- L&T posts strong figures on rising infrastructure, hydrocarbon demand

- APSEZ delivers healthy cargo growth, maintains robust FY26 guidance

India’s infrastructure sector maintained strong momentum in Q2FY26, with major companies delivering solid operational progress and healthy financial results across transportation, energy, and logistics. The quarter saw steady project execution, improving traffic and cargo flows, and continued capital investment, highlighting the sector’s resilience despite changing demand conditions.

Updates from L&T, APSEZ, IRB, KPIL, and GRIL show broad-based growth and reaffirm the sector’s key role in driving India’s long-term infrastructure and economic development.

Performance highlights

1. Larsen & Toubro (L&T) delivered a strong performance in Q2FY26, driven by healthy order inflows and steady execution. The company’s order inflows surged 23% q-o-q to INR 1,158 billion as against INR 945 billion in Q1FY26. On a y-o-y basis, order inflows rose 45%, compared with INR 800 billion in Q2FY25, supported by robust demand in the infrastructure and hydrocarbon segments.

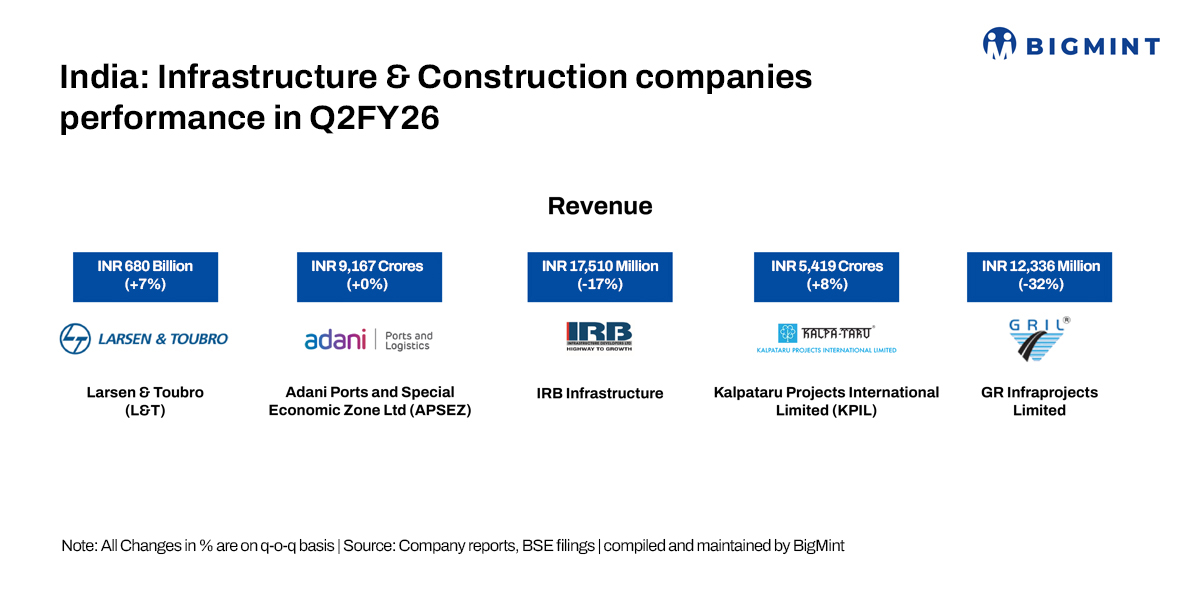

Revenue grew 7% q-o-q to INR 680 billion in Q2FY26, against INR 637 billion in Q1FY26, and increased 10% y-o-y from INR 616 billion in Q2FY25. On the profitability front, EBITDA climbed 8% q-o-q to INR 68.1 billion, compared with INR 63.2 billion in the previous quarter, and was up 7% y-o-y from INR 63.6 billion in Q2FY25.

The company’s consolidated order book stood at INR 6,670 billion as of 30 September, marking a 9% q-o-q increase from INR 6,128 billion in Q1FY26 and a 31% y-o-y rise from INR 5,104 billion in Q2FY25. International orders accounted for 49% of the total order book. The company reported a strong prospect pipeline of around INR 6.5 trillion for the near term, indicating continued order visibility.

2. Adani Ports and Special Economic Zone (APSEZ) delivered a strong performance in Q2FY26, handling 124 million tonnes (mnt) of cargo, marking a 2% q-o-q growth as compared to 121 mnt in Q1FY26. On a yearly basis, the same was up by 12% from 111 mnt. The growth was primarily supported by a 20% rise in container volumes, with Krishnapatnam Port recording its highest-ever monthly cargo at 5.85 mnt in June.

On the financial front, revenue remained almost stable to around INR 9167 crores. Meanwhile on y-o-y basis , the revenue rose to 30% as compared with INR 7,067 crore in Q2FY25. However, on q-o-q basis EBITDA stood at INR 5,550 crore, up by 1% from INR 5,495 crore in Q1FY26. On a yearly basis, the same increased by 27% from INR 4,369 crore in Q2FY25.

Reaffirming its positive outlook, the company retained its FY26 guidance, projecting revenue of INR 36,000-38,000 crore, EBITDA of INR 21,000-22,000 crore, and capex of INR 11,000-12,000 crore. Backed by a strong order pipeline and sustained demand momentum, port cargo volumes are expected to reach 505-515 mnt in FY26, highlighting APSEZ’s expanding presence in India’s logistics and port infrastructure landscape.

3. IRB Infrastructure reported a resilient performance in Q2FY26, with total income of INR 18,003 million compared to INR 21,646 million in Q1FY26, reflecting normalization after a strong first quarter. EBITDA stood at INR 9,739 million, maintaining a robust 56% margin, supported by stable toll revenues and cost efficiency. Toll revenue grew 11% y-o-y, driven by strong traffic growth across Private InvIT assets, the Mumbai–Pune Toll–Operate–Transfer (TOT), and Ahmedabad–Vadodara Build–Operate–Transfer (BOT) projects.

During the quarter, the company achieved key milestones, including the completion of the Vadodara–Mumbai Expressway (Package 7) and operationalization of Hyderabad ORR, Lalitpur–Lakhnadon, and Jhansi–Gwalior–Kota TOT projects. Construction of the Ganga Expressway and other HAM projects is progressing well. PAT surged 41% y-o-y to INR 1,408 million. With a strong order book, low leverage, and favourable sector outlook, the company remains well-positioned for sustainable growth in FY26.

4. Kalpataru Projects International Ltd (KPIL) posted a strong performance in Q2FY26, achieving record revenues and steady profitability backed by robust execution and a healthy order pipeline. Standalone revenue rose 8% q-o-q to INR 5,419 crore as against INR 5040 crores in Q1FY26 and 31% y-o-y from INR 4,136 crore in Q2FY25, while consolidated revenue grew 32% y-o-y to INR 6,529 crore, driven by strong execution across the Transmission & Distribution (T&D), Buildings & Factories (B&F), Oil & Gas, and Urban Infrastructure segments.

Order inflows during the quarter stood at INR 14,951 crore, up 51% q-o-q from INR 9,899 crore in Q1FY26 and 26% higher y-o-y compared to INR 11,865 crore in Q2FY25, led by robust traction in the B&F and T&D businesses. The consolidated order book stood at INR 64,682 crore as of 30 September 2025, reflecting a 7% y-o-y increase, though marginally lower by 1% q-o-q compared to INR 65,475 crore in Q1FY26. With its diversified EPC presence and execution capabilities, KPIL remains well-positioned to capitalize on upcoming infrastructure opportunities.

5.GR Infraprojects Ltd (GRIL) reported revenue of INR 12,336 million in Q2FY26, up 9% y-o-y from INR 11,280 million, though lower 32% q-o-q from INR 18,261 million due to execution timing. EBITDA stood at INR 1,204 million, rising 3% y-o-y, but declining 48% q-o-q from INR 2,311 million.

As of 30 September, the company’s order book stood at INR 211,149 million, up 44% y-o-y from INR 1,46,405 and 9% q-o-q from INR 1,94,104, with roads contributing 65%, transmission 13%, and the balance from tunnels, railways, and other infrastructure projects. Recently, GRIL was declared L1 bidder for two road projects worth INR 42,960 million, which will expand its order book to INR 254,108 million, further strengthening revenue visibility and long-term growth prospects.

Leave a Reply