- Battery waste emerges as next structural challenge

- High metal value contrasts with low recovery efficiency

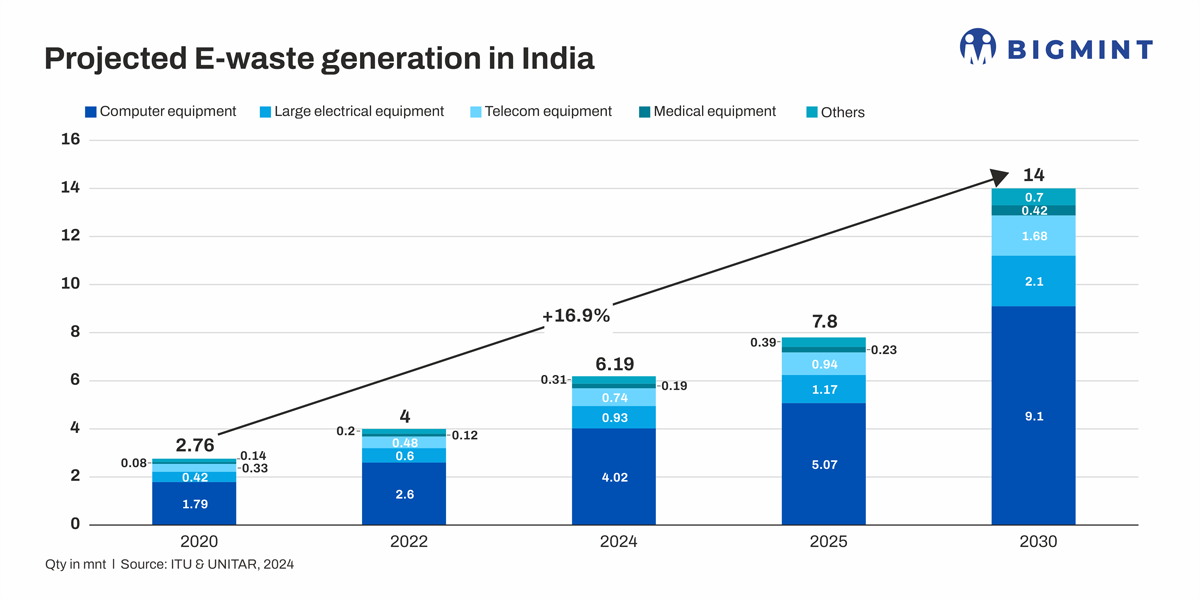

India’s e-waste generation is projected to increase from 6.19 million tonnes (mnt) in 2024 to nearly 14 mnt by 2030, growing at a compound annual rate of around 17%. Rapid digitisation, shorter product lifecycles, and rising consumption of electrical and electronic equipment are driving this expansion, placing mounting pressure on India’s recycling ecosystem.

India already ranks as the third-largest e-waste generator globally, accounting for nearly 7% of global volumes. However, the pace of waste generation continues to outstrip formal recycling capacity. India’s formal e-waste recycling rate remains close to 10%, well below the global average of around 22% and significantly lower than recovery rates in the EU and the US, which exceed 50%. As a result, a large share of e-waste continues to be processed through informal channels, leading to material losses and environmental risks.

Informal sector still dominates collection

Despite the introduction of Extended Producer Responsibility (EPR) under the E-waste Management Rules, 2022, the informal sector continues to handle an estimated 60-65% of e-waste flows. Informal collectors provide high collection efficiency and support more than 500,000 livelihoods, but rely on unsafe and low-recovery processing practices.

Formal infrastructure has expanded to over 400 authorised e-waste recyclers and dismantlers across India. However, capacity utilisation remains uneven. Nearly 60% of formal processing capacity is concentrated among just 6% of recyclers, while limited collection infrastructure–approximately 2,800 formal collection centres nationwide—continues to divert waste toward informal supply chains.

High metal value, low recovery

e-waste is a metal-rich waste stream. A tonne of mobile phone scrap can yield 300-400 grams of gold and up to 4 kg of silver, while printed circuit boards contain high concentrations of copper, palladium, and other critical materials. Despite this, India’s current EPR framework mandates recovery of only four metals–iron, aluminium, copper, and gold.

As a result, recovery rates for critical raw materials remain limited to around 17%, leading to an estimated INR 42,500 crore in cumulative economic losses from unrecovered metals. Expanding EPR coverage to include additional critical and precious metals could materially improve recycling economics and attract greater investment into the formal sector.

Lithium-ion batteries add to the challenge

The e-waste challenge is now converging with rising lithium-ion battery waste. India’s lithium-ion battery demand is projected to grow from 16 GWh in 2023 to nearly 250 GWh by 2035, driven largely by electric vehicles and energy storage systems. End-of-life battery volumes are expected to rise sharply over the next decade.

Against over 80,000 t of announced lithium-ion battery recycling capacity, end-of-life battery availability in 2025 is estimated at only around 15,000 t, creating underutilisation risks. Recycling economics vary by chemistry. While NMC and LCO batteries remain viable to recycle, LFP batteries–expected to account for nearly 60% of EV battery demand by 2030–remain commercially unviable under current EPR pricing.

Outlook

With e-waste generation set to more than double by 2030, India is approaching a critical inflection point. The country imports 100% of its lithium and cobalt, and 75-80% of its nickel and rare earth requirements, making material recovery a strategic priority.

Strengthening enforcement, expanding EPR metal coverage, introducing chemistry-linked EPR pricing, and integrating informal collectors into formal supply chains will be key to unlocking value at scale. The next phase of India’s resource strategy will depend not on how much waste it generates–but on how efficiently it recovers materials from it

Leave a Reply