- G11 coal dominate volumes, fetches sub-1% premiums

- Rama Coal Washeries largest bidder followed by Vedanta

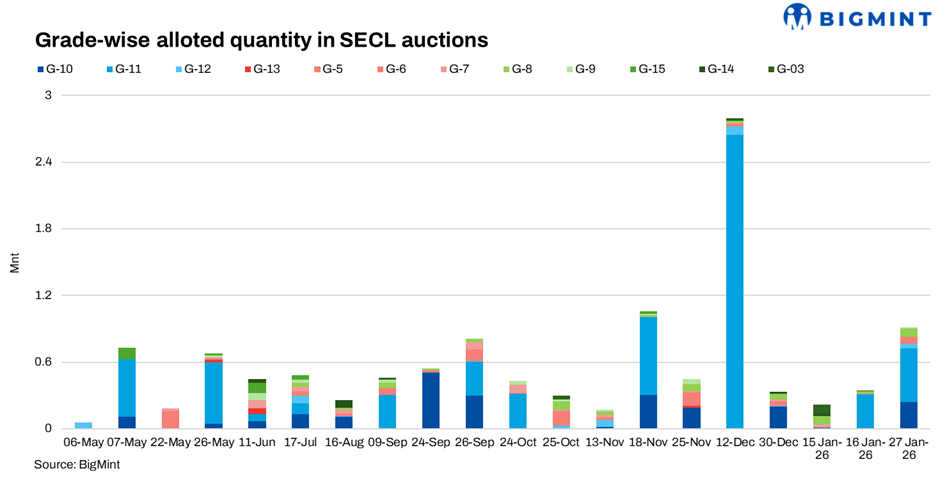

South Eastern Coalfields Limited conducted a non-coking coal auction on 27 January 2026, offering 1,716,050 t, of which 915,200 t was allocated. Buying remained selective, with a clear split between bulk mid-CV grades clearing near floors and smaller industrial grades attracting sharp premiums.

Mid-CV grades dominate volumes, y application

G11 formed the backbone of the auction, accounting for 481,450 t, or more than half of total allocations. The grade cleared at an average winning price of INR 1,430/t against a floor price of INR 1,418/t, reflecting a marginal premium of about 0.8% amid ample availability and steady utility-led demand. Large opencast mines such as Gevra OC and Kusmunda OC together supplied over 440,000 t of G11, anchoring volumes and preventing aggressive bidding.

G10 emerged as the second-largest grade, with 244,150 t allocated at an average winning price of INR 1,863/t versus a floor of INR 1,628/t, implying a premium of around 14%. Demand was supported by industrial and cement buyers seeking a balance between calorific value and cost. Amadand OC and Dipka OC together contributed a significant share of G10 volumes, with Amadand OC achieving higher realisations, lifting the grade average.

Industrial grades record sharp premiums

Premium intensity increased sharply in smaller-volume industrial grades. G8 recorded one of the strongest performances, with 74,000 t sold at an average winning price of INR 3,258/t against a floor of INR 2,312/t, translating into a premium of roughly 41%. Buyers competed selectively for quality parcels from mines such as Kanchan OC and Amera OC, reflecting steady demand from sponge iron and industrial consumers.

G6 also attracted firm interest, with 60,000 t clearing at INR 3,375/t versus a floor of INR 3,305/t, implying a premium of around 2%. In contrast, G12 volumes of 41,800 t cleared exactly at the floor price of INR 1,318/t, highlighting strict price discipline in lower-CV, utility-linked segments.

Smaller grades such as G9 and G7 saw pronounced premiums despite limited volumes. G9 cleared 10,000 t at INR 2,214/t against a floor of INR 1,803/t, reflecting a premium of about 23%, while G7 achieved INR 3,493/t versus a floor of INR 3,040/t, implying a premium close to 15%, driven largely by UG-origin parcels such as Rehar UG.

Buyers engage in targeted, need-based procurement

Buyer participation was broad but measured. Rama Coal Washeries emerged as the largest buyer, lifting 100,000 t of G11 at INR 1,418/t, followed by Vedanta Limited with 80,000 t of G11 at similar levels. Agarwal Coal Corporation lifted close to 60,000 t across G10, G11 and G6, reflecting mixed-grade procurement. Cement and industrial buyers such as UltraTech Cement, Hind Unitrade, Singhal Enterprises and Jai Bhole Enterprises focused on G8, G10 and G6 parcels, indicating application-specific buying rather than volume accumulation.

Mine-wise outcome underscores segmentation

Mine-level data reinforced the segmented nature of the auction. Bulk G11 supply from Gevra OC and Kusmunda OC cleared at marginal premiums, while UG-linked and select OC parcels in G6, G8 and G7 fetched materially higher prices. Gayatri UG supplied the entire G6 volume at INR 3,375/t, while Rehar UG recorded the highest realisation in the auction at INR 4,247/t for G7, underscoring scarcity-driven bidding for cleaner UG coal.

Takeaway

The 27 January SECL auction reaffirmed a segmented domestic coal market. Bulk mid-CV grades such as G11 cleared large volumes near floor prices, reflecting comfortable supply, while smaller industrial grades attracted double-digit to over 40% premiums due to limited availability and steady end-use demand. Overall bidding remained disciplined, pointing to controlled restocking rather than any demand-led surge.

Leave a Reply