India’s stainless steel finished flat prices witnessed weekly gains for the 3rd consecutive time on price hikes by India’s leading coil manufacturer. Notably, this marked the second consecutive price increase in August 2024, driven by improved seasonal requirements.

BigMint’s benchmark assessments of stainless steel (304 series) HRC prices stood at INR 179,000/t ex-Mumbai and domestic 304-grade scrap was at INR 121,000/t ex-works Delhi.

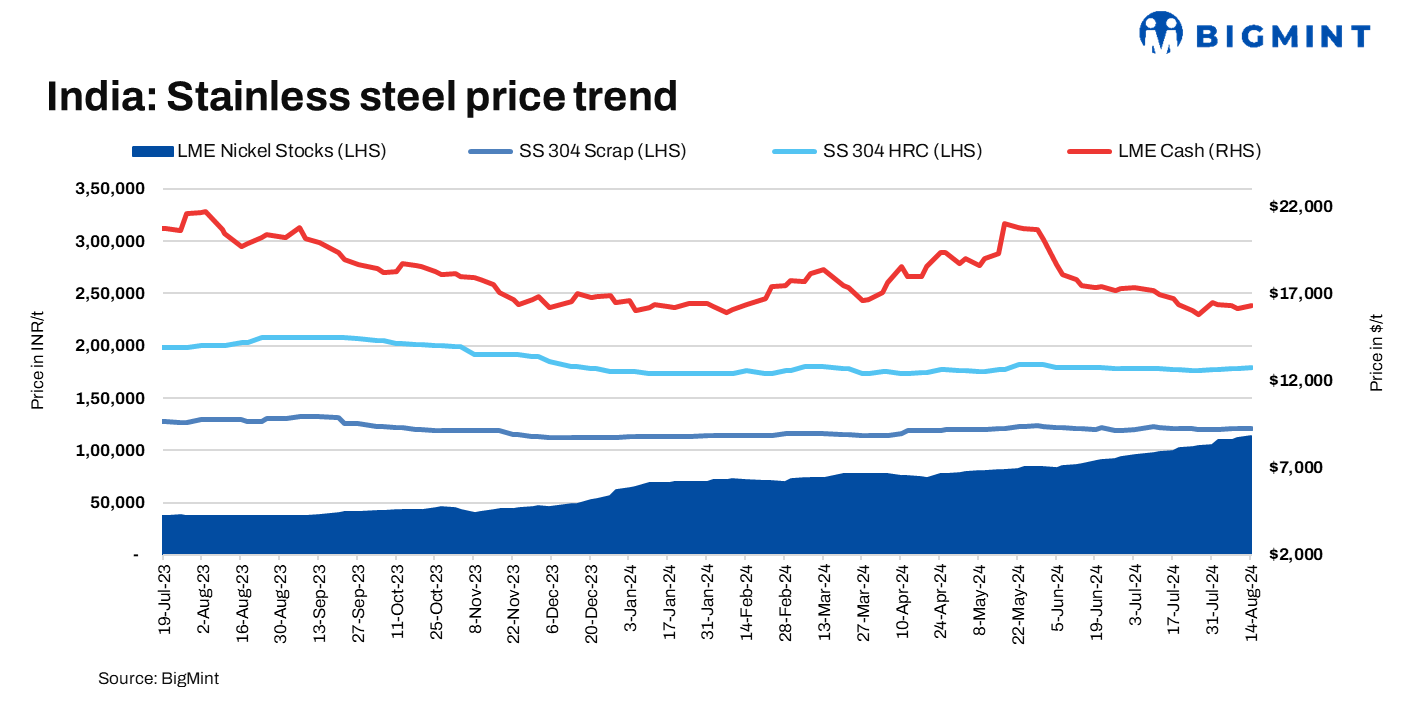

LME nickel prices trends

At the time of reporting, the three-month prices of LME nickel stood at $16,300/t, largely stable from the previous week’s levels. Meanwhile, stocks of nickel in LME-registered warehouses kept increasing w-o-w, reaching 113,712 t from the previous week’s 110,670 t.

Additionally, Indonesia has suspended new smelter construction for midstream nickel products like nickel pig iron and ferronickel. Minister Arifin Tasrif cited concerns over resource depletion, environmental damage, and overcapacity. The government is focusing on developing the electric vehicle and renewable energy sectors and is evaluating advanced smelters like HPAL to enhance value and sustainability.

Domestic finished flats prices firm

In the finished flat segment, prices saw a marginal gain this week. As per BigMint’s assessment, 304 HRC prices stood at INR 178,000-180,000/t, while prices of the SS316 HRC stood at INR 309,000-311,000/t ex-Mumbai.

A source said, “Market demand for finished products has improved over the past few weeks, with some transactions being completed. Despite this progress, the market still cannot be deemed strong. Furthermore, ongoing price increases by leading coil manufacturers are currently driving up prices in the finished flat market.”

Recently, around 100 t of SS 304 CRC was heard traded at INR 189,000/t, ex-Mumbai.

Domestic finished longs’ (AOD grade) indicative levels

In the finished longs segment, 304 black round bars were priced at INR 180,000/t exw-Mumbai, while SS 304 bright bars were at INR 203,000-205,000/t exw-Mumbai. SS316 black round bars were offered at INR 285,000-290,000/t exw-Mumbai, and SS316 bright bars were priced at INR 315,000-320,000/t exw-Mumbai.

Scrap market insights

In the local market, prices of the 304 scrap were assessed at INR 121,000/t ex-Delhi NCR, on cash payment terms. Sources indicated that major mills are purchasing 304 scrap at approximately INR 124,000-126,000/t delivered (DAP), with a credit period of 45 days.

This week, imported scrap prices saw a marginal uptick due to a rise in inquiries for imported material, reflecting a market improvement. BigMint’s evaluation reported 304-grade scrap prices at $1,410/t CFR Mundra. Suppliers are quoting SS 304 scrap at $1,420-$1,430/t, while buyers’ bids range slightly lower at $1,390-$1,400/t.

The 316-grade scrap was priced at $2,600/t CFR Mundra, with some suppliers offering it at $2,620-$2,630/t. Buyers’ bids are currently at around $2,590/t.

Sources informed BigMint, the current sea freights from Thailand/Indonesia stand at $2,200-$2,400/20-foot container.

Additionally, SS 410 was at $660-$680/t CFR Mundra. Meanwhile, offers for SS Zurik scrap originating from the US ranged from $1,310-$1,370/t levels for SS content of 90-95%.

China market overview

During the week, China’s domestic stainless steel prices dipped marginally w-o-w. Prices of the 304 grade CRC reached RMB 14,550/t ($2,038/t) ex-works. Meanwhile, prices of 304 grade CRC stood at $2,108/t FOB.

In July 2024, China’s large-scale stainless steel enterprises produced 3.46 mnt of crude steel, up 3.2% m-o-m and 5.3% y-o-y. Series-wise bifurcation: 200 series at 1.06 mnt (down 0.7% m-o-m, 2.4% y-o-y), 300 series at 1.69 mnt (up 2.6% m-o-m, down 1.2% y-o-y), 400 series at 712,100 t (up 11.3% m-o-m, 45% y-o-y).

Global updates

Taiwan 300 series HRC prices rise due to Tsingshan

In July, Taiwan saw a significant drop in imports and exports of 300 series stainless steel hot-rolled coil. Imports fell 18.9% to 58,300 t, while exports plummeted 62.5% to 57 t, a new low since November. Prices surged, with import prices reaching an eight-month high of NT$62,000/t ($1,921/t) and export prices hitting a new high since last November.

Outokumpu eyes cost savings strategy

Outokumpu’s Q2 performance was solid, with improved profitability compared to Q1. Despite this, the CEO highlighted ongoing challenges in the European market and emphasized the need for enhanced cost competitiveness, especially in commodity stainless steel. They plan to optimize production in Finland and Germany, leveraging Nordic clean energy for cost savings.

Raw materials scenario

Ferro molybdenum: Indian ferro molybdenum prices continued its fall and dropped further by INR 53,000/t ($631/t) as compared to the previous assessment on 7 August. Limited inquiries prompted panic sales which resulted in the price drop.

As per BigMint’s assessment on 14 August, ferro molybdenum prices in India were INR 2,446,000/t ($29,141/t) exw-Nagpur on a 60% pro rata basis.

Ferro chrome: Indian ferro chrome prices (HC, FeCr60%) stood at INR 103,100/t exw-Jajpur, down by INR 1,800/t w-o-w.

Outlook

Stainless steel prices are expected to stay within a narrow range due to stable nickel prices. However, global nickel prices on the LME could experience short-term fluctuations in the near future.

Leave a Reply