- Dispatches to sponge iron sector surge as producers turn away from imports

- Captive, commercial miners lift production as CIL, SCCL record declines

India’s June 2026 coal data signals an important shift in the domestic supply chain. The focus has moved from expanding mine output to accelerating coal evacuation. National production increased just 1.4% y-o-y to 80.09 million tonnes (mnt), while dispatches rose a much stronger 7% to 90.01 mnt.

The nearly 10 mnt gap between production and dispatch indicates that producers continued drawing down the substantial pithead inventories accumulated at the end of FY’26. The trend was even clearer during April-June: production declined 5.9% y-o-y to 232.49 mnt, while dispatches increased 2.8% to 268.04 mnt, implying that 35.55 mnt more coal was dispatched than produced during the quarter.

The data also points to a changing demand mix. While power remained the largest consumer, much of the incremental coal was absorbed by sponge iron and the broad “others” category rather than steel or cement. At the same time, stronger rail evacuation enabled higher dispatches despite largely flat mine output.

Captive, commercial producers drive production growth

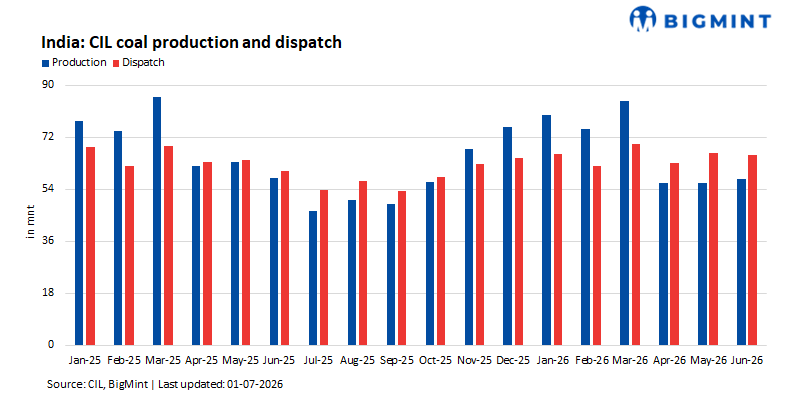

Headline production growth concealed significant divergence among producers. CIL’s June output declined 0.6% y-o-y to 57.43 mnt, while April-June production fell 7.5%. SCCL’s production declined even more sharply, falling 17% in June and 20.4% during the quarter.

The entire increase in national production came from captive and other producers, whose June output rose 14.4% to 18.37 mnt and increased 5.1% during April-June. The data reinforces a structural trend already underway: incremental domestic coal production is increasingly being delivered by captive, commercial, and other producers rather than the traditional public-sector miners.

CIL nevertheless increased June dispatches by 7.8% to 65.95 mnt despite lower production. During April-June, it dispatched 28.24 mnt more coal than it produced, making it the principal contributor to the national drawdown in pithead inventories. Operationally, the company prioritised clearing accumulated stocks rather than maximising mine output.

Among CIL subsidiaries, three developments stood out. Central Coalfields Ltd (CCL) was the strongest performer, with June production rising 35.4% and dispatches 52.7%, supported by a sharp improvement in rail evacuation. Mahanadi Coalfields Ltd (MCL) continued to dispatch substantially more coal than it produced, making it another major contributor to inventory reduction despite lower output. Bharat Coking Coal Ltd (BCCL) remained the weakest performer, with cumulative production falling 27.5%, highlighting the continuing challenge of increasing domestic coking coal availability.

Dispatch growth reflects changing consumption patterns

Production remained subdued, but dispatches increased across all supplier categories as producers accelerated evacuation from existing inventories rather than relying on fresh mine output.

Power remained the dominant consumer, accounting for nearly 79% of June dispatches, but its contribution to quarterly growth was modest. Power-sector dispatches increased just 1.09 mnt during April-June, compared with an overall national increase of 7.25 mnt, indicating that most additional coal was directed to non-regulated consumers.

The strongest growth came from sponge iron, where dispatches jumped 90.6% in June and 56% during the quarter. The increase supports broader market evidence that domestic coal has become more competitive relative to imported thermal coal, encouraging sponge iron producers to substitute domestic supplies for imports.

By contrast, steel sector dispatches declined 14.9% in June and 31.6% during April-June, while June deliveries to cement also weakened. Although cement dispatches remained marginally higher for the quarter, the June slowdown is consistent with seasonal construction weakness and the sector’s ability to switch between domestic coal, imported coal, and petcoke depending on delivered fuel economics.

Another noteworthy development was the 35.1% increase in dispatches to the broad “others” category. During April-June, this segment accounted for almost the entire increase in national dispatches, suggesting that much of the additional coal was absorbed outside the traditional power, steel, and cement sectors.

Improved rail movement enables higher dispatches

Higher dispatches would not have been possible without stronger rail evacuation.

Average daily rake loading increased 6.1% y-o-y across all sectors and 9.7% for power, enabling producers to move accumulated inventories to consumers. However, actual loading still fell short of Ministry targets, achieving only 81% of planned all-sector loading and 85.4% of planned power-sector movement.

The data therefore highlights both progress and remaining constraints. Rail logistics improved sufficiently to support stronger dispatches, but the system continues to operate below planned capacity.

Outlook

June’s data marks a transition in India’s coal market from production-led growth to inventory-led supply. Production remained subdued and was driven almost entirely by captive and other producers, while CIL and SCCL relied on accumulated pithead stocks to maintain dispatches.

Demand also became more uneven. Power remained well supplied but contributed relatively little to incremental growth, while sponge iron and the broad “others” category absorbed much of the additional coal. Steel and cement procurement, by contrast, remained restrained.

In the near term, this strategy is sustainable because pithead inventories remain comfortable despite the first-quarter drawdown. Over time, however, dispatch growth cannot continue to outpace production indefinitely. As inventories normalise, sustaining coal availability will increasingly depend on restoring production momentum at CIL and SCCL while further improving rail evacuation to narrow the persistent gap between planned and actual rake loading.

Leave a Reply