- Middle East tensions raise risks for key shipping routes

- Indonesian nickel smelters face sulphur supply risks from imports

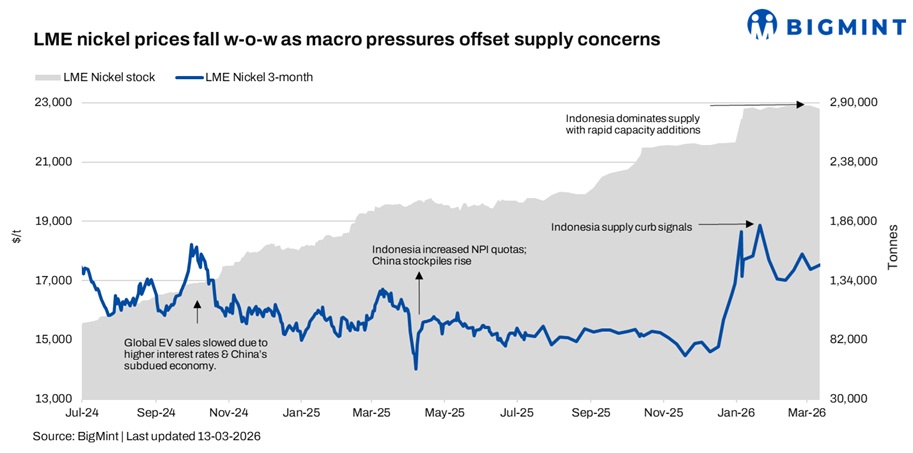

Nickel prices on the London Metal Exchange remained relatively firm in the week ended 13 March, supported by geopolitical uncertainties and tightening inventories. The LME three-month nickel contract closed at $17,530/t, slightly higher compared with $17,385/t in the previous week.

Meanwhile, LME warehouse inventories declined by around 1% w-o-w to 284,658 t, compared with 287,550 t in the previous week, indicating steady physical demand and limited supply inflows.

On the macroeconomic front, geopolitical tensions intensified during the week following renewed conflict risks in the Middle East and concerns over potential disruptions to key shipping routes. Rising uncertainty in global trade flows has continued to influence sentiment across base metals markets.

In addition, stronger US economic indicators weighed on non-ferrous metals. US ADP employment data showed job growth of 63,000 in February, exceeding market expectations and reinforcing expectations that the Federal Reserve may maintain a cautious monetary policy stance. The stronger labour data supported the US dollar index, which in turn exerted pressure on base metal prices including nickel.

Macro matters

Harita nickel operations face scrutiny

Harita Group, a major Indonesian nickel producer, reportedly removed key information regarding the capacity of coal-powered facilities supporting its nickel operations after concerns were raised with the Singapore Exchange (SGX). Environmental group Market Forces stated that earlier disclosures indicated about 910 MW of coal-based power capacity supporting processing activities on Obi Island. The revision has raised concerns over transparency as Indonesia’s rapidly expanding nickel processing sector continues to rely heavily on captive coal power for energy-intensive smelting operations.

Hormuz risks threaten sulphur supply for Indonesian smelters

Indonesia’s nickel processing industry is also facing potential raw material risks as escalating tensions in the Middle East raise concerns over possible shipping disruptions through the Strait of Hormuz. Sulphur—an essential input used in the High-Pressure Acid Leach (HPAL) nickel refining process—is largely imported, with a significant share sourced from the Middle East. Indonesian smelters typically maintain limited sulphur inventories, meaning prolonged disruptions in regional shipping routes could gradually tighten supply and affect nickel processing operations.

Outlook

Nickel prices are likely to remain supported in the near term amid continued geopolitical uncertainties and tightening raw material supply conditions. However, stronger US dollar movements and cautious global demand trends may limit sharp upside in the LME nickel market. Supply developments in Indonesia, particularly related to ore availability and raw material logistics, will remain key factors influencing price direction in the coming weeks.

Leave a Reply