- Tin production in Yunnan remains constrained

- Optimism on US Fed rate cuts boosts confidence

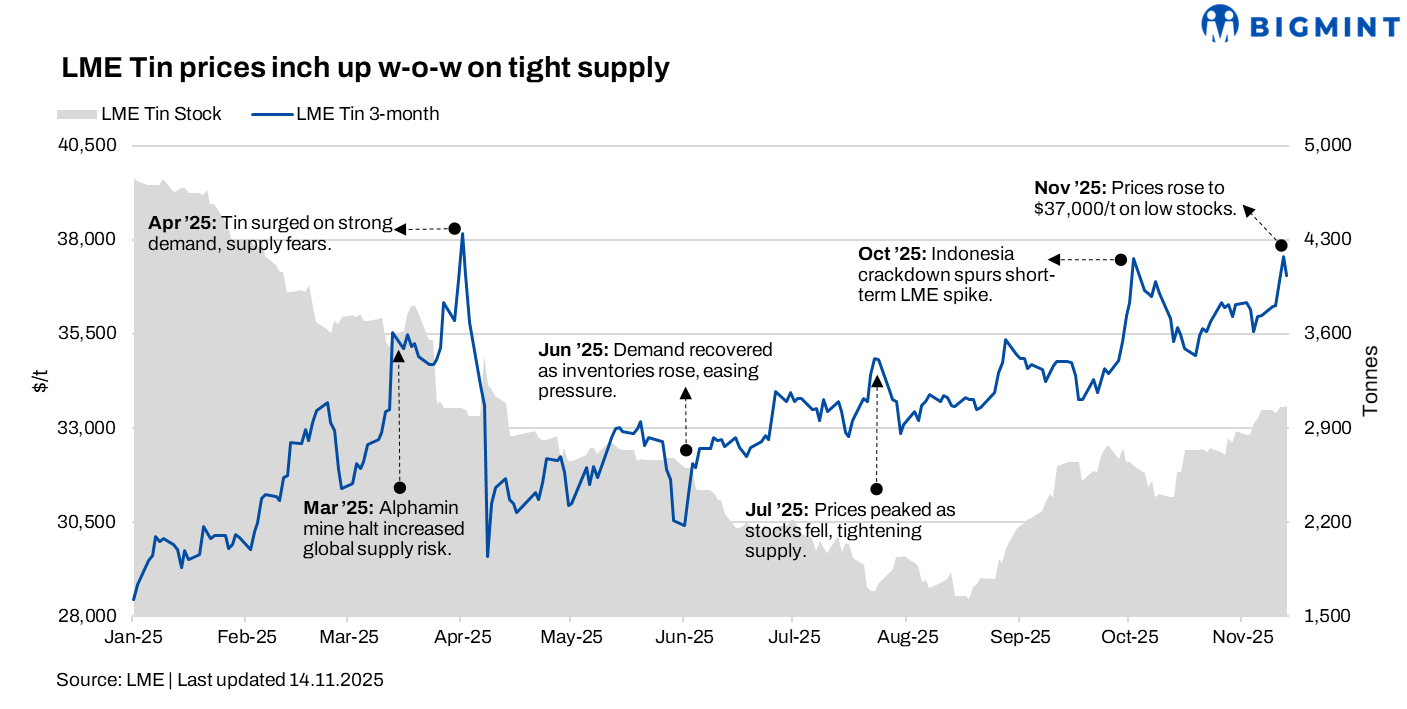

LME Tin prices gained during week 46 of CY’25 (10-14 November), keeping up the firm trend, amid persistent supply concerns. Tin prices were supported by a tight supply and a slightly brighter market mood. Optimism that the US government shutdown would be resolved, along with hopes of Federal Reserve interest rate cuts, boosted confidence and lifted appetite for risk across commodity markets. Still, worries about US-China trade tensions and signs of slowing global growth kept a lid on how high tin prices could go.

Pricing, inventory trends

LME Tin prices averaged $36,806/tonne (t) in week 46, marking an $800/t or 2% rise w-o-w from week 45 (03-07 November). The week began with prices at $36,225/t, which inched up to around $36,925/t mid-week and closed at $35,070/t.

Meanwhile, Tin inventories at LME-registered warehouses rose to 3,045 t from 2,932 t in week 45.

What impacted prices this week?

On the supply side, disruptions continued to tighten Tin availability. Production in key regions such as Yunnan remained constrained, and most smelters are expected to maintain relatively stable production in November, while Indonesia’s refined Tin exports in October plunged 54% y-o-y, heightening concerns over global supply shortages. Against this backdrop, the most-traded SHFE Tin contract surged to a new record high of RMB 298,500/t. In the near term, SHFE tin prices are expected to remain elevated.

Outlook

Tin prices are expected to remain firm, driven by the resumption of production in Myanmar, progress in US-China trade talks, and forthcoming guidance on the Federal Reserve’s policy, all of which are likely to influence near-term market movements.

Leave a Reply