- 300-series dominates with 46% share in total Q1 sales

- Capacity utilisation at 85% in Q1, target to breach 90%

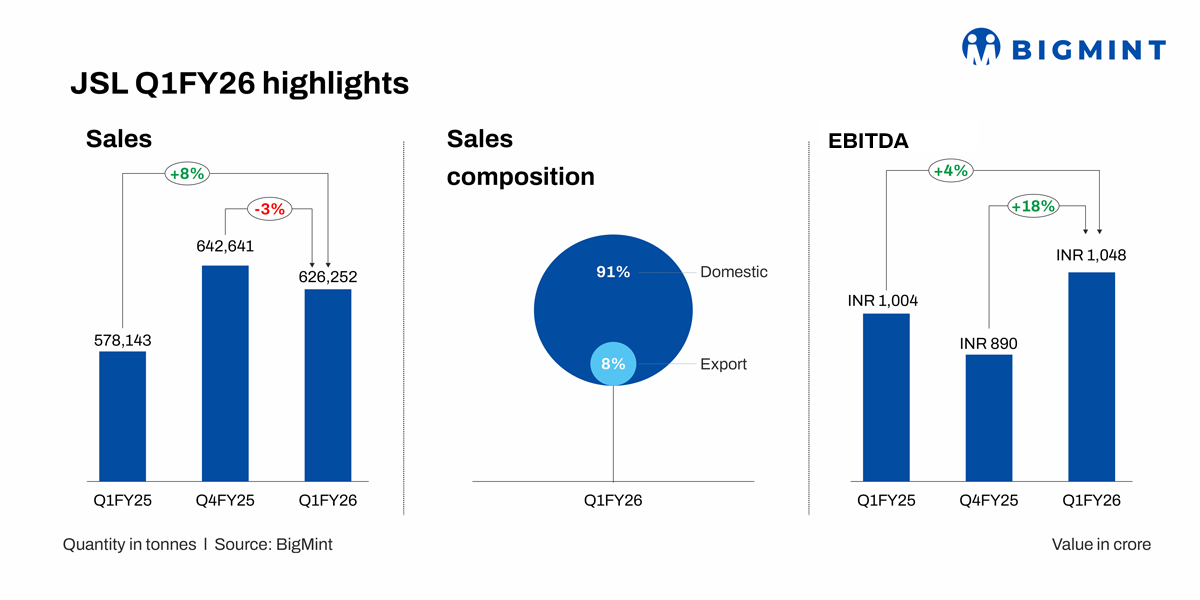

India’s largest stainless steel producer Jindal Stainless Ltd (JSL) struck a confident tone in its Q1FY’26 earnings call, projecting 9-10% y-o-y volume growth for the fiscal year, underpinned by resilient domestic demand and ongoing capacity enhancements.

Sales

Sales volumes in Q1 grew 8% y-o-y to 676,252 tonnes (t), while remaining flat q-o-q, driven by strong offtake from auto, railway, lift, and white goods sectors.

Series-wise, the 300 series continued to dominate at 46% of sales, followed by 200 series at 36% and 400 series at 18% – reflecting a stable product mix.

EBITDA

EBITDA rose sharply to INR 1,303 crore, up 11% y-o-y and 21% q-o-q, aided by a better product mix, rising share of special-grade volumes, and tighter cost control.

JSL reinforced its domestic-first strategy, noting robust demand from metro and railway projects. Export push remains on the backburner amid global market volatility. The company continues to deepen its presence in defence and aerospace steel applications, including supplies for ATGMs and naval platforms – low in volumes but strategic in value.

Product mix

Product innovation also featured, with the ‘Jindal Saathi’ co-branding initiative now expanding from pipes and tubes to kitchenware and sinks. Cold rolled volumes rose 12% q-o-q, and the company aims to expand chrome-line capacity further to boost CR output.

Capacity utilisation

Capacity utilisation stood at 85% in Q1, with a target to breach 90% as new lines ramp up. Capex guidance for FY’26-27 remains unchanged at INR 2,700 crore. Land acquisition for the 1 million tpa Maharashtra unit is progressing, while commissioning of the Indonesian SMS and United Steel’s HRAP line remains on track for FY’27.

Update on trade measures

On trade actions, JSL said ISSDA has filed for anti-dumping probes against China, Vietnam, and Indonesia. BIS certification norms continue to restrict sub-par imports, supporting domestic realisations.

Subsidiary update

Rathi unit

The Rathi unit operated at a healthy 80-85% capacity utilisation during Q1 FY26, with a primary focus on rebar and wire rod production. While rebar sales witnessed a temporary slowdown during the quarter, a recovery is anticipated in the upcoming quarter, supported by improving market dynamics.

Other subsidiaries:

All other subsidiaries are progressing in line with the company’s strategic growth roadmap, contributing steadily to the overall business performance.

Raw material outlook

On raw materials, the company expects nickel prices to hover in the $14,000-$16,000/t range, with stainless prices moving in tandem. JSL continues to rely on natural hedging to navigate volatility.

Leave a Reply