- Sponge iron prices drop INR 200/t d-o-d

- Semis, finished steel prices decline on weak buying

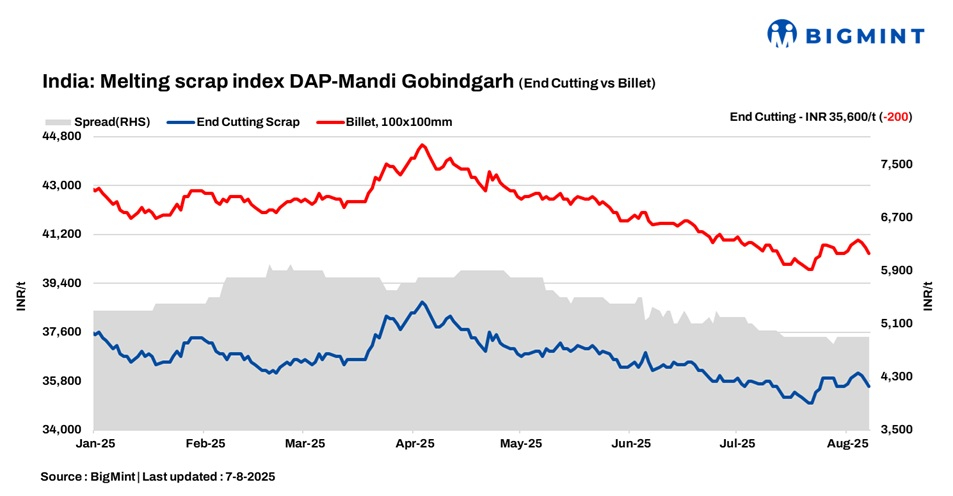

BigMint’s domestic end-cutting scrap index, tracking the Mandi Gobindgarh market, further declined by INR 200/tonne (t) d-o-d to INR 35,600/t DAP on 7 August 2025. Scrap prices in the region have been on a continuous downward trajectory over the past few days, driven by subdued buying interest and a cautious procurement approach adopted by buyers. The prevailing uncertainty and lack of strong demand are contributing to weak market sentiment, slowing overall trading activity in the scrap market.

Raw material prices

Sponge iron (CDRI) prices in Mandi Gobindgarh continued their downward trend, falling by another INR 200/t today. It is now assessed at INR 30,000/t DAP. This marks a cumulative drop of INR 300/t over the past few days, reflecting a muted buying trend and cautious procurement by secondary steel producers.

On the other hand, pig iron prices in Ludhiana (Punjab) remained stable for the third consecutive day, assessed at INR 35,800/t DAP. Market activity has been largely stagnant, with limited trade movement observed, indicating a wait-and-watch approach among buyers.

Steel market trends

The semi-finished steel market in Mandi Gobindgarh continued to face downward pressure, with prices dropping by INR 200/t d-o-d, settling at INR 40,500/t DAP. The sustained decline highlights ongoing sluggishness in buying activity, which is keeping overall market sentiment subdued. Ingot prices in the region have now returned to levels last seen a week ago, signaling stagnation in demand.

In the finished steel segment, rebar prices also saw a correction, falling by INR 200/t d-o-d. Rebar (Fe500) is now assessed at INR 45,700/t ex-works, in line with the broader trend of limited trade volumes and cautious market participation.

Overview of Hyderabad market

Hyderabad’s steel market remained largely stable today, though overall activity was subdued. Market sources reported weak demand for billets at current price levels, with buyers remaining inactive. Despite the muted interest, sellers are holding firm on prices, buoyed by a positive long-term outlook for the steel sector.

In the finished steel segment, trading activity for rebar (Fe500) remained low to moderate. Buyers are cautious, with limited spot procurement observed amid rangebound price movement and broader market uncertainty.

On the semi-finished front, billet prices in the region remained unchanged d-o-d at INR 39,500/t ex-works. In the finished steel segment, rebar (Fe500) prices were also steady at INR 43,500/t ex-works.

Raw material prices maintained stability, supported by current auction trends. Sponge iron (PDRI) prices remained firm at INR 25,900/t ex-works. Meanwhile, HMS (80:20) scrap prices were flat at INR 29,300/t delivered at plant (DAP), reflecting a balance between cautious buying and steady supply.

Upcoming scrap auctions

Price highlights

End-cutting-billets spread: In Mandi, the end-cutting scrap and billet spread stood at INR 4,800-5,200/t.

Domestic vs imported scrap: Imported melting scrap prices at Nhava Sheva Port were at $335/t, which equates to approximately INR 31,512/t (including freight). HMS (80:20) prices in Mumbai remained stable at INR 31,300/t DAP today. Indicative prices of shredded from Europe stood at $365/t CFR Nhava Sheva.

Raipur sponge iron-billet spread: The conversion spread (margin) between pellet-based DRI (P-DRI) and steel billets in Raipur stood at INR 13,050/t.

To check BigMint’s melting scrap assessment, pricing methodology, and specification documents, click here.

Leave a Reply