- Supply constraints and raw material shortages support prices

- Global markets supportive despite weak end-user demand

Stainless steel prices remained firm in the week ended 1 April, supported by improving demand conditions and tightening material availability. Market participants expect further upside amid persistent supply disruptions, elevated freight costs, and ongoing geopolitical tensions impacting energy supply chains.

Meanwhile, India has granted a temporary exemption from mandatory input standards for select stainless steel flat product imports, easing procurement challenges. The exemption applies to shipments with bill of lading dated on or before 30 September 2026.

The move reflects a continued gap between domestic supply and demand, particularly in 200 and 300 series flat products. Limited raw material availability, coupled with energy-related disruptions, has restricted capacity utilisation across mills. Industry participants highlighted that the exemption will support supply continuity, stabilise prices, and prevent downstream shortages in the near term.

Earlier, the Ministry of Steel had extended the BIS exemption till 31 March 2026 under specific Indian standards, and the latest notification further prolongs this relaxation. As a result, stainless steel flat products can continue to be imported without BIS certification, ensuring smoother inflows. Market participants noted that the extension signals persistent structural supply tightness, with domestic production still unable to fully match rising demand, thereby necessitating continued import support in the near term.

Finished flats

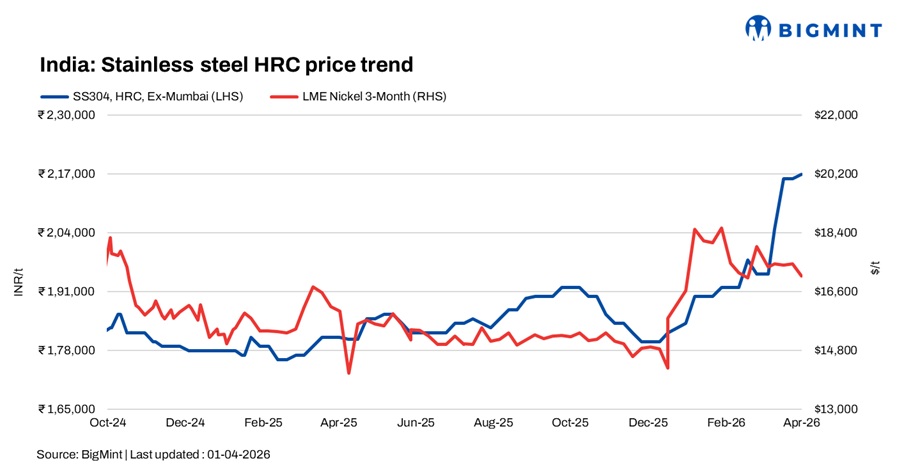

BigMint’s benchmark 304 HRC was assessed at INR 217,000/t ex-Mumbai, up INR 1,000/t w-o-w, while 316 HRC stood at INR 375,000/t, stable w-o-w.

Market participants indicated that supply tightness persisted, while demand showed gradual improvement, supported by restocking and need based consumption. Rising input costs and limited inventory availability continued to underpin price levels.

A leading stainless steel producer in India has also increased prices for HR and CR coils, effective 1 April, marking the first hike of the month. The revision is driven by rising logistics costs, a stronger US dollar, and ongoing geopolitical tensions impacting energy and gas supply. Revised prices:

304/304L: +INR 2,500/t

316/316L: +INR 7,500/t

400 series: +INR 2,000/t

200 series: +INR 2,000/t

JSL AUS: +INR 3,000/t

The company has increased its coil prices by up to INR 28,500/t in 304-grade and INR 45,000/t for 316 grade products in Q1 CY’26, citing higher alloy costs, global pressures and strong dollar.

Globally, stainless steel prices in Taiwan continued to rise despite subdued demand, reflecting cost-push pressures. In Europe, major producers increased alloy surcharges for April, further reinforcing the global uptrend.

Finished longs

The finished longs market also strengthened, supported by supply constraints and moderate domestic demand. However, export activity remained subdued due to ongoing Middle East tensions.

304L (25-100 mm) black round bars were assessed at INR 183,000/t ex-Mumbai, up INR 7,000/t w-o-w. Meanwhile, 316L black round bars stood at INR 310,000/.

Raw material scenario

Outlook

India’s stainless steel market is expected to remain firm in the near term, supported by supply-side constraints and gradually improving demand. However, geopolitical risks, energy cost volatility, and raw material availability will continue to influence market direction.

Leave a Reply