Bangladesh’s imported ferrous scrap index witnessed a mixed trend w-o-w, mainly driven by a rise in offers for containerised shredded and HMS (80:20) from Europe. Offers in bulk moved slightly upwards from Japan due to JPY appreciation on the other hand US origin bulk scrap offers softened following falling scrap prices in recent deals into Turkiye. Although market activities improved as compared to last week bids continue to remain unchanged with a monsoon-affected steel sector.

Finished steel sales have been sluggish due to recent disruptions, but operations are set to return to normal.

- A supplier said, “No inquiries from the last 2-3 weeks from UAE origin HMS and PNS Mix offered at $425/t whereas pure PNS was offered at $438-440/t, US origin offers were around $405-410/t if we consider the freight rates per containers from US to Chattogram is currently at the level of $1100-1200.”

- A major trading house representative said, “Shipping lines are currently canceling bookings, raising questions about whether the Kanto scrap export tender booking to Bangladesh will proceed as planned amid these challenges. Additionally, there have been reports of recent sponge iron trades, suggesting buyers may be adjusting their bookings in anticipation of upcoming changes in trade conditions.”

Changes in assessment prices:

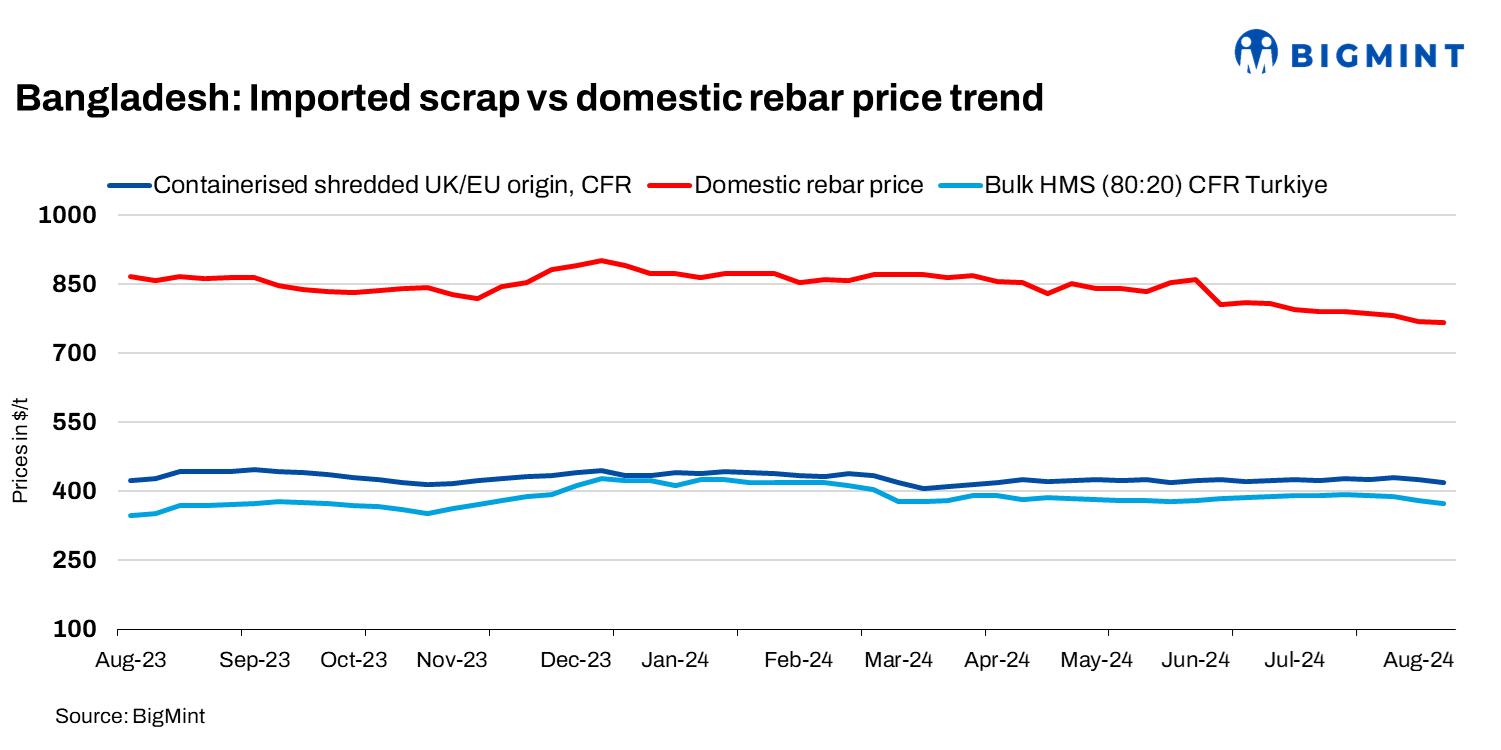

- BigMint’s assessment of Europe-origin containerised shredded remains largely stable with $1-2/t fluctuation w-o-w and stood at $420/t, while HMS (80:20) prices stood at $400/t (declined by $5/t w-o-w).

- BigMint’s latest weekly assessment shows US-origin HMS (80:20) bulk prices decreasing by $5/t t0 $403/t CFR Chattogram.

- BigMint’s weekly assessment for Japan-origin H2 bulk price shows an increase of $1/t w-o-w at $405/t CFR Chattogram.

Japanese H2 was offered at $405-408/t, with bids at $395-398/t. US offers included HMS (80:20) mix at $405/t and shredded at $412-414/t.

UAE-origin HMS 1 was offered at $425-428/t Indicative prices from the UK/EU showed shredded at $420-422/t.

Confirmed deals

Around 500 t of Brazil-origin HMS (80:20) was booked at $410/t CFR Chattogram.

- As per another market participant, Bangladesh’s scrap market started moving, with recent sales including US Shredded at $413/t, New Zealand Shredded at $430/t, and Australian Shredded at $425/t, along with Chile HMS 80:20 at $397/t. The preferred price for Australian Shredded in Bangladesh is $425-430/t, reflecting a $10 premium over India ($415-420/t).

Domestic market overview

Domestic rebar prices remain range-bound amid a slow-moving steel market to BDT 86,000-87,500/t exw-Dhaka and BDT 91,000-91,500/t exw-Chattogram, with workable levels for billets at BDT 72,000/t and offers at BDT 74,500/t. Ship plate scrap ex-Chattogram yard was heard at BDT 71,500-72,000/t exy and HMS scrap at BDT 60,000-60,800/t exy.

- According to a major steel mill in Dhaka, market sentiment is currently down. However, an improvement in market activities is anticipated once the banking sector and financing facilities are streamlined following the new government formation. Currently, rebar prices in Dhaka are at BDT 87,500/t, with a BDT 3,000-3,500/t premium in Chattogram.

Amid nationwide protests disrupting economic activities, Bangladesh’s electricity demand surged by 7%, with households using more power to combat the heat. Average daily demand hit 316 million kilowatt-hours, driven primarily by residential use, unlike other developing Asian nations where industrial consumption prevails. As a result, Bangladesh has increased thermal coal imports by 26.6% this year, with coal-fired power generation nearly tripling.

Outlook: The market is expected to recover soon, supported by strong backing from the trader-mill community following the formation of the new interim government. Although the process of opening Letters of Credit (LCs) is currently slow, banks are anticipated to resume normal LC operations next week.

Leave a Reply