In Pakistan, market activity remained moderate in terms of fresh inquiries due to challenges in LC processing and subsequent payment delays. Shredded scrap offers from Europe and the Middle East ranged between $435-445/t CFR Qasim, while HMS 1 offers from Kuwait were around $415-420/t CFR Qasim.

Additionally, Yemen-origin LMS Bundles are available at $350/t (shipment within 14-21 days).

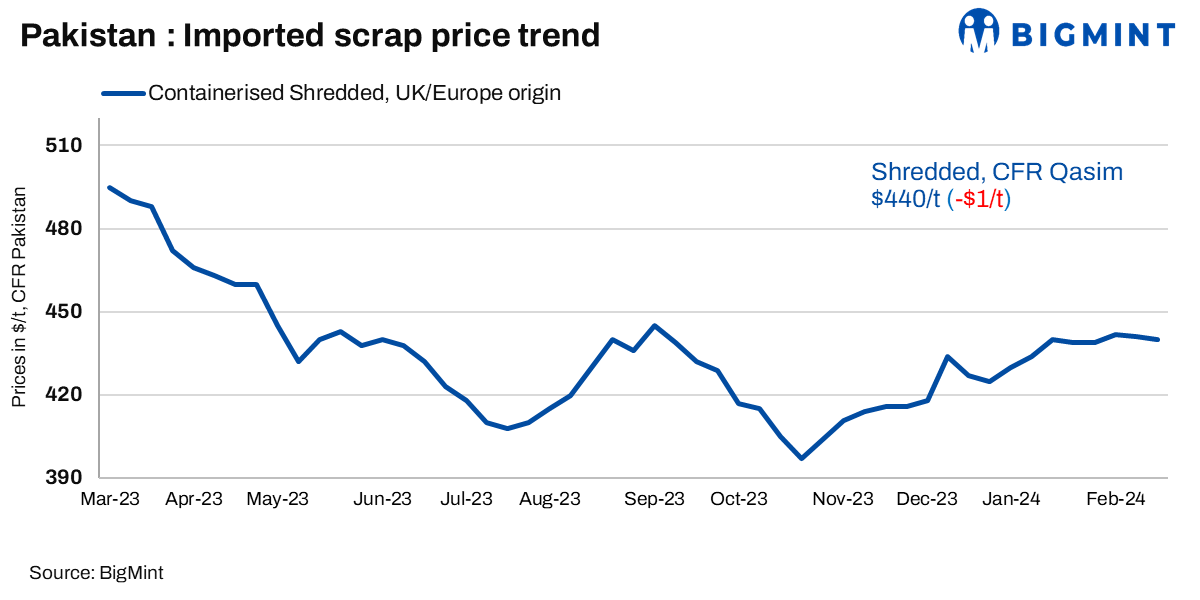

Current rates for US/Europe origin shredded stand at $438-442/t CFR Qasim, while HMS from the UAE is offered at $420/t.

BigMint’s assessment for European-origin shredded stood at $440/t slightly dropped by 1/t w-o-w.

A trader source mentioned, “Bookings have been declined due to LC-related issues, exacerbated by unsupportive banking operations post-election.”

As per market participants, document approvals face delays amidst forex volatility, IMF negotiations, and decreased foreign investment in January, impacting steel companies for further imported inquiries.

As per a mill-side source, “Market sluggishness persists due to delayed LCs and payments, and a slightly unstable market environment, both domestically and internationally, despite notably low rebar sales.”

Recent deals:

- Around 500 t of shredded scraps were booked from Europe at $443/t CFR Qasim.

- Approximately 500 t of shredded scraps were booked from Belgium at $437/t CFR Qasim.

- About 500 t of HMS scraps were booked from UAE at $410/t CFR Qasim.

- Around 260 t of turning boring scraps were sourced from the UAE at $375/t CFR Qasim.

- Around 250 t Brazil-origin LMS booked at $385/t on a CFR Qasim basis.

- Around 250 t Brazil-origin busheling scrap was booked at $445/t on a CFR Qasim basis.

- Approximately 1,400 t Kuwait-origin HMS 1 was booked at $420-425/t range on a CFR basis.

- A parcel of 500 t of Europe-origin shredded was booked at $439/t on a CFR Qasim basis.

- Another 1000 t of UK-origin shredded was booked at $444/t on a CFR Qasim basis.

Domestic market: In the domestic market, local scrap offers and indicatives were reported at PKR 155,000-175,000/t on an exw basis ($554-626/t) for exw-Karachi and an exw-Punjab basis, respectively. Similarly, rebar offers were heard at PKR 255,000-270,000/t($912-966/t) on an exw basis, whereas billet offers were heard at PKR 229,000-230,000/t($819-823/t) on an exw basis.

According to a steel mill representative, the current domestic market conditions are slightly subdued, with anticipation for improvement post-the-winter season. Finished steel sales continued at a moderate pace, with prices ranging from PKR 260,000/t to 268,000/t on an exw basis, consistent with previous reports of a downward trend.

Foreign direct investment (FDI) in January saw an inflow of $184.7 million, but outflow amounted to $357.9 million, resulting in the net outflow. For the July-January period of FY’24, FDI totalled $689.5 million, down by 21.4% compared to the same period last fiscal year, representing a loss of $187.3 million.

Despite a marginal increase of $13 million in reserves, reaching $8.056 billion, uncertain political and economic conditions have hindered Pakistan’s ability to raise dollars from international markets. The economy’s projected 2% GDP growth in FY’24, while an improvement over the previous year’s contraction, falls short of the country’s needs, potentially exacerbating unemployment and revenue challenges.

Power generation cost surge: In January 2024, Pakistan experienced a 23% increase in the cost of power generation compared to the same period last year. This surge, with the average cost reaching PKR 13.8/KWh, was primarily driven by higher costs of power generation from gas, nuclear, and Furnace Oil (FO) sources.

On a monthly basis, power generation increased by 9% compared to December 2023. During the first seven months of fiscal year 2024, power generation saw a slight uptick of 0.14% y-o-y reaching 77,200 GWh.

In terms of power sources, coal emerged as the leading contributor, accounting for 23.4% of the generation mix, followed by nuclear (20.8%) and RLNG (18.2%). Renewable sources, including wind, bagasse, and solar, collectively contributed 3.4% to the generation mix.

Currency rate: On Tuesday, the Pakistani rupee slightly weakened against the US dollar by 0.08%, closing at PKR 279.57 in the inter-bank market, down by PKR 0.21 compared to the previous day’s close of PKR 279.36, according to the State Bank of Pakistan.

Outlook: Delays in LC approval pose a potential threat to imported scrap volume, according to sources from several mills. The political uncertainty has significantly heightened concerns regarding both the economic and political trajectory of the country during the last month.