- Higher import offers failed to revive buying

- Domestic fuels continued replacing imported petcoke

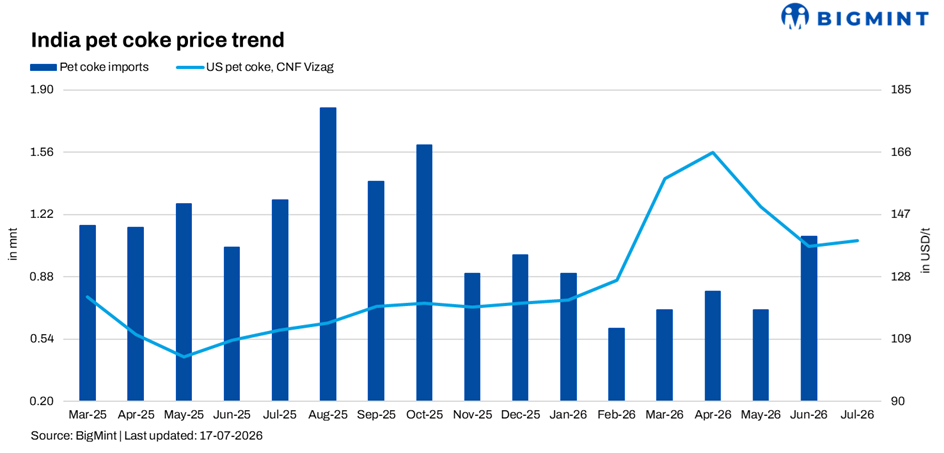

Imported petcoke offers have moved back towards US$140-145/t CFR India, but cement producers remain reluctant to buy, relying on domestic coal, existing inventories and selective use of US high-CV coal. Domestic refinery price cuts have further weakened immediate import demand.

India’s petcoke market is showing a widening disconnect between international replacement values and domestic buying appetite. High-sulphur imported petcoke offers have firmed after correcting sharply from April-May highs, but cement producers remain largely on the sidelines.

The weakness is not due to a collapse in cement output. Industry volumes are estimated to have grown around 8% year on year in Q1FY27. Instead, procurement is being restrained by the monsoon slowdown, comfortable inventories, cheaper domestic alternatives and expectations that imported prices could soften again.

Key market indicators

Imported offers rise, but buyers stay away

Imported petcoke indications were around US$132-135/t CFR India in late June, while cement buyers were bidding closer to US$120/t and waiting for a deeper correction following weaker crude oil prices.

By early July, offers had increased to US$134-139/t, with some US high-sulphur and Saudi-origin cargoes indicated near US$142/t CFR west coast India. By 17 July, immediately available offers were heard at US$140-145/t, although assessed values remained lower.

This gap between published assessments and executable offers is important. Replacement cargoes available to Indian buyers appear tighter and more expensive than the headline index suggests.

Buying, however, remains weak. Several cement producers reported that they were not purchasing at current levels, while others had sufficient fuel stocks for another six to eight weeks. The market is therefore not experiencing a demand-led rally. Sellers are attempting to recover higher FOB and freight costs in a market where buyers see little urgency to replenish.

Freight supports delivered prices

US Gulf Coast 6.5% sulphur petcoke was assessed at US$78/st, up US$3/st week on week, while CFR India material stood at US$136.50/t, up US$1.50/t.

Freight remains the main support for delivered values. Indicative US Gulf Coast-east coast India freight for a 50,000-t cargo was US$62.85/t, materially above freight into Europe or Turkey. Marine insurance premiums and intermittent geopolitical risks have also prevented logistics costs from returning fully to pre-conflict levels.

As a result, petcoke has corrected substantially from its April-May peak, but Indian buyers are still not seeing consistently cheap replacement cargoes.

Domestic price cuts weaken the import case

India’s domestic refiners reduced petcoke prices again in July as global supply concerns eased.

IOCL cut road prices by INR 800-880/t:

· Koyali: INR 15,420/t

· Panipat: INR 16,680/t

· Paradip: INR 14,430/t

· Haldia: INR 14,550/t

Nayara Energy lowered its price by INR 1,680/t to INR 17,650/t, while CPCL reduced prices by INR 1,540/t to INR 17,760/t. BPCL made the sharpest cuts, with Bina prices falling by INR 2,500-3,000/t and Kochi rail prices declining to INR 17,000/t.

These reductions matter because cement producers compare imported petcoke not only with other imported fuels but also with domestic petcoke and coal. Although refinery prices remain elevated at some locations, the downward trend has encouraged buyers to defer imported purchases.

Cement producers are switching fuels, not reducing energy use

Weak imported petcoke buying does not mean cement plants have stopped consuming fuel. It reflects greater flexibility in procurement.

Cement volumes are estimated to have grown around 8% year on year in Q1FY27, while pan-India cement prices rose approximately 3% quarter on quarter. However, operating costs remained elevated and the monsoon quarter is expected to bring weaker demand and margin pressure.

Plants are responding by adjusting their fuel mix:

· Some are relying mainly on domestic coal from CIL and SCCL.

· Others are blending domestic coal with US high-CV NAPP coal.

· Several have reduced petcoke use because current replacement offers are uneconomical.

· Buyers with adequate inventories have postponed fresh purchases.

This suggests that cement producers are not abandoning petcoke structurally. They are treating it as one component of a wider fuel basket and adjusting consumption according to delivered cost, sulphur limits, kiln chemistry and inventory position.

Petcoke retains a heat-value advantage over NAPP

Recent industrial US NAPP coal business has been reported at around US$134/t CFR west coast India and US$136/t CFR east coast India. At current levels, high-sulphur petcoke is being offered at US$136.5-145/t CFR India with an assumed calorific value of 7,500 kcal/kg NAR, translating to a delivered energy cost of around US$18.2-19.3/GCal. In comparison, US NAPP coal, priced at US$134-136/t CFR India with an assumed 6,900 kcal/kg NAR, works out to a delivered energy cost of approximately US$19.4-19.7/GCal. At the lower end of the petcoke price range, its energy-cost advantage is clear. At executable offers of US$141-145/t, however, the difference narrows and may disappear after accounting for grinding costs, sulphur restrictions and plant-specific operating requirements. This explains why some cement plants are using NAPP coal despite petcoke’s higher calorific value. NAPP offers lower sulphur, easier blending with domestic coal and, at current prices, comparable delivered economics.

Outlook

India’s imported petcoke market is likely to remain subdued during the monsoon quarter despite firmer international offers.

Cement producers have limited urgency to purchase because many hold comfortable stocks and can switch towards domestic coal or NAPP coal. Domestic refinery price cuts have further weakened the case for imports, while buyers continue to expect a deeper international correction.

At the same time, downside may be limited by firmer US Gulf Coast prices, expensive freight and elevated marine insurance costs. Sellers are therefore unlikely to accept the US$120/t buying ideas seen in late June unless FOB or freight markets weaken sharply.

The near-term market is likely to remain divided between assessed values in the mid-US$130s/t and executable offers around US$140-145/t. Meaningful Indian buying is more likely to return when delivered offers move closer to the mid-US$130s/t, plant inventories decline enough to force replenishment, or NAPP coal becomes materially more expensive.

Until then, Indian cement-sector petcoke demand will remain selective rather than absent, with procurement determined by the economics of the entire fuel basket rather than headline calorific value alone.

Leave a Reply