- LME aluminium rises 3% w-o-w on Middle East supply risks

- Lower inventories and Qatalum output cuts tighten aluminium market

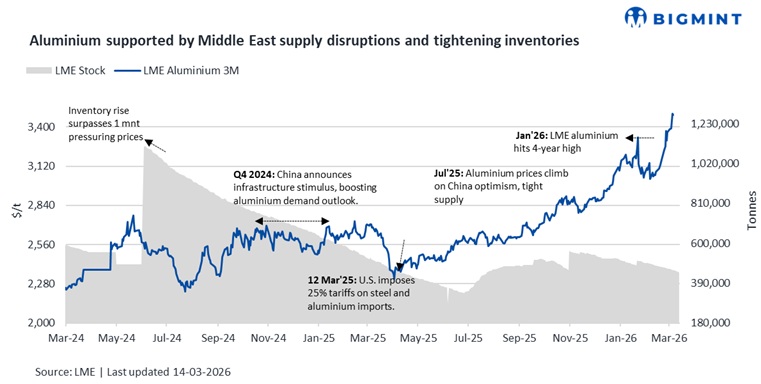

Benchmark aluminium prices on the LME increased by 3% in the week ended 13 March 2026, supported by rising geopolitical tensions and supply-chain disruptions, which intensified concerns over global aluminium supply.

Pricing, inventory trends

LME aluminium prices averaged $3,440/t during the week, increasing by $99/t or 3% w-o-w. Prices opened the week near $3,387/t, strengthened to around $3,444/t mid-week, and closed at $3,486/t.

Meanwhile, LME aluminium inventories declined 2% w-o-w to 445,300 t from 454,625 t, indicating tightening exchange stocks and providing additional support to prices.

Factors impacting prices

LME aluminium prices strengthened last week, averaging around $3,440/t, up $99/t or 3% w-o-w, supported by tightening supply expectations and heightened geopolitical risks. Prices moved higher through the week, opening near $3,387/t and closing around $3,486/t, as market participants reacted to disruptions affecting global supply chains.

The rally was largely driven by supply concerns in the Middle East, where gas supply constraints forced Qatar’s Qatalum smelter to operate at reduced capacity, limiting aluminium output. At the same time, shipping delays across Gulf trade routes raised concerns over potential disruptions in metal shipments, further tightening near-term supply expectations.

Additional support came from declining LME inventories, which fell 2% w-o-w to around 445,300 t, highlighting tightening exchange stocks. The market also shifted into backwardation, reflecting stronger spot demand relative to forward supply.

With geopolitical tensions, logistical disruptions, and constrained production capacity influencing market sentiment, aluminium prices remain sensitive to supply-side developments, suggesting continued volatility in the near term.

Outlook

Aluminium prices are likely to remain firm in the near term as geopolitical tensions and supply-chain disruptions continue to embed a supply-risk premium in the market, while LME inventories declined 2% w-o-w to 445,300 t. Ongoing constraints, including reduced output at Qatar’s Qatalum smelter and shipping delays across Gulf trade routes, may keep supply tight and support prices near recent highs. However, any easing in regional tensions or improvement in logistics could limit further gains, with markets closely tracking inventory trends and developments in Middle East supply routes.

Leave a Reply