- Selective buying continues amid weak end-user demand

- Ship-recycling sentiment improves but LC issues curb trade

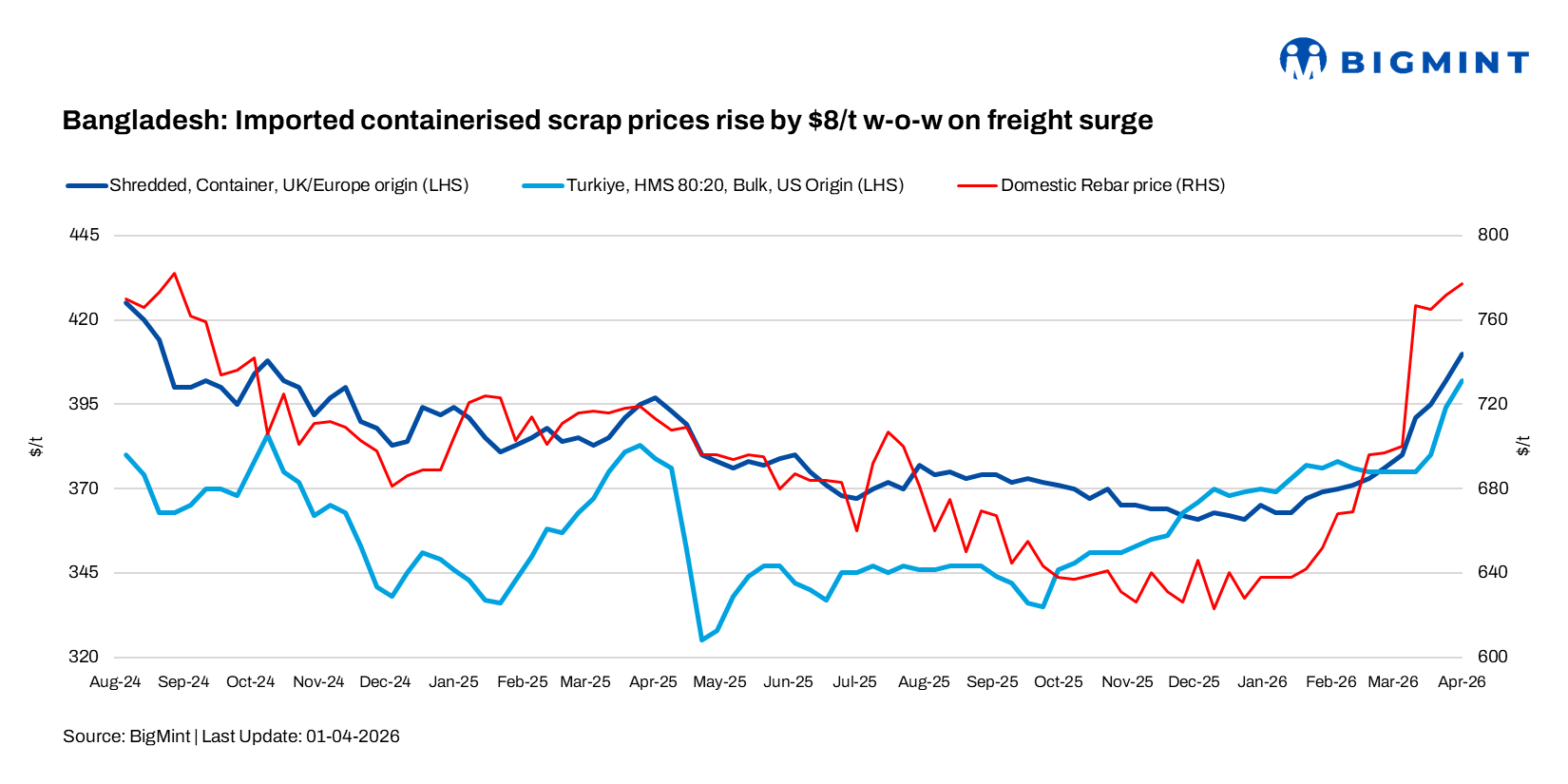

Bangladesh’s imported ferrous scrap market remained firm in the last week of March, with prices rising by up to $8/t w-o-w on 1 April 2026, driven by higher Japanese offers and rising freight costs linked to ongoing Middle East tensions. However, demand fundamentals remained fragile, limiting aggressive procurement despite improved trading activity.

BigMint’s weekly assessments

- European-origin containerised HMS (80:20): $385/t, up $8/t w-o-w

- European-origin containerised shredded: $410/t, up $8/t w-o-w

- Japanese-origin bulk H2: $390/t, up $1/t w-o-w

- US-origin bulk HMS (80:20): $398/t, up by $3/t w-o-w

Price scenario

Offers from alternative origins also remained elevated. Australia/New Zealand and Singapore-origin cargoes were heard at $420/t CFR for PNS and around $410/t for shredded, while imported shredded scrap was assessed at approximately $408/t CFR.

A Chattogram-based trader informed BigMint that Bangladesh continued to trade at a premium to India ($395/t CFR), though still below Pakistan ($415-420/t CFR).

As per a Japanese trader source, Japanese scrap offers continued to set a firm tone for the market. H2 offers were heard at JPY 50,000-52,000/t FOB ($315-328/t), translating to $390-395/t CFR Bangladesh, while H1/H2 (50:50) stood at JPY 51,000-53,000/t ($322-334/t) FOB or $400-405/t CFR.

Higher-grade Shindachi and HS scrap were offered at JPY 55,500-56,500/t ($350-357/t) and JPY 55,000-56,000/t ($347-353/t) FOB, translating to $425-430/t and $420-425/t CFR, respectively, indicating firm sentiment across premium grades.

Freights from Japan were reported at $65-70/t, while broader logistics costs remained elevated due to disruptions in the Middle East. Market participants highlighted additional war-related surcharges of nearly $100/t on certain Gulf routes, rendering shipments from the UAE, Kuwait, and Bahrain largely unviable.

Disruptions in oil supply, particularly from Qatar, have further increased cost pressures across the value chain in Bangladeshi mills’ operations.

Rebar prices were reported at BDT 91,000-96,000/t ($740-781/t), while billet prices stood at BDT 76,000-77,000/t ($618-626/t). Local scrap was heard at BDT 61,000-63,000/t ($496-512/t). Buying activity was largely driven by stockists — inventory accumulation rather than real end-user demand — and market participants noted that retail (individual) demand remains limited.

Chattogram’s ship recycling market experienced a pickup in sentiment post-Eid, with recyclers returning after clearing inventories and securing financing. Buyer interest improved, with participants re-entering the market for fresh tonnage. However, momentum was constrained. Low flat steel prices in Bangladesh and China continued to cap bid levels, while lingering LC-related issues and stricter due diligence on sanctioned vessels slowed transaction closures.

While demand improved, market participants remained cautious, with activity in the near term likely to depend on vessel availability and smoother financial flows.

A major recycler noted that global regulatory pressure continues to underestimate the progress made by South Asian yards in compliance and operational standards, even as the region strengthens its position in the global recycling market.

Outlook

Bangladesh’s scrap market is expected to remain firm, with imported shredded holding at $408-410/t CFR and Japanese-origin H2 bulk offers expected to stay at $390-395/t CFR, supported by elevated freight amid the ongoing Middle East war situation. However, end-user demand remains weak, with buying largely driven by stockists rather than end-use consumption. While import activity may gradually improve, the pace of recovery will depend on a pickup in real steel demand. Overall, the market is likely to stay stable with a slight upward bias in the coming days.

Leave a Reply