- Imports remain soft as buyers resist higher offers

- Monsoon, liquidity strains cap market momentum

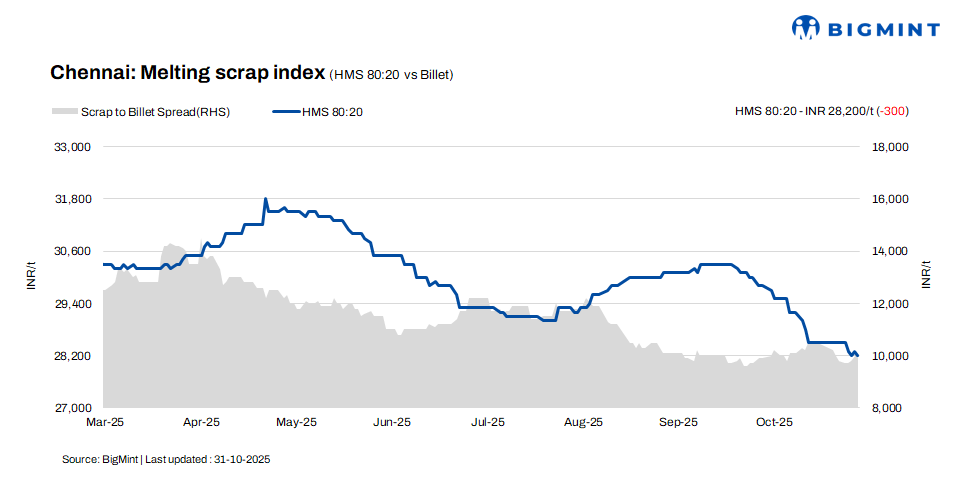

According to BigMint’s latest assessment, HMS (80:20) scrap prices eased by INR 100/t d-o-d to INR 28,200/t, extending their weekly decline to INR 300/t. Billet prices held steady at INR 38,300/t d-o-d but registered a minor fall of INR 200/t on a w-o-w basis. Rebar prices, on the other hand, dropped INR 100/t w-o-w but gained INR 200/t d-o-d, assessed at INR 43,200/t. Overall, the market displayed a mixed trend, with marginal recovery seen in daily trade sentiment.

Imported, domestic market trends

Imported shredded scrap offers are reported at $345-350/t, while buyer bids are slightly lower at $340-345/t. HMS (80:20) scrap is being quoted at $330-335/t, with bids hovering around $320-325/t, reflecting a consistent $5-10/t bid-offer spread. Market sentiment remains under pressure due to weak finished steel demand and limited buying interest. The ongoing monsoon season is further dampening trade activity and restricting price movement, leading participants to adopt a cautious stance in the short term.

In the domestic market, HMS (80:20) scrap prices were reported in the range of INR 28,000-28,500/t for buyers making immediate payments, while offers for extended payment terms were slightly higher at INR 28,500-29,000/t. Most transactions were concluded within the INR 28,000-29,000/t range, indicating overall price stability. Market participants are maintaining a cautious approach, with bids closely aligned to liquidity conditions and payment flexibility.

Buyer-supplier sentiments

Market sources report that steel trade activity is yet to recover following the Diwali holidays. The Mantha cyclone alert and subsequent heavy rainfall have disrupted logistics and slowed overall market movement in the region. Additionally, the onset of the monsoon season has further dampened buying sentiment in finished steel, as buyers remain cautious amid weak end-user demand and uncertain weather conditions.

According to a leading scrap supplier, HMS (80:20) scrap traded in the range of INR 28,000-29,000/t, with price realizations largely dependent on payment terms. Liquidity challenges continue to exert pressure on market sentiment, though a marginal improvement in finished steel trade activity has been noted in recent sessions. However, most mills continue to hold finished steel inventories of around 15-20 days, indicating subdued demand and cautious buying in the near term.

Regional comparison

In the western India-based Jalna market, HMS (80:20) scrap prices inched up by INR 100/t to INR 28,800/t, while billet prices rose by INR 200/t to INR 37,500/t. Rebar offers also gained INR 500/t, reaching INR 42,900/t. Market sources reported improved trade activity in finished steel over recent sessions. Stable scrap availability continues to support mill operations, enabling producers to maintain output levels in line with steady regional demand and firm market sentiment.

Outlook

Market participants expect domestic scrap prices to remain largely stable, with a possible marginal dip of INR 200-500/t in the near term. The onset of the monsoon season in Chennai has prompted major finished steel buyers to adopt a cautious approach, limiting trade activity across the region. This subdued sentiment is likely to keep overall steel market momentum restrained in the short run.

Leave a Reply