- Seasonal softness and ample tonnage weigh on freights

- Baltic Dry Index hits six-month low on Capesize correction

Dry bulk iron ore freight rates have dropped this week amid softer capesize demand and broader dry bulk rate weakness, reflecting seasonal trade patterns and early-year market dynamics rather than a structural collapse in global dry bulk shipping.

Capesize freight rates have eased on key Brazil-China, West Australia-China and South Africa-China routes, reflecting a soft seasonal demand ahead of the Lunar New Year, weaker early-year iron ore cargo flows, and increased vessel availability, resulting in lower overall dry bulk freight costs. Also, fixture activity continues, but at lower levels, reflecting increased vessel availability and cautious chartering amid softer freight sentiment.

Beyond seasonal factors, the decline in iron ore freight rates is also being shaped by charterer caution amid mixed macro signals, including softer steel margins in China and uncertainty around near-term construction demand.

While iron ore exports from major producers remain steady, cargo release has slowed, limiting fresh enquiries in the spot market. At the same time, tonnage supply has expanded as vessels ballast into key loading areas following earlier rate strength, shifting bargaining power toward charterers. This imbalance has resulted in fixtures being concluded at discounted levels, reinforcing near-term pressure on Capesize and Supramax freight rates.

Route-wise updates

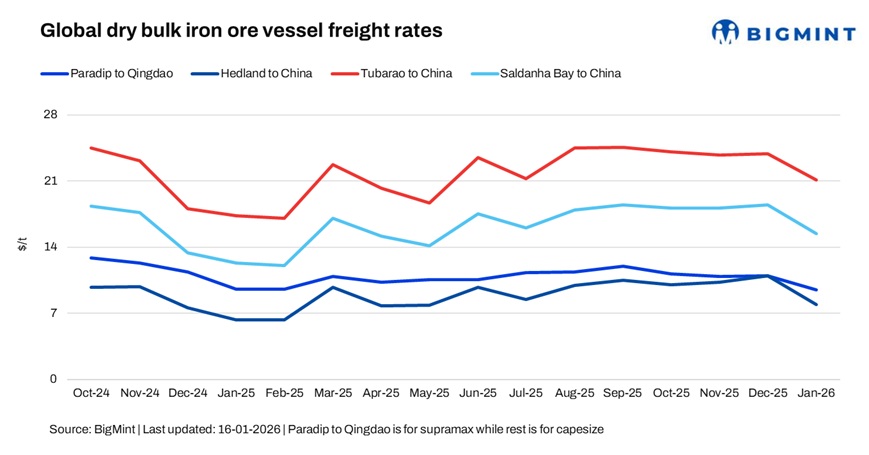

- India (Paradip)-China (Qingdao), Supramax: Freights for Supramax vessels from the Indian Ocean to China fell by $0.4/dry metric tonne (dmt) w-o-w to $9.1/dmt on 16 January.

- Australia (Port Hedland)-China (Qingdao), Capesize: Capesize freights for iron ore shipments from Western Australia to China declined by $0.8/dmt w-o-w to $7.2/dmt.

- Brazil (Tubarao)-China (Qingdao), Capesize: Capesize freights for Brazil-China iron ore shipments dropped by $2.3/dmt w-o-w to $19.2/dmt.

- South Africa (Saldanha Bay)-China (Qingdao), Capesize: Capesize freights from Saldanha Bay to Qingdao down by $2.1/dmt w-o-w to $13.9/dmt.

Market highlights

- Baltic dry index hits six-month low: The Baltic dry index declined by 10.8% (186 points) w-o-w to 1,532 on 15 January. Fall in index is due to a sharp Capesize correction, driven by softer iron ore demand sentiment, increased vessel availability in key loading regions, and profit-taking after recent gains, while strength in smaller segments was insufficient to offset the decline.

- Brent crude futures increase w-o-w: Brent crude oil futures rose by around $1.87/bbl w-o-w to $64.5/bbl for the March 2026 contract on 16 January. Brent crude rose w-o-w supported by supply-side discipline, geopolitical risk premium, and expectations of tighter balances in early 2026, despite lingering concerns over global demand growth.

- DCE iron ore futures decrease w-o-w: Iron ore futures on the Dalian Commodity Exchange dropped by RMB 5/t ($0.7) w-o-w to RMB 812/t ($117/t) on 16 January. Iron ore futures on the DCE declined w-o-w amid cautious steel demand outlook, seasonal slowdown in construction activity, and easing restocking momentum, which weighed on near-term price sentiment.

Outlook

In the near term, iron ore freight rates are expected to remain under pressure, with the Capesize segment likely to stay rangebound as seasonal softness persists ahead of the Lunar New Year and vessel supply remains ample in key loading regions.

Limited spot cargo enquiries and cautious chartering are expected to keep fixtures at lower levels. However, the downside may be capped as iron ore export volumes are unlikely to decline materially, and any post-holiday rebound in Chinese steel production, coupled with improved demand visibility.

Leave a Reply