- India sees 42% m-o-m decline in tonnage secured

- Pakistan’s volume rises 71% m-o-m, drops 86% y-o-y

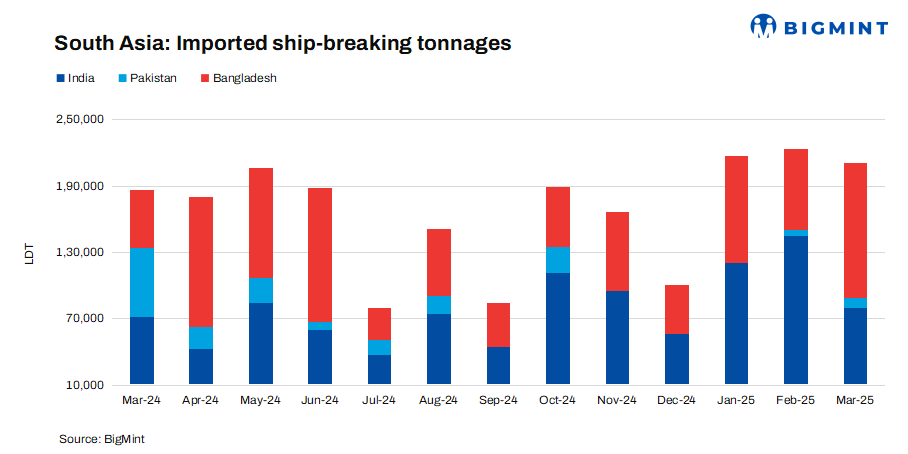

South Asia’s ship-breaking markets witnessed a mixed performance in March 2025. Facing competition and tight supply, India saw a decline in tonnage, while Bangladesh experienced growth, taking the lead despite economic challenges and regulatory concerns. Meanwhile, Pakistan saw limited tonnage arrival, though it was higher m-o-m.

India: In March 2025, India’s ship-breaking sector secured 83,934 light displacement tonnes (LDT), falling by 42% from February’s 144,683 LDT. However, this marked a sharp rise of 16% from March 2024’s 72,056 LDT.

The Alang ship-breaking yard also saw a decrease in arrivals m-o-m, receiving 10 vessels for recycling in March, one less than in February.

India’s ship recycling market faced challenges throughout the month, with Alang facing growing competition from Pakistan and Bangladesh. Limited vessel supply, declining steel prices, and currency volatility kept buyers cautious, allowing Pakistan to surpass Alang in regional rankings.

Towards the month-end, ship-breaking prices saw a slight uptick due to higher domestic steel rates and speculation over duty changes, but vessel shortages stalled sales. With tight supply and subdued demand, the market remained under pressure, showing no clear signs of recovery.

Pakistan: Only a small tonnage of around 20,572 LDT arrived in March 2025, marking a slow start for Pakistan’s ship recycling sector in 2025 but a rise of four-fold from 5,204 LDT in February. Additionally, this reflects a sharp decline of 67% from the 62,339 LDT recorded in March 2024. Notably, only one ship was recycled in March 2025.

Pakistan’s ship recycling market remained sluggish, with Gadani struggling to secure tonnage despite briefly gaining competitiveness as India’s market weakened. Some deals for small LDT vessels were concluded, but vessel supply remained tight, and financing constraints limited buying. The lack of Hong Kong Convention (HKC) compliance kept shipowners cautious, while falling steel prices and a record-low PKR added further pressure.

Despite some interest from buyers, deals were slow to materialise, as recyclers held back, expecting better pricing. Many focused on HKC facility upgrades, but with no major progress, Pakistan risks falling behind regional competitors. Rising Indian offers and weak local demand also weighed on sentiment.

Bangladesh: In March 2025, Bangladeshi recyclers processed approximately 164,208 LDT, marking a nearly two-fold rise from the 73,989 LDT recycled in February 2025. This also reflected a nearly three-fold jump compared to the 51,968 LDT recorded in March 2024.

Thirteen ships were recycled during the month, six more than in February, indicating an increase in m-o-m performance.

Bangladesh took the lead in ship recycling, supported by strong domestic steel prices and steady vessel arrivals. Over 100,000 LDT reached Chattogram, keeping yard operations stable despite tightening supply. However, economic challenges, including a weakening taka and high inflation, raised concerns over long-term price stability.

Demand from recyclers remained strong, but political instability and stricter banking controls added uncertainty. Very large crude carriers (VLCCs) listed on the Office of Foreign Assets Control (OFAC) were denied entry, highlighting regulatory risks. With Ramadan approaching and a 31 March deadline for yard upgrades, activity is expected to slow, though rising prices suggested some deals might close before the break.

Leave a Reply