Today, the South Asian ferrous scrap market exhibited a mixed trend. Indian buyers remained inactive due to price disparities and cost-effective alternatives in the domestic market. The markets in Pakistan and Bangladesh slowed down due to LC processing issues and a sluggish domestic steel market.

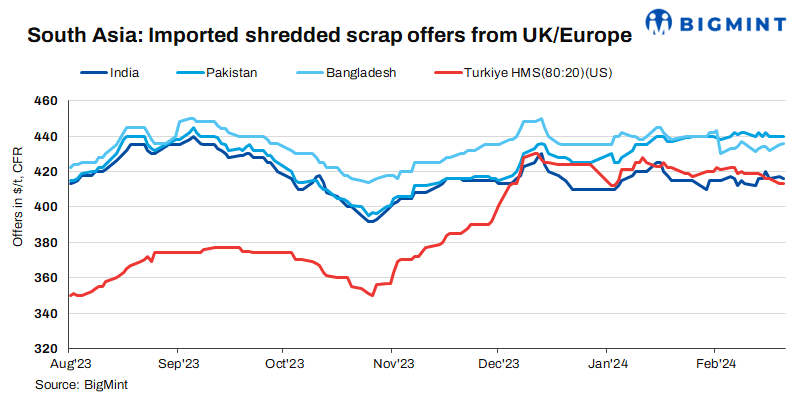

Shredded scrap offers decreased by $1/t in India, remained unchanged in Pakistan, and increased by $1/t in Bangladesh. Bulk US HMS (80:20) scrap prices to Turkiye also remained flat d-o-d.

Market overview

India: In India, imported scrap buyers are cautious due to cost-effective alternatives available in the domestic market and sluggish domestic steel sales. Shredded scrap from Europe is being offered at $415-420/t CFR Nhava Sheva, while HMS (80:20) prices are $390-395/t CFR.

Buyers aim for shredded scrap at $400-405/t CFR and HMS at $380-385/t CFR.

A representative from a trading company said, “India’s market is quiet due to multiple reasons. Local scrap is available at a lower price, and for suppliers the price of scrap in their respective markets is more attractive compared to exports. Additionally, there is very poor sales of finished steel.”

As per market participants, no specific deals were reported but customers suggest a price of around $405/t for shredded scrap. Suppliers are offering shredded scrap from Europe at $420-422/t and Australian suppliers are offering at $425/t, while bids stand at $405/t and $410/t. However, HMS is struggling to gain traction at $400/t, with reports of deals involving old imported material below market rates by $10-15/t.

Pakistan: In Pakistan, market activities remained average as buyers encountered difficulties in opening LCs, leading to delay in payments. Shredded scrap offers from Europe and the Middle East were at $435-445/t CFR Qasim. HMS 1 offers from Kuwait were at $415-420/t CFR Qasim, while sheared HMS offers from the Middle East stood at $425/t CFR and fabrication at $440/t CFR.

An official from a steel mill said, “Bookings have declined due to LC-related issues resurfacing as a major problem. Post-election, banking operations also remain unsupportive.” Another official added, “Document approval is being delayed due to a weaker forex situation, IMF negotiations, and decreased foreign investment in January.”

In the domestic market, local scrap prices were approximately at PKR 155,000-160,000/t ($554-572/t) ex-Karachi and PKR 173,000-180,000/t ($619-644/t) ex-Punjab. Rebar was assessed at PKR 255,000-260,000/t ($912-930/t) ex-Karachi and Punjab, while billets were reported at PKR 230,000/t ($823/t) ex-Punjab.

Bangladesh: In Bangladesh, the pace of imported scrap buying slowed down due to a sluggish domestic steel market. Indicative offers for shredded scrap from Europe were at $435-440/t CFR Chattogram, while HMS (80:20) stood at $415-420/t CFR. From Australia, offers for shredded scrap were heard at $420-425/t CFR, and for HMS (80:20), they were around $410-412/t CFR.

In the domestic market, local HMS scrap prices were reported at BDT 61,000-62,000/t ($556-565/t), while rebars were assessed at BDT 85,000-87,000/t ($775-793/t) ex-Dhaka and BDT 94,000-95,000/t ($857-966/t) ex-Chattogram. Billet prices were noted in the range of BDT 75,000-76,000/t ($683-692/t).

Turkiye: Turkish deepsea import ferrous scrap prices remain stable for HMS (80:20) assessed at $413/t CFR, unchanged from yesterday. Turkish mills remained cautious due to a slowdown in domestic rebar sales and anticipated softer scrap prices. Turkish exported rebar fell to $608/t FOB. Lower HMS collection costs in the Benelux region contributed to expectations of reduced scrap prices, with offers targeted at $410/t CFR and above. Despite the decline, EU sellers aimed for $418-420/t CFR, mindful of potential short positions in the market. The market remained cautious amid fluctuating demand and bearish sentiments from futures traders, awaiting further clarity on US domestic settlements in March, which could potentially push scrap prices below $400/t CFR.

Recent deals

- Around 500 t of PNS scraps were booked from Peru at $428/t CFR Chattogram.

- A parcel of 500-t PNS scraps were sourced from Malaysia at $435-440/ CFR Chattogram.

- Approximately 250-t of turning boring scraps were booked from the US at $345/t CFR Nhava Sheva.

- A small parcel of 250 t of HMS (80:20) scraps were procured from Central America at $387/t CFR Nhava Sheva.

- Around 500 t of shredded scraps were booked from Europe at $443/t CFR Qasim.

- Approximately 500 t of shredded scraps were booked from Belgium at $437/t CFR Qasim.

- About 500 t of HMS scraps were booked from UAE at $410/t CFR Qasim.

- Around 250-260 t of turning boring scraps were sourced from UAE at $375/t CFR Qasim.

Price assessments

India: UK-origin shredded scrap indicatives were assessed at $416/t CFR Nhava Sheva, down by $1/t d-o-d.

Pakistan: UK-origin shredded scrap indicatives were assessed unchanged at $440/t CFR Qasim.

Bangladesh: UK-origin shredded scrap prices were assessed at $436/t CFR Chattogram, up by $1/t.

Turkiye: US-origin HMS (80:20) bulk prices were assessed at $413/t CFR Turkiye, unchanged d-o-d.

Outlook

Imported scrap offers in the South Asian market are expected to stay range-bound, with fluctuations of approximately plus or minus $5/t due to prevailing market sentiments. Indian buyers are adopting a firm stance and are inclined to procure imported scrap only when it becomes financially viable. Currently, there exists a minimum gap of $20/t between domestic and imported scrap prices.