- Steel export value declines 2% y-o-y even as volume rises 7%

- HRC exports decline by 19% y-o-y on trade remedial measures

- Govt brings back export licensing system after 16-year gap

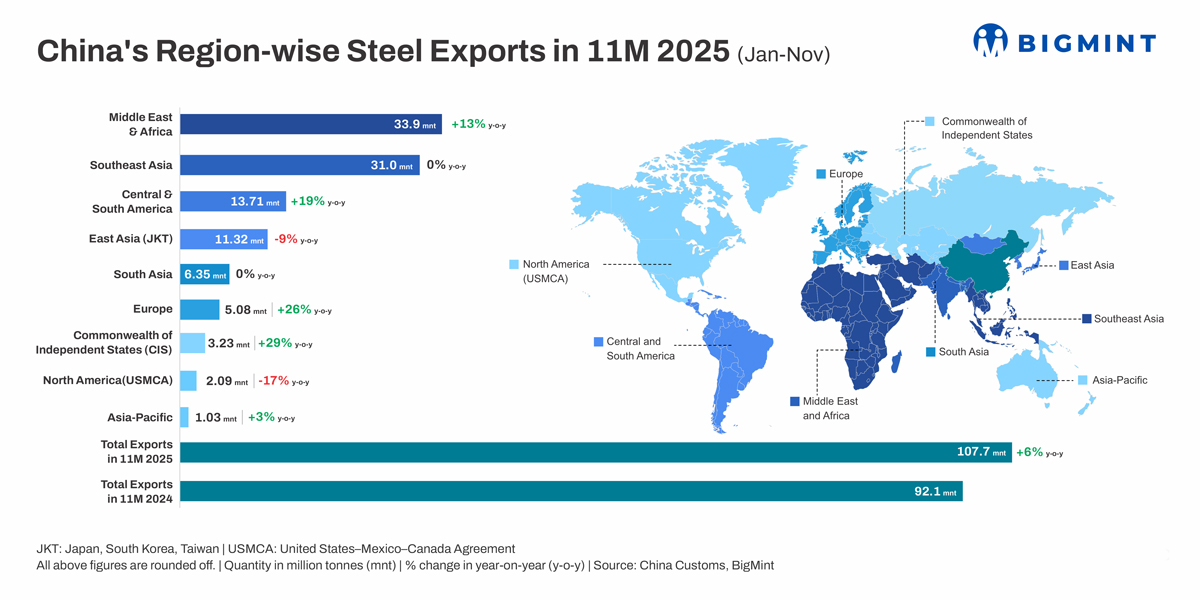

Morning Brief: China’s steel exports continued at a robust pace in January-November 2025 in sharp contrast to the steady downtrend in crude steel production. Exports increased by 6.7% y-o-y to 107.7 million tonnes (mnt) in January-November, easily surpassing the 100-mnt mark with November’s total of 9.98 mnt.

According to Mysteel’s projections, total exports in 2025 are sure to eclipse the previous record of 112.4 mnt, set in 2015, to reach an all-time peak. Additionally, various projections suggest a full-year total of around or at least 116-118 mnt, given that exports have consistently remained above the 9-mnt mark since March 2025.

Factors influencing China’s export growth in Jan-Nov’25

Supply glut continues, domestic demand remains inadequate: Chinese steelmakers continued to struggle with weak domestic demand throughout January-November, forcing them to redirect surplus supply to overseas markets. While the property sector grappled with falling prices and poor consumer demand, even manufacturing activity slowed, evidenced by the investment growth rate falling to a multi-year low of 1.9% in January-November 2025 against 9.2% in CY’24.

Interestingly, even a 4% contraction in crude steel output has failed to stabilise domestic supply-demand dynamics. China is on track to close the year with less than 1 billion tonne of crude steel production for the first time in five years.

Geopolitical tensions prompt frontloading: March 2025 onward, the US-China tariff war sparked an export rush from China. Unsure about the scope of the tariffs and fearing further escalations, Chinese exporters frontloaded shipments, while importers were eager to stock up on material, as downstream industries in their countries, too, accelerated deliveries to the US ahead of the reciprocal tariff deadline.

The robust export momentum, established early on in the year, continued through November, even though tensions between the two countries have eased relatively in the last few months.

Chinese exporters continue to offer competitive prices: Competitive prices have sustained overseas demand for Chinese steel. In fact, China’s export growth is rooted in volume rather than value, as according to Reuters’ analysis of Chinese customs data, the steel export value in dollars decreased by 2.1% y-o-y.

This is because Chinese steel exporters have continued to reduce prices to undercut offers from other origins. For example, prices of Chinese hot-rolled coils (HRCs) have averaged $466/tonne (t) this year, till 26 December, down 10% from 2024’s average of $518/t.

China’s 2025 HRC price average is lower than Japan’s $468/t, South Korea’s $493/t, and India’s $493/t for Middle East and Southeast Asian cargoes and $551/t for EU-bound shipments.

Export diversification enables circumvention of trade barriers: Chinese has diversified its export basket, both in terms of commodities and geographies, in the face of rising trade frictions and protectionism from some importing regions. For example, Chinese steel billet exports increased by 150% y-o-y to 11.93 mnt, with prices down 9.9%, as per a CISA release.

Meanwhile, HRC exports decreased by 19% to to 22.37 mnt during January-November, as per a Shanghai Metals Market report. HRC exports have been limited by trade barriers, while billet shipments have been boosted by comparatively restriction-free access.

Additionally, the share of steel sheets and plates in total exports fell by nine percentage points y-o-y to 51% during January to November this year.

Exports to the Middle East and Africa increased by 13% y-o-y in January-November, with the steepest growth in volumes to Saudi Arabia and Nigeria.

Southeast Asian volumes were stable y-o-y, with growth led by Thailand and the Philippines. A 22% decline in exports to Vietnam contributed to the stability.

Exports to Central and South America surged by 19% y-o-y. Only Brazil reduced exports by 8%; other regions witnessed a double-digit increase.

Shipments to East Asia fell 9% y-o-y on the back of a 12% decrease in intake by South Korea and 43% by Taiwan.

Exports to South Asia fell 5%, driven by a 34% drop in India. Those to Europe increased by 26%.

CIS countries witnessed an uptick of 29%, while North American volumes decreased by 17%. Exports to the Asia-Pacific increased by 3%.

Outlook

China has brought back a steel export licensing system after a 16-year gap, aimed at curbing tax evasion by exporters. Global steel market participants expect this measure to slow down China’s export momentum in the future, though it is unclear at the moment whether the impact will be significant.

Sluggish growth in China’s infrastructure, real estate, and manufacturing segments, which account for the bulk of the country’s steel consumption, may continue to exert pressure on demand. This will necessitate a turn to exports. The government’s property stimulus, so far, has been weaker than hoped for by steel market participants.

However, exports may remain higher y-o-y in December, as the export licensing system may prompt frontloading and exporters will also be keen on closing the financial year with robust revenues.

Leave a Reply