The South Asian scrap index was further marked by cautious buying behavior across key countries, with India, Pakistan, and Bangladesh all witnessing sluggish demand for imported scrap amid local challenges. In India, a weakening steel market and sufficient domestic supply have led to a decline in interest for imported scrap. Pakistan is similarly seeing limited purchases due to a seasonal slowdown and expectations of price corrections. Meanwhile, in Bangladesh, economic uncertainties and banking issues have kept scrap transactions subdued. Turkiye, facing its own pressures, has seen a further drop in imported scrap prices, with mills pushing for lower rates.

India: In India, demand for imported scrap has been sluggish, with buyers leaning towards more cost-effective domestic alternatives. The weakening domestic steel market has further dampened scrap consumption from this sector. Indicative offers for shredded scrap from the US and UK/Europe were in the range of $400-410/t CFR Nhava Sheva, but there were no takers, even at $400/t CFR.

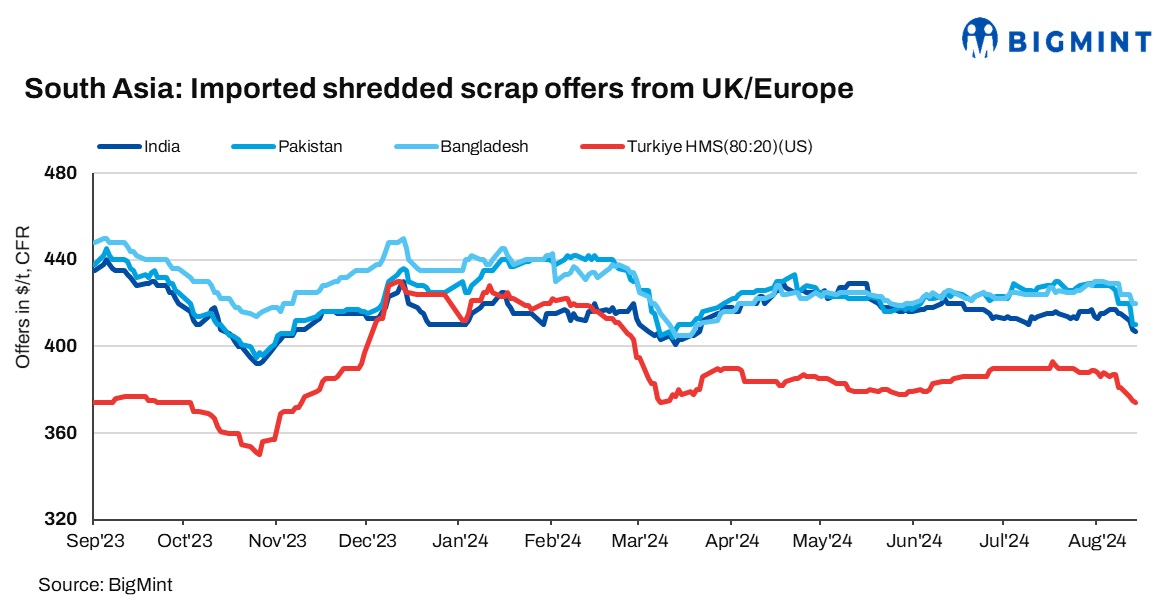

HMS (80:20) offers from the UK/Europe were reported at $380/t CFR, but there was no buying interest at this price point.

A steel mill based in southern India commented, “We have no interest in purchasing imported scrap as our inventory is sufficient. Additionally, we’ve implemented nearly 30% production cuts due to weak steel demand, and we’re opting to buy scrap from the domestic market, which is cheaper and readily available. Previously booked material is still arriving, so we don’t anticipate any fresh bookings anytime soon.”

Pakistan: Pakistani buyers exhibited limited interest in imported scrap, purchasing only as needed due to sluggish steel sales during the ongoing seasonal slowdown. Indicative offers for shredded scrap from the UK and Europe were around $408-410/t CFR Qasim.

Market participants noted that buyers are holding off on purchases, anticipating a price correction.

Bangladesh: Bangladesh’s imported scrap market saw limited activity today, with buyers cautious due to sluggish steel sales and challenges in the banking sector. In the domestic market, rebar prices were stable at BDT 87,000- 87,500/t ex-Dhaka, while Chattogram prices were slightly higher.

Offers for HMS (80:20) from Australia were around $412/t CFR Chattogram, but bids were lower at $405-406/t CFR. Shredded scrap was offered at $428/t CFR, with bids at $420-422/t CFR. Market participants expect an improvement in activity once banking operations normalise, but no significant deals have been reported in the past 2-3 weeks.

Turkiye: Turkish imported ferrous scrap prices dropped further, following the recent Eu-origin deals driving the decline. Meanwhile, offers for US origin bulk HMS (80:20) were assessed at $374/t CFR, a $1/t decrease from the previous day. Turkish mills, under pressure, pushed for lower prices, with bids for EU-origin scrap ranging from $360-$365/t CFR. Despite this, sellers were cautious, offering HMS (80:20) at $375-$379/t CFR from the UK/EU and $378-$380/t CFR from the US. The market remained tense, as mills had recently imported large quantities of billets, reducing their need for scrap. Meanwhile, shortsea scrap prices held steady at $367/t CFR, with limited room for further declines.

Price assessments

India: UK-origin shredded scrap indicatives were assessed at $407/t CFR Nhava Sheva, down by $1/t d-o-d.

Pakistan: UK-origin shredded indicatives were assessed unchanged at $410/t CFR Qasim.

Bangladesh: UK-origin shredded prices were assessed stable at $420/t CFR Chattogram.

Turkiye: US-origin HMS (80:20) bulk prices were at $375/t CFR Turkiye, down by $1/t d-o-d.

Leave a Reply