- Indian buyers resist high imported scrap offers

- Turkiye in wait-and-see mode amid trade policy uncertainties

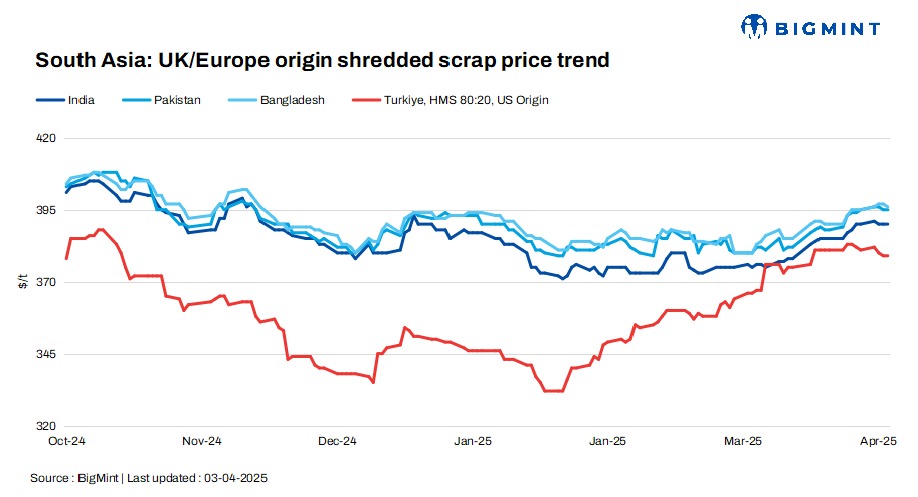

South Asia’s imported scrap markets remained sluggish as buyers held back amid pricing concerns, liquidity constraints, and post-holiday slowdowns. In India, resistance to high offers kept trade minimal, while Pakistan’s market stayed muted due to Eid-related inactivity and LC challenges.

Bangladesh saw limited movement, with stable prices but weak demand, and uncertainty over HKC compliance weighed on ship recycling.

Meanwhile, Turkiye’s market remained in limbo, with buyers and sellers waiting for clarity on trade policies and currency fluctuations.

UK-origin shredded scrap offers remained unchanged in India and Pakistan but edged down by $1/t d-o-d in Bangladesh. US-origin bulk HMS 80:20 offers to Turkiye also remained unchanged.

Overview

India: India’s imported scrap market remained sluggish as buyers resisted high prices, expecting further declines. Shredded scrap was offered at $390-400/t CFR, but buying interest was capped at $385-386/t, limiting deals. UK-origin HMS 80:20 was available at $365-370/t CFR, while UK Turning was offered at $345/t CFR.

A bulk deal from Japan to Chennai at $385-390/t was heard last week, but overall demand remained weak. With buyers hesitant to commit at current levels, market activity stayed subdued.

Pakistan: Pakistan’s imported scrap market stayed quiet as buyers remained inactive during the Eid holidays. The UK/EU-origin shredded scrap was offered at $395-400/t CFR Qasim, but buyers aimed for $390-395/t. Mills operated at reduced capacity due to liquidity constraints and LC challenges, keeping trade minimal. While inquiries are expected to revive by mid-week, elevated global scrap prices and economic uncertainty may limit a swift recovery in demand.

Bangladesh: Bangladesh’s imported scrap market remained quiet post-Eid, with buyers staying on the sidelines and LC constraints restricting trade. Prices were largely stable, with European HMS at $370-375/t and US HMS at $380-384/t CFR.

Domestic ship scrap and rebar prices held steady, while uncertainty over HKC compliance pressured the ship-recycling sector.

Market activity is expected to remain slow until mid-April, with only a gradual recovery anticipated as mills resume operations next week and assess demand.

Turkiye: The Turkish imported scrap market remained quiet as buyers and sellers awaited key trade policy developments. US-origin HMS (80:20) held steady at $379/t CFR, with no fresh deals reported. Turkish mills were largely inactive, having already secured sufficient scrap for April and early May shipments.

Market participants noted uncertainty due to the ongoing US tariff discussions and euro volatility. While European recyclers sought higher prices, Turkish buyers bid as low as $365/t, but no supplier accepted such levels. The market remained in a holding pattern with limited activity.

Price assessments

India: UK-origin shredded indicatives were assessed at $390/t CFR Nhava Sheva, unchanged d-o-d.

Pakistan: UK-origin shredded indicatives remained unchanged d-o-d $395/t CFR Qasim.

Bangladesh: UK-origin shredded indicatives edged down by $1/t d-o-d to $396/t CFR Chattogram.

Turkiye: US-origin HMS (80:20) bulk scrap prices were assessed stable d-o-d at $379/t CFR Turkiye.

Leave a Reply