- Mine output to recover quickly post-holiday, raising surplus risks

- Prices may weaken further amid supply-demand imbalance

Mysteel Global: The Chinese metallurgical coal market is anticipated to face mounting downside pressures after the Chinese New Year (CNY) holiday that officially spans February 15-23, as a fundamental imbalance may aggravate with the majority of miners planning to resume production within February, Mysteel’s latest survey results find.

The survey covers 395 operating coking coal mines across China, with a total capacity of 757 million tonnes/year. Of these, 388 mines, with a combined capacity of 744 million t/y, have scheduled holiday shutdowns for varying durations, estimated to reduce raw coal production by 18.68 million tonnes, according to the survey.

The average holiday leave for the surveyed mines is 10.1 days, slightly shorter than the 10.6 days observed for the corresponding period of last year. Privately-owned mines are expected to take nearly 14 days off on average, much longer than the 6.2 days for state-owned mines, the survey indicates.

Notably, around 69% of the mines surveyed plan holidays of less than seven days, a higher rate than the previous year’s 62%. In North China’s Shanxi province, the country’s largest producing hub for the steelmaking feed coal, 104 mines plan to halt operations for less than seven days for the festival.

The survey shows that the resumption rate among these coking coal mines after the CNY holiday will climb to around 84% before the end of February, and national mine production may notch an intra-year high in March, indicating a relatively fast supply recovery after the holiday. This will likely exacerbate the imbalance of coking coal fundaments amid expectations for a slow return of buying demand, Mysteel’s analyst predicts.

As major coking coal buyer, independent coke firms will typically maintain their destocking process of the feed coal in one month after the CNY holiday, meaning that they mainly consume their existing stockpiles and barely make new purchases, according to survey respondents. Therefore, coking coal trading is unlikely to see synchronous recoveries with supply, elevating surplus risks as well as downside pressures for coal prices.

Meanwhile, demand for the feed coal will likely see continued constraints if downstream steel mills are not motivated enough to lift their hot metal production or there are no favorable macroeconomic policies to support the sentiment, the analyst warns.

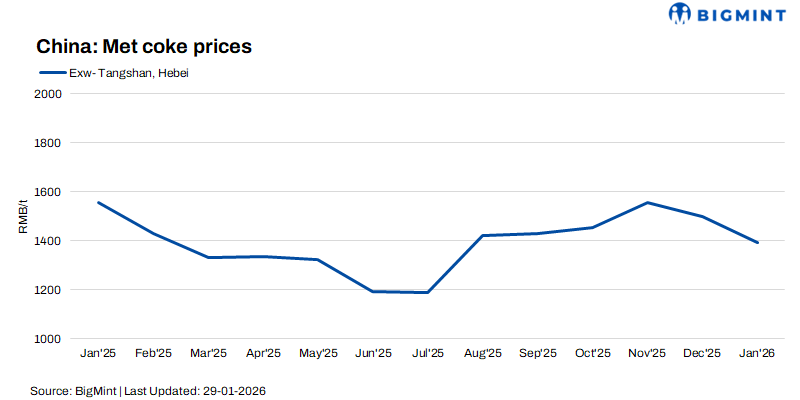

Like in the previous two years, the post-holiday market could remain weak for up to two months. For example, Mysteel’s assessment of the national composite coking coal price hit a low of Yuan 1,065.4/tonne ($153.4/t) by March 21 2025, lower by 12% from the pre-holiday level.

The weak market conditions leading up to the CNY holiday will likely put additional pressure on coal prices post-holiday. The recent restocking activities among coke and steel producers have cooled earlier than usual this winter, mainly due to domestic miners’ active production this month as well as steady inflows of imported coal cargoes. The slow liquidity will keep the coking coal market in a surplus state, adding pressures to stock selling after the holiday.

Mysteel’s survey on the 523 Chinese coking coal mines shows that their washed coal inventories reached 3.9 million tonnes in the first week post the holiday last year, up by 2.1% from a week earlier. For 2023 and 2024, stock levels even started rising quickly in the second week after the holiday.

Note: This article has been written in accordance with a content exchange agreement between Mysteel Global and BigMint.

Leave a Reply