- Weak nickel spurs 300 series price cut

- Chinese portside NPI prices decline

Prices of Indian stainless steel (SS) finished flat products decreased w-o-w, following recent price cut by a major coil manufacturer and weak finished demand. Meanwhile, long product prices also saw a similar trend amid subdued market sentiments.

Recently, India’s leading stainless steel coil manufacturer reduced tags of its 300 series effective 13 April, following a drop in prices of nickel which plunged nearly 5-year low, a key raw material. Consequently, prices of 304 and 316 HRCs were cut by INR 3,000/t ($34/t), while CRC tags were reduced by INR 2,000/t ($23/t). Notably, this marks the first price revision in April 2025.

However, LME nickel prices rebounded towards the end of last week and have continued to rise consecutively this week, likely in response to the 90-day suspension of reciprocal tariffs.

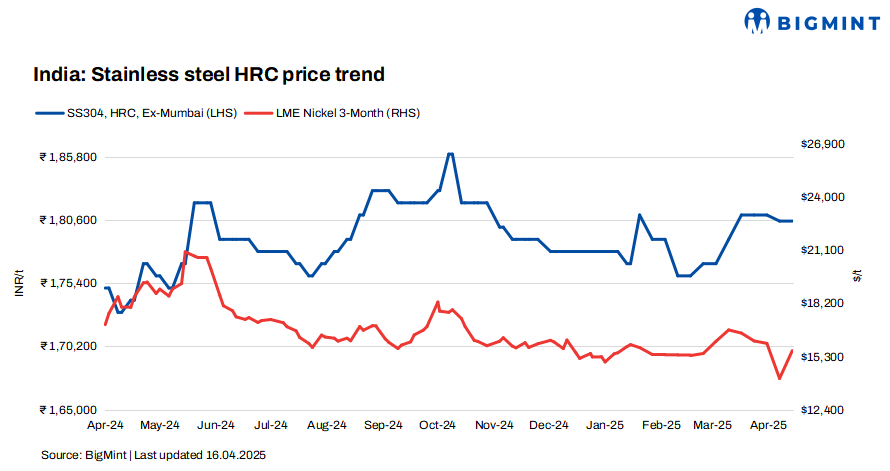

BigMint’s benchmark assessment for stainless steel (304 series) hot-rolled coils (HRCs) stood at INR 180,500/tonne (t), stable w-o-w, while 304L (25-100 mm) black round bars also dropped by INR 1,000/t to INR 159,000/t, both ex-Mumbai.

LME nickel tags up, Asian NPI fell w-o-w

At the time of reporting, three-month LME nickel prices stood at $15,655/t, reflecting an increase of 10% from last week’s $14,145/t. Nickel stocks in LME-registered warehouses stood at 202,818 t, range-bound compared to 202,938 t in the previous week.

Chinese portside prices of nickel pig iron (NPI) (grade 13%>Ni>10%) witnessed a w-o-w decrease of RMB 25/metric tonne unit (mtu) ($3/mtu) to RMB 1,000/mtu ($136/mtu). Meanwhile, Indonesian FOB prices of NPI (grade 13%>Ni>10%) stood at $118/mtu, down by $3/mtu w-o-w.

Finished market dips w-o-w

According to market participants, “Market activity right now is mainly driven by need-based procurement, with buyers avoiding large orders. The seasonal slowdown due to summer conditions has further reduced purchasing momentum. The decline in flat prices is a direct reflection of the drop in major coil makers’ prices.”

As per BigMint’s assessment, SS 316 HRCs dropped by INR 2,000/t w-o-w to INR 321,000-323,000/t ex-Mumbai.

BigMint’s assessment of SS 316L (25-100 mm) black round bars stood at INR 267,000-269,000/t ex-Mumbai, down INR 2,000/t w-o-w. Prices of SS 316L (25-100 mm) bright bars stood at INR 286,000-288,000/t ex-Mumbai, down by INR 2,000/t w-o-w.

Another source mentioned, “There’s been no significant positive change in the current market. IF route mills continue to express dissatisfaction with the state of the stainless steel market. Despite fluctuations on the LME, the local market remains largely unaffected. Buyers can expect short-term price stability, but they should remain cautious due to sluggish consumption trends.”

Chinese stainless steel prices steady

In China, prices of domestic stainless steel 304-grade cold-rolled coils (CRCs) stood at RMB 14,050/t ($1,920/t) exw, stable w-o-w, while FOB tags of 304-grade CRCs were at $1,910/t.

Global market updates

Global SS output hits peak in CY’24: According to the World Stainless Association, global stainless steel melt shop production touched a record 62.6 mnt in CY’24, marking a 7% y-o-y increase. This milestone represents the highest production ever recorded. The CAGR from 2015 to 2024 was recorded at 4.8%.

Nickel prices up amid dollar weakness: Nickel prices rose, driven by a weaker US dollar, US tariff adjustments, and improved market sentiment. The March Producer Price Index (PPI) in the US increased by 2.7%, while China’s strong export performance further supported the upward trend. However, high refined nickel inventories may create short-term price strength and potential volatility.

Raw materials overview

Ferro molybdenum: Indian ferro molybdenum prices edged down by INR 15,000/t ($175/t) in comparison to the previous assessment on 9 April. This decline followed a drop in global prices, especially in China.

As per BigMint’s assessment on 16 April, ferro molybdenum prices in India were at INR 2,553,000/t ($29,808/t) exw on a 60% pro rata basis.

Ferro chrome: Indian high-carbon ferro chrome (HC60%, Si:4%) prices were at INR 100,700/t ($1,175/t) exw-Jajpur, range-bound w-o-w.

Additionally, at Vedanta-FACOR’s ferro chrome auction on 14 April, the bigger lot of 10-150 achieved an H1 price of INR 100,100/t exw, above the base price of INR 99,700/t. Bids also went up by INR 1,400/t from the previous 21 March auction. The price gain was likely influenced by improved domestic demand and a recent rise in Chinese tender and spot prices, leading to more active bidding.

Outlook

Buyers can expect price stability in the near term, but should remain cautious as sluggish consumption and weak demand for finished goods continue to limit the overall market momentum.

Leave a Reply