- HRC exports surge 77% on pre-emptive restocking by EU

- Low prices, geopolitical factors lift billet exports by 80%

- India reduces HRC imports by 38%, finished flats down 28%

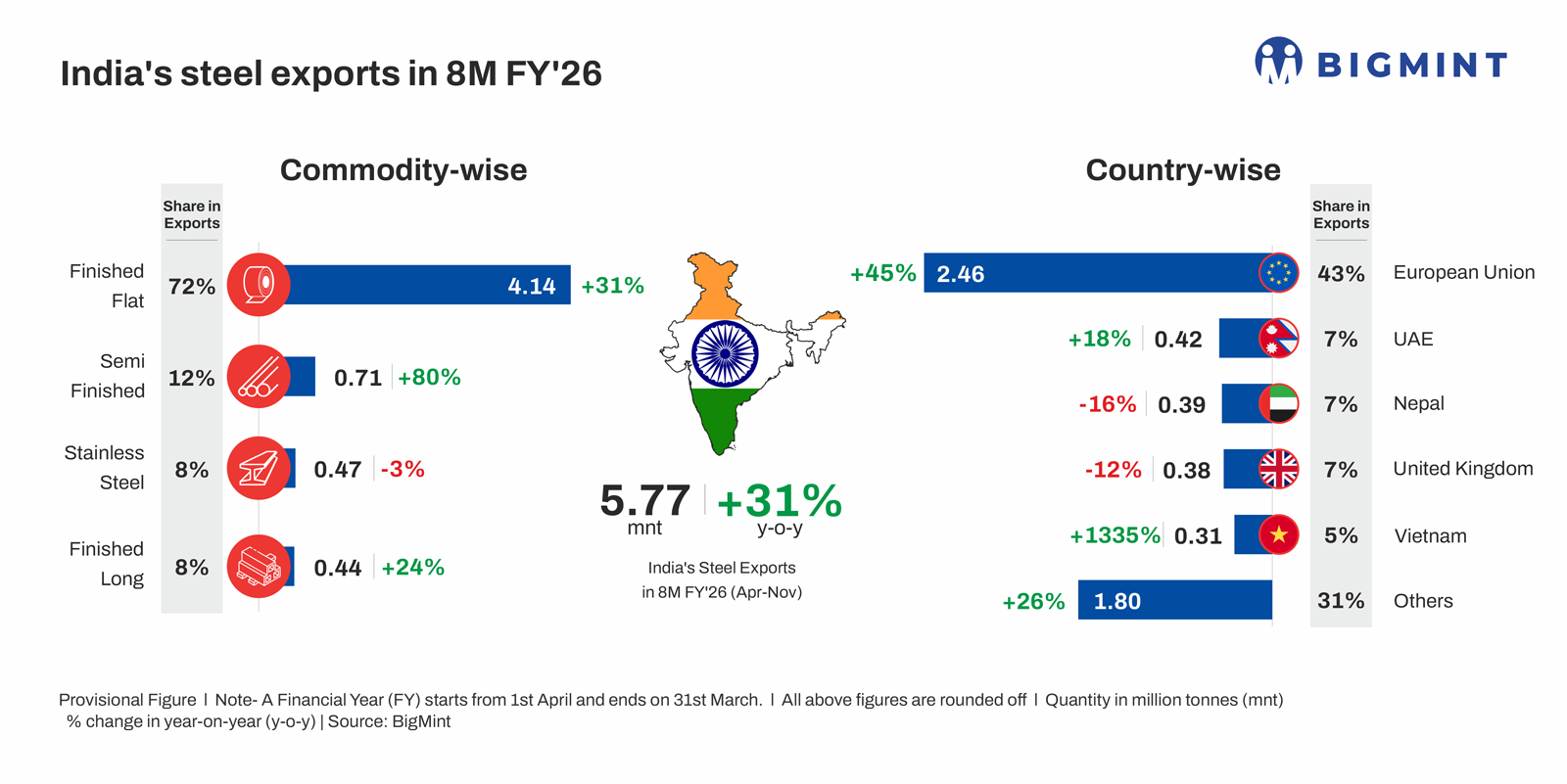

Morning Brief: India’s steel exports (including stainless steel) climbed up by a strong 31% y-o-y to 5.77 million tonnes (mnt) in April-November 2025 (8MFY’26), as per provisional data maintained by BigMint. Pre-emptive restocking by EU-based buyers was the primary trigger, with cost concerns emerging ahead of the phase-in of Carbon Border Adjustment Mechanism (CBAM) from 1 January 2026.

Despite the strong export growth, India’s steel imports remained higher, totalling around 6.54 mnt in April-November. Imports fell 13% y-o-y under the influence of the 12% safeguard duty, which had been proposed in March this year and imposed provisionally for 200 days in April. However, it should be noted that the 200-day term expired in early November, as the Ministry of Commerce is yet to ratify the duty.

Commodity-wise export breakdown

India’s finished flat carbon steel exports totalled 4.14 mnt, up 31% y-o-y. Exports of hot-rolled coils (HRCs) surged by 77% y-o-y to 1.68 mnt, driving the strong growth in the finished flats category. Pipes and tubes shipments were up 26% at 1.32 mnt, while those of cold-rolled coils (CRCs) jumped by 37.1% to 0.42 mnt.

Semi-finished steel exports surged by 80% to 0.71 mnt. Long steel exports also increased by a strong 24% to 0.44 mnt.

Stainless steel exports dipped by 3% to 0.47 mnt in the wake of an 8% drop in flats exports.

Country-wise export scenario

Shipments to the EU surged by 45% y-o-y to 2.46 mnt, while those to the UAE climbed up by 18% to 0.42 mnt. Deliveries to Nepal slid by 15% to 0.39 mnt and to the UK by 12% to 0.38 mnt.

The strongest growth emerged in exports to Vietnam, which jumped manifold to 0.31 mnt compared to 21,000 t in the year-ago period. The US witnessed a 53% increase to 0.28 mnt, while shipments to Saudi Arabia dropped 74% to 45,000 t.

Factors influencing exports in Apr-Nov’25

CBAM concerns spur EU import rush: The imminent enforcement of CBAM from 2026 pushed EU-based importers to stock up on Indian goods, as there was uncertainty regarding the additional tax burden. Consequently, despite weak steel demand in the EU, India’s exports to the EU increased, especially from June.

Notably, India exhausted its HRC safeguard quota (227,782 t) for Q4CY’25 at the end of November, well ahead of its expiration on 31 December. In the CRC category, India exhausted around 47% of its 165,051 t quota by the same period, with approximately 88,268 t still remaining.

Indian HRC exports to Vietnam resume: Another supportive factor has been the resumption of HRC exports to Vietnam in September, which had been on pause for a prolonged period. The conclusion of some isolated deals seems to have pushed up export volumes, as demand remained subdued in October-November, particularly after a series of typhoons hit the country.

Billet exporters push more volumes on competitive pricing: India’s billet exports surged, with the UK, Nepal, and the US being primary destinations.

Supply shortfalls and elevated energy costs prompted UK-based re-rollers and sections mills to turn to imported billets from low‑cost origins (India, CIS, and MENA). Indian billets were competitively priced in 2025 because of a softer rupee and relatively low conversion costs, allowing FOB offers to undercut some European and CIS material after freight.

Additionally, in 2025, several regions in west and central India had surplus billets due to strong crude steel output but muted domestic longs demand, especially during the monsoon, so mills pushed more volumes to Nepal via short‑haul road/rail.

Freight and logistical advantages (low transport cost, short lead time, established credit relationships) meant incremental surplus was most easily absorbed by Nepal.

Commodity-wise import breakdown

India’s finished flat carbon steel imports stood at 4.31 mnt in April-November, down 28% y-o-y. Hot-rolled coil (HRC) arrivals declined by 38% to 1.89 mnt, while electrical steel fell by 15% to 1.21 mnt and galvanised steel by 26% to 0.61 mnt.

Semi-finished steel imports jumped by 437% to 0.91 mnt, while finished long arrivals decreased by 20% to 0.16 mnt. Stainless steel imports were marginally higher at 1.17 mnt compared to 1.16 mnt in the year-ago period.

Country-wise import break-up

Imports from South Korea remained stable y-o-y at 1.87 mnt. Chinese exports to India plunged by 51% y-o-y to 1.14 mnt, while shipments from Japan fell 22% to 1.01 mnt.

Factors influencing imports in Apr-Nov’25

Safeguard duty raises landed costs of imports: The implementation of the 12% safeguard duty raised landed costs of flat steel imports, making them higher than domestic prices.

For example, on 6 November, the landed costs of Chinese HRCs came to INR 55,786/t and Japanese HRCs to INR 53,128/t, while domestic HRCs were priced at INR 47,850/t ex-Mumbai, excluding GST.

Anti-dumping duties keep importers wary: Anti-dumping duties on Vietnamese flat steel and Chinese electrical steel also curbed India’s import demand. Additionally, the government has launched an anti-dumping investigation into cold-rolled stainless steel flat steel imports from China, Indonesia, and Vietnam.

Govt stresses on stricter quality control for imported steel: In June, the government mandated that raw materials used in the manufacturing of imported steel adhere to BIS quality norms. This was expected to curtail the arrival of low-priced, substandard imports, but implementation was deferred and certain exemptions granted. In November, a notification ordered a temporary suspension of 55 steel quality standards for products used by the engineering, auto, and specialty steel segments.

Outlook

Exports may moderate as CBAM kicks in

Going forward, the key theme seems to be CBAM and the associated cost pressures. Although there is just one week left before New Year’s Day, market participants continue to lack clarity on tax calculations, as the EU is yet to offer any definitive information. Moreover, the market has been inactive due to Christmas and the year-end, and Indian mills have also paused export offers, given the exhaustion of the safeguard quota.

Given such lack of clarity and the possibility of higher landed costs, India’s export momentum is likely to soften as January arrives. Indian exporters are holding out hope for an India-EU free trade agreement (FTA), as reports suggest that the pact may be in its final stages of negotiation.

Meanwhile, Indian exporters are looking to diversify their export basket. While the Middle East remains the leading alternative, Nepal has also emerged as an attractive market, with exporters concluding some deals in the first three weeks of December. Notably, the weakening rupee has made exporters very keen on boosting shipments.

Import outlook remains clouded

On the imports front, India seems to be witnessing contrarian trends. On the one hand, the recent spate of anti-dumping duties signal a firm hand, the quiet expiry of the safeguard duty and relaxation of steel quality norms have clouded the outlook. Additionally, despite the absence of the safeguard duty, importers have shied away from procuring significant volumes due to higher import costs, stemming from a weaker rupee. However, there is a risk of increased steel exports being diverted into India, with CBAM limiting imports into EU. This threat may end up pushing the government to formally ratify the safeguard duty.

Leave a Reply