- India’s copper scrap demand stays resilient

- Japan’s smelters face margin squeeze, plan output cuts

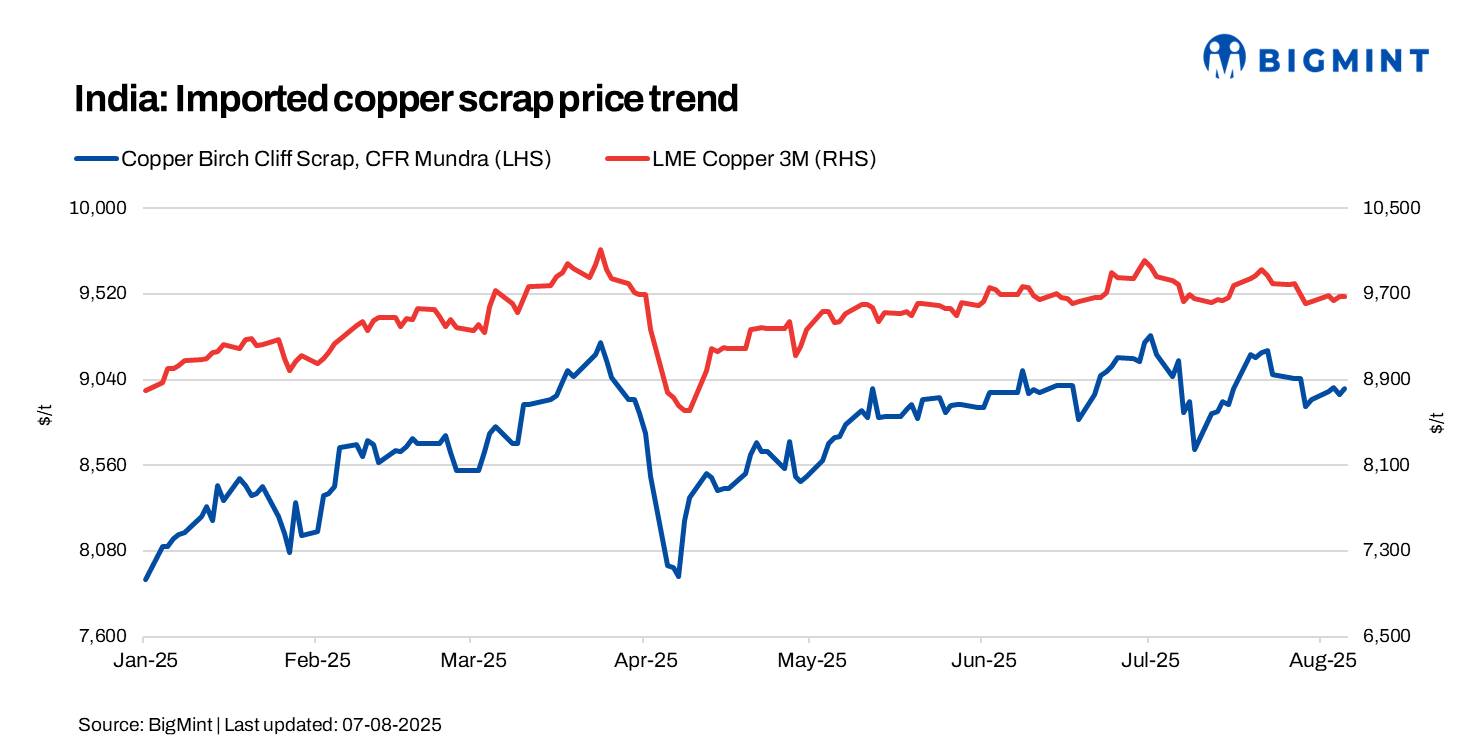

Imported copper scrap prices in India registered a modest w-o-w gain, despite a 1.24% drop in LME copper futures to $9,676/tonne. The LME downturn was driven by persistent supply constraints and continued uncertainty surrounding potential US import tariffs. LME futures also remained below the recent three-month peak of $10,005/t (recorded on July 3), adding mild bearish pressure to domestic scrap pricing sentiment.

According to BigMint’s assessment, copper Birch cliff scrap was assessed at $8,990/t, up by 1.12% w-o-w, while US motors mix stood at $1,170/t (both CFR Mundra), stable w-o-w.

Market scenario

The United States has imposed a 50% tariff on all semi-finished copper imports, including pipes, wires, rods, and related products. However, copper cathodes and copper scrap remain exempt from the new tariff, allowing continued international trade in those materials.

Despite this exemption, the US government has proposed new export controls targeting high-quality copper scrap. A key recommendation is that 25% of domestically produced high-grade scrap must be sold within the country to ensure adequate local supply. If implemented, this policy could reduce the volume of copper scrap available for export.

Scrap dealers are concerned about the lack of clarity on how “high-quality” scrap will be defined and monitored. The absence of clear guidelines is causing uncertainty and delays for exporters, particularly those reliant on predictable trade flows.

In the short term, this may lead to increased copper scrap availability within the US and reduced outbound shipments. If further restrictions are introduced, global buyers — especially in Asia — could face tightened supply and upward price pressures.

A trader stated, “India’s copper scrap market remains supported despite logistical headwinds due to the ongoing monsoon season, which has impacted operations at scrap yards and downstream wire rod units. Additionally, stricter BIS quality compliance checks have led to extended import clearance timelines at key ports, prompting some buyers to shift toward consistent, pre-inspected suppliers”.

Demand from the secondary manufacturing segment — particularly cable and conductor producers continue to drive buying interest for clean, high-grade copper scrap with prompt delivery.

High-grade imported scrap categories such as Millberry and Birch/Cliff remain in focus. Offers for Millberry from the US and Europe are currently quoted at premiums of 102-103% over the 3-month LME, reflecting tight availability and sustained buyer appetite.

However, market sources indicate that South Korean buyers are offering more competitive realisations — up to 93.5% for Birch/Cliff and 101-102% for Millberry — leading some European and Australian suppliers to divert cargoes away from India. Despite this, Indian buyers continue to secure material for immediate needs, with deals reported around flat LME levels for quick-delivery cargoes.

Europe market

Copper scrap prices remained largely stable over the week, supported by steady demand from secondary smelters facing refined cathode shortages. Many smelters had redirected their supply chains toward the US market in anticipation of tariff shifts, tightening prompt availability and keeping prices firm for immediate delivery material.

Price levels

- Millberry (US/Europe origin): 99-100% LME

- Candy Berry (Europe): 97.5-98.5% of LME

- Birch/Cliff (Europe): 91-93.5% of LME

Traders noted that despite seasonal slowdowns due to the summer holidays, buying activity from refiners and secondary smelters — particularly in southern Europe — remains stable. However, some downside pressure has emerged from increased availability of secondary raw materials and cautious sentiment amid global macroeconomic uncertainty.

Meanwhile, European recyclers are closely monitoring demand trends in Asia, especially in South Korea, where aggressive bidding has recently diverted high-grade scrap away from European markets.

Japan market update

Mitsubishi Materials is considering a partial cut in copper concentrate processing at its Onahama smelter in Fukushima after scheduled maintenance in October-November, as falling treatment and refining charges (TC/RCs) have eroded smelting profitability. The smelter, with a monthly copper cathode capacity of 25,000 t, will maintain scrap-based operations, which are less affected by TC/RCs.

Outlook

India’s copper scrap market is expected to remain firm in the near term, supported by steady secondary sector demand and resilient procurement activity despite ongoing monsoon-related disruptions. While US copper scrap remains exempt from recent tariffs, the proposed export restrictions and evolving definitions of “high-quality” scrap are likely to create global supply uncertainties.

Leave a Reply