- Bid-offers disparities limit deal closures

- Domestic realisations remain more attractive

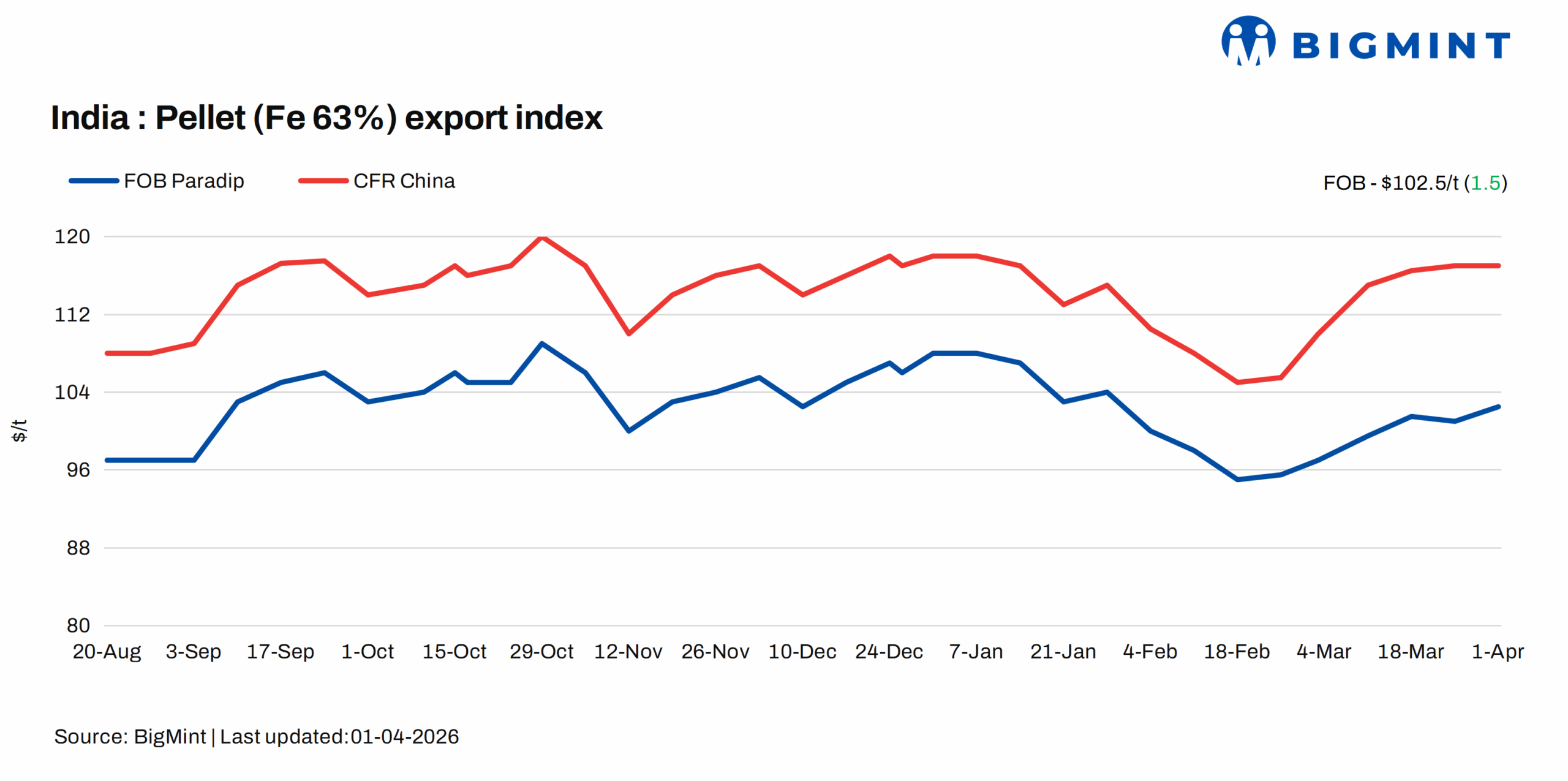

India’s pellet export prices inched up w-o-w on 1 April 2026, supported by the global iron ore fines benchmark remaining largely stable. At the same time, freight rates showed some temporary easing, and vessel availability improved, reviving buyer interest and lifting CFR levels. However, overall sentiment remained cautious, as no confirmed export deals have been heard over the past couple of weeks.

Price and trades update

BigMint’s India pellet (Fe 63%, 3-3.5% Al) export index edged up by around $1.5/t w-o-w to $102.5/t FOB east coast on 1 April against 25 March. No export deals were concluded from the east coast in this publishing window, with most buyers staying away from bidding.

Market updates

Pellet export prices remained largely stable in the past few days, with market activity largely quiet and only a few offers circulating. While freight rates, which were previously at around $16-18/dmt, eased in recent days, CFR levels remained largely unchanged. This indicates that FOB prices moved higher.

Notably, although Chinese portside inventories are still high, participants believe there is enough room to absorb additional volumes. This has prevented any sharp downside for now.

Buyers, however, remained cautious and unwilling to match current offers. Bids were heard around $114-115/t CFR China, well below sellers’ expectations of $134-135/t CFR China. This wide pricing gap kept most deals on hold.

An international trader stated, “There are very few offers in the market, and even those are not workable for buyers. The gap between bids and offers is just too wide right now.”

On the demand side, Chinese raw material demand was supported by steady pig iron production, but mills leaned towards cost-effective options such as domestic concentrates instead of imported pellets.

Another participant noted, “Demand is there to some extent, but buyers are being very selective and only looking at options that make sense cost-wise. The Chinese mills are using cost-effective material to safeguard margins.”

Meanwhile, Indian sellers focused on the domestic market, where trades were still taking place, though at a slower pace, offering relatively better realisations than exports.

A pellet producer stated, “Current export prices are not viable for us due to higher transportation costs and competitive offers from international buyers. Prices of around $112-115/t FOB on the east coast are more feasible for us, as domestic prices and demand are relatively better.”

Overall, the pellet export market was slow and cautious, with most players waiting for prices to align before any meaningful trade activity picks up.

Domestic vs export market

Domestic pellet prices remained steady over the week, while export realisations moved higher, leading to a narrowing of the domestic-export spread. Export realizations (Fe 63%) increased to INR 7,400/t on 1 April, reflecting a w-o-w rise of INR 150/t. In contrast, domestic realisations (Fe 62.5%) held firm at INR 8,850/t exw, stable w-o-w. As a result, the spread between domestic and export prices narrowed to INR 1,450/t remaining largely stable.

Rationale

- No confirmed deal from India’s east coast was recorded in this publishing window for T1 trade and was allotted 0% weightage for today’s price calculations. Click here for the detailed methodology.

- Eight (8) indicative prices were received, and six (6) were considered for the calculation of the index and given a balance 100% weightage.

Factors impacting pellet exports

Chinese iron ore fines prices dip w-o-w: The benchmark iron ore fines Fe 61% index decreased by $1/t w-o-w to $108/dmt CFR China on 31 March. Trading activity picked up despite stalled negotiations, with prices supported by higher hot metal output, supply concerns, and improved portside trades.

DCE iron ore futures prices remain stable: Iron ore futures on the Dalian Commodity Exchange (DCE) for the May 2026 contract closed at RMB 815.5/t ($119/t) on 1 April, largely steady w-o-w.

Vessel freights drop w-o-w: Iron ore freights declined by 0.9/dmt w-o-w to 14.8/dmt on 31 March 2026 on heightened market volatility. Sentiment remained subdued with limited fixture activity, thin tonnage availability, and higher bunker prices, as participants largely adopted a wait-and-watch approach. With, CFR offering levels largely being the same; on reduction of freight, the export level prices received an uptick. Most fixtures were concluded at lower levels, reflecting a soft and uncertain market tone.

Outlook

The pellet export market is expected to remain subdued, as sellers are not floating offers currently. The market may resume in the second half of April, with some export tenders expected during that period.

Leave a Reply