- Demand from Asia remains largely weak

- Cautious Turkish mill procurement limits overall trading activity

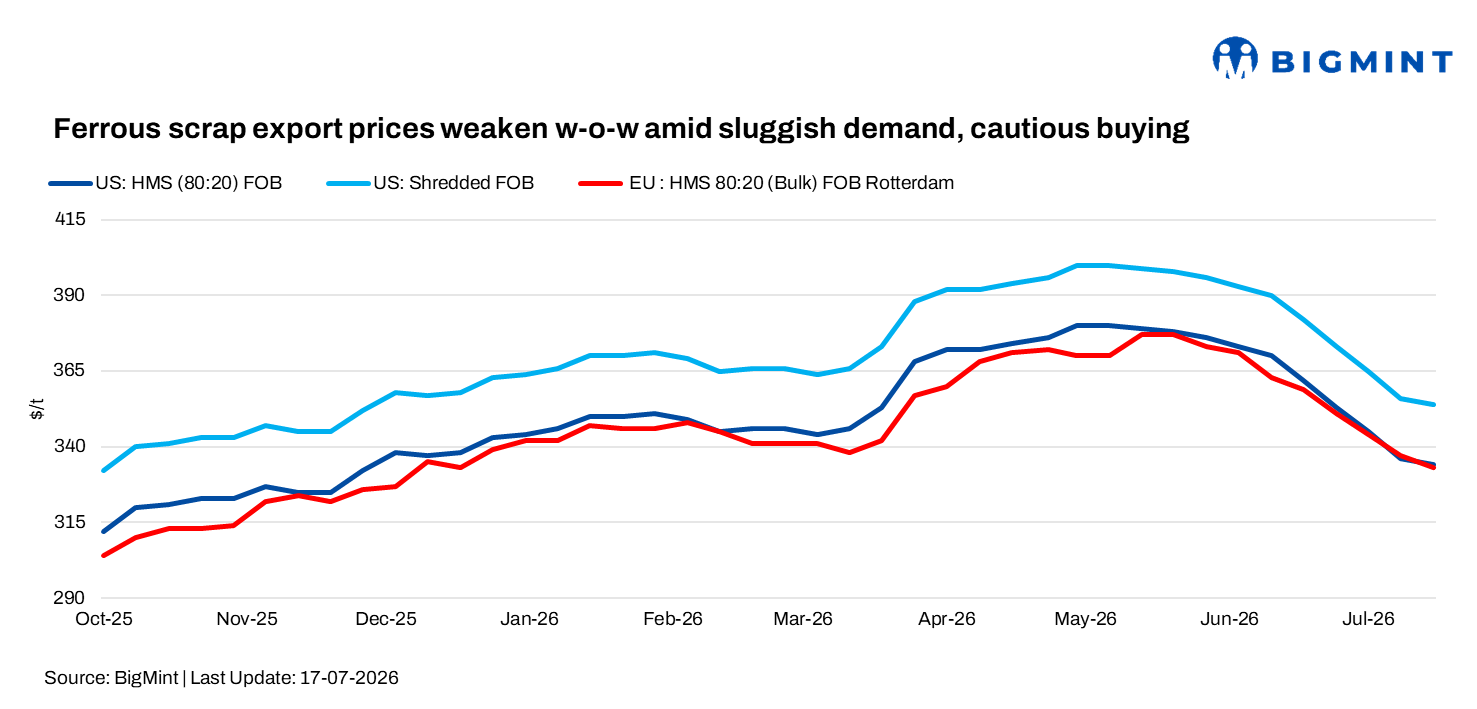

Ferrous scrap export markets remained under pressure during the week ended 17 July, with the US market recording lower prices amid weak export demand and improved domestic scrap availability. Meanwhile, European and Brazilian exporters also faced subdued buying interest from Turkiye and Asia, while cautious mill procurement and sluggish steel demand continued to weigh on overall market sentiment.

US

The US ferrous scrap market softened during the week ended 17 July as weaker export demand and improved domestic scrap availability pressured obsolete grades. Shredded scrap declined to $420-425/t DAP Midwest and $415-418/t DAP Southeast, while HMS eased to $365-370/t DAP Midwest but remained stable at $372-375/t DAP Southeast. In contrast, busheling held firm at $460-462/t DAP, supported by steady sheet steel production.

Export sentiment remained subdued, with HMS 80:20 assessed at $334/t FOB US East Coast and shredded scrap at $354/t FOB, as limited buying interest from Türkiye continued to weigh on overseas demand. However, the weaker export market had only a muted impact on domestic pricing. Supported by steelmakers operating at around 80% capacity utilisation, the US scrap market remained broadly balanced, although July settlements exposed growing regional disparities.

Rather than following a uniform national trend, domestic scrap prices were shaped by local supply-demand conditions and the negotiating leverage of individual mills. Regions with ample scrap availability saw deeper price concessions, while tighter supply and stronger dealer positions helped limit declines elsewhere. The uneven settlements underscored the fragmented nature of the domestic market, suggesting regional procurement dynamics are likely to remain the primary driver of pricing through August.

Europe

European export ferrous scrap markets remained under pressure during the week as weak buying interest from Turkiye and South Asia continued to weigh on prices. Turkish mills maintained cautious procurement due to poor long steel demand and squeezed margins, with only one Baltic-origin HMS 80:20 cargo reported at $363/t CFR.

Benelux dockside HMS 80:20 prices eased to around Euro 270/t ($209/t) DAP, while FOB Rotterdam HMS 80:20 declined to $333/t FOB. In Italy, export scrap prices were assessed at Euro 340-350/t ($389-400/t) FOB for shredded scrap (E8), Euro 305-325/t ($349-372/t) FOB for HMS 80:20 (E3), and around Euro 335/t ($383/t) FOB for HMS 90:10 (E2), reflecting continued pressure from subdued export demand and cautious buying sentiment.a

Brazil

Brazil’s ferrous scrap market remained under pressure during the week as several steelmakers announced a second round of domestic scrap price cuts amid weak finished steel demand and sluggish mill sales. Market participants reported further purchase price reductions of BRL 50-80/t ($10-16/t), particularly in Sao Paulo, while some foundries kept prices unchanged but are expected to renegotiate procurement in the coming days.

Export sentiment also weakened, with HMS 80:20 FOB easing to around $275-285/t and shredded scrap FOB to $305-310/t, reflecting softer demand from key overseas markets. Limited buying interest from India and Bangladesh, coupled with uncertainty over potential US tariffs on Brazilian pig iron, continued to weigh on export prices and overall market sentiment.

Leave a Reply