- Portside prices rise on tight supply, higher global indices

- Export cargo diversion limits availability, lifts offers

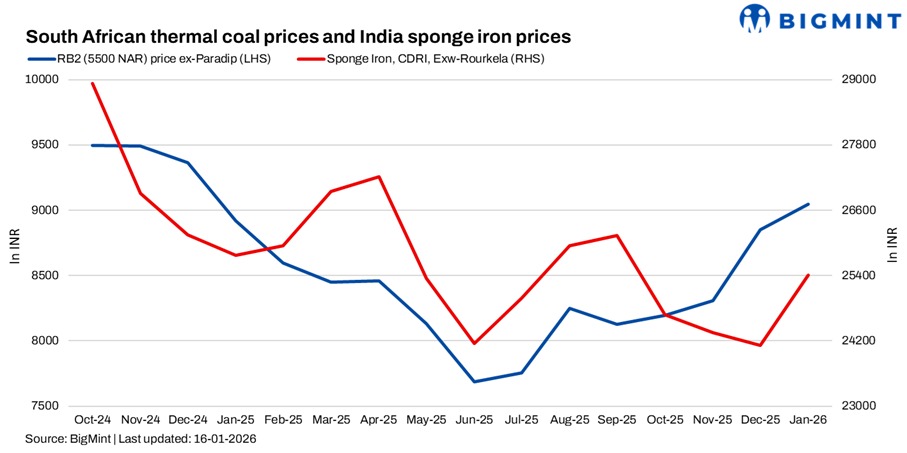

South African thermal coal prices at Indian ports moved higher w-o-w, supported by seasonal supply tightness, rising global indices, and selective improvement in sponge iron prices. However, trade activity stayed muted during the week as Sankranti holidays in South India, cautious buying behaviour, and ample domestic coal availability limited deal closures.

Portside price movements strengthen, trades remain thin

Exw Paradip 5,500 NAR rose by INR 100/t w-o-w to INR 9,150/t, while at Vizag prices increased by INR 50/t to INR 9,000/t. 4,800 NAR recorded sharper gains at Paradip, rising by INR 200/t to INR 7,800/t, while Vizag prices edged up by INR 50/t to INR 7,600/t. Prices in Paradip have risen to one year high as per data maintained with BigMint.

At Mangalore, 5500 NAR offers were heard in the range of INR 9,200-9,300/t and 4800 NAR around INR 8,200/t exw, though no trades were concluded at these elevated levels amid low enquiries. Market participants indicated that buying interest remained subdued, with most consumers deferring purchases due to sufficient domestic supply and holiday-led slowdown.

Export market tightness lifts offers, cargo availability constrained

On the export front, RBCT-origin 5,500 NAR FOB offers increased to around $79-80/t, with CFR-India levels indicated near $93-94/t, while 4800 NAR CFR-India was quoted around $77-79/t. Market sources highlighted that January-February cargo availability remained tight, with several cargoes diverted towards South American destinations, tightening prompt supply for Asia.

A CFR Vizag offer for 5500 NAR at $91.5/t was reported for a 25-30 January laycan, though buyer response remained limited. FOB indications were also heard as high as $82/t for 5500 NAR amid rising API 4 index levels. Despite higher offers, actual trades remained scarce as buyers resisted elevated landed costs.

Domestic coal stable; auctions reflect cautious procurement

Domestic coal prices remained unchanged w-o-w, with 5,000 GCV assessed at INR 5,750/t and 4,500 GCV at INR 4,800/t. Recent SECL auctions continued to reflect cautious sentiment, with weaker participation and most bids clearing near floor prices. Only selective parcels, such as Sonepur Bazari, attracted premiums, while overall bidding remained flat, signalling adequate availability and disciplined procurement.

India’s portside thermal coal inventories declined by 2.3% w-o-w to 12.65 mnt in week 2 of 2026 from 12.95 mnt in week 1, as evacuation activity picked up after the holiday period. However, inventory levels remained comfortable overall, preventing aggressive buying at higher prices.

Sponge iron prices rise, but demand response muted

India’s sponge iron prices increased by INR 300-850/t across major regions, driven by higher offers from producers. Central India saw prices rise by INR 300-500/t, while eastern India recorded increases of INR 300-800/t. Sponge Iron (CDRI), exw-Rourkela, rose sharply by INR 1,000/t w-o-w to INR 26,000/t.

Despite the price uptick, demand remained steady to muted, as buyers restricted purchases to immediate requirements amid uncertainty around finished steel prices. Sellers continued to test higher levels, but trade volumes softened as many buyers had already covered near-term needs earlier in the week.

Outlook

South African thermal coal prices at Indian ports are likely to remain firm in the near term, supported by tight export availability, rising global thermal index levels, and limited 4800 NAR supply. However, ample domestic coal availability, cautious buying behaviour, and muted post-holiday demand are expected to cap deal closures at higher levels. Any sustained upside will depend on stronger downstream steel demand and improved trade liquidity beyond the festive slowdown.

Leave a Reply