candy and motor scrap at consistent quality and prices.

Snapshot of finished copper imports

Pricing scenario

Pricing scenario

According to BigMint’s assessment, in 5MCY’25 copper scrap prices in India remained comfortably below the LME benchmark. Middle East-origin Birch/Cliff averaged around $8,770/t, while US-origin motor scrap hovered at $1,160/t. Even Brass Honey from the Middle East traded at an average of $5,930/t CIF Mundra.

In comparison, the six-month average LME cash copper price stood at $9,420/t, putting premium scrap grades like Birch/Cliff at a 5-7% discount to refined copper.

However, growing scarcity of refined copper and declining LME inventories have flipped the script for certain scrap grades. Millberry, which traditionally traded at 97–98% of the 3M LME price, has now reached parity- and in some cases, even exceeded LME prices, with deals reported at 101% of LME.

This unusual inversion highlights how clean, high-grade scrap has become a prized and sometimes premium alternative in today’s market.

What’s next?

Copper supply tightness is likely to persist through 2025. While new smelters like Adani’s (1 mnt/year by FY’29) and JSW’s (500,000/year by CY’28) are in the pipeline, they will not ease India’s – 300,000-t refined copper deficit immediately.

Leave a Reply