- Indian buyers retreat amid weak finished steel demand

- Pak faces slow post-Eid sales, capacity underutilisation

South Asia’s imported scrap market witnessed a notable slowdown across key regions, driven by weak post-holiday demand, volatile global cues, and persistent economic constraints.

In India, subdued finished steel demand, a weakening rupee, and fears of Chinese dumping pressured imported scrap interest, while Pakistan grappled with sluggish post-Eid sales and capacity underutilisation, prompting mills to avoid fresh bookings. Bangladesh remained largely inactive as letter of credit (LC) issues and tight forex reserves limited buying, despite stable domestic rebar prices.

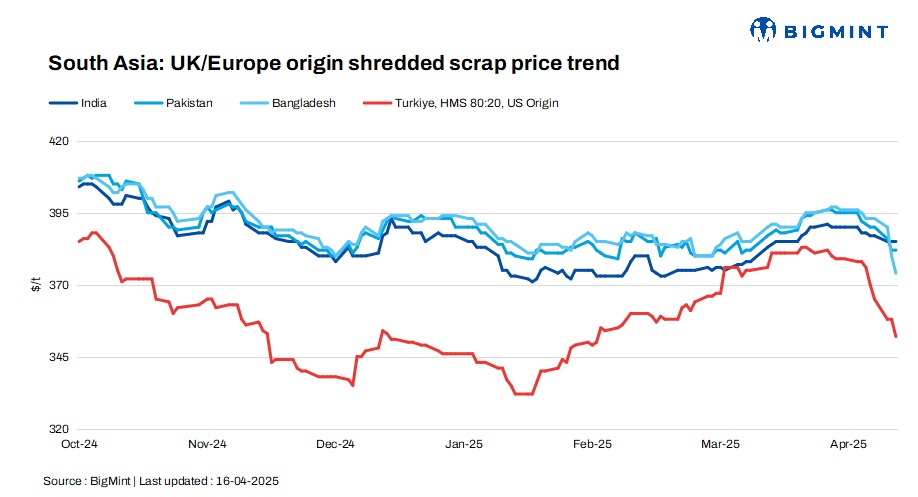

In South Asia, prices of UK-origin shredded fell $1/t d-o-d in Bangladesh, while they remained unchanged in India and Pakistan.

Meanwhile, US-origin HMS (80:20) bulk prices in Turkiye dropped steeply by $6/t d-o-d. Notably, imported scrap prices have been declining in Turkiye over the past couple of days. Declining bulk scrap prices and deal-to-deal variability added further uncertainty to the region’s sentiment, casting a shadow over near-term market direction.

Overview

India: India’s imported scrap market turned sluggish as buyers pulled back amid weakening domestic steel demand, forex volatility, and a softening Turkish market. Containerised shredded offers were at around $380-385/t but received minimal counters. Australian HMS (80:20) was booked at $362-363/t, while UK sheared HMS traded at $350-355/t CFR.

A wide bid-offer gap persisted, as buyers targeted below $380/t for shredded scrap.

Falling domestic rebar prices and rising sponge iron usage also dented demand. Additionally, a weakening rupee and fears of cheap Chinese steel imports kept sentiment subdued, with many mills opting to wait rather than commit to fresh bookings.

Pakistan: Pakistan’s imported scrap market slipped further as weak post-Eid demand, slow steel sales, and global price corrections kept sentiment under pressure.

Shredded from the UK/Europe dropped to $380-385/t CFR Qasim, with bids lagging near $375-378/t. Falling Turkish scrap prices and subdued Chinese steel offers added to bearishness.

Domestic scrap remained tight, but rebar sales stayed sluggish, with mills operating at just 30-40% capacity and rebar prices ranging between PKR 232,000-250,000/t depending on region and payment terms.

Most mills stayed cautious, avoiding fresh bookings and opting to wait for clearer signals from demand recovery or potential policy support.

Bangladesh: Bangladesh’s imported scrap market remained weak, with limited activity as buyers stayed on the sidelines amid ongoing LC restrictions and tight forex conditions. Bulk offers from the US disappeared due to volatile Turkish pricing, while Australian-origin bulk was floated at $375-380/t CFR but saw little response.

Japanese bulk offers hovered at around $360-365/t CFR, but suppliers showed reluctance to reduce prices further.

Containerised HMS (80:20) from the Dominican Republic was offered at $355-360/t CFR Chattogram.

Mills showed more interest in domestic scrap, supported by stable rebar prices in the BDT 82,000-86,000/t range.

Turkiye: The Turkish imported scrap market was subdued, with US-origin bulk HMS 80:20 offers at $352/t CFR, down by $6/t d-o-d, amid growing uncertainty and sluggish buying appetite. Notably, two deep-sea EU-origin scrap deals were heard to have been concluded at $348/t and $335/t CFR, marking a decrease of $10-15/t compared to the last deal, signalling rising buyer-to-buyer variation.

Price assessments

India: UK-origin shredded indicatives were assessed unchanged d-o-d at $385/t CFR Nhava Sheva.

Pakistan: UK-origin shredded indicatives stood at $382/t CFR Qasim, unchanged d-o-d.

Bangladesh: UK-origin shredded indicatives edged down by $1/t d-o-d to $389/t CFR Chattogram.

Turkiye: US-origin HMS (80:20) bulk scrap prices decreased by $6/t d-o-d to $352/t CFR Turkiye.

Leave a Reply