- Capex at INR 3,375 crore in H1FY’26

- Sales volumes up 7% q-o-q to 4.9 mnt

PSU steelmaker Steel Authority of India Limited (SAIL) reported a q-o-q decline in crude steel production, while saleable steel output and sales volumes improved in Q2FY’26. The company incurred a capex of INR 3,375 crore in H1FY’26, surpassing its target, and aims to exceed INR 7,500 crore for the full year. The company is progressing with its 4.5 mnt capacity expansion at ISP (ISCO), involving an investment of about INR 33,000 crore, BigMint at SAIL’s investor call held on 30 October.

Key highlights

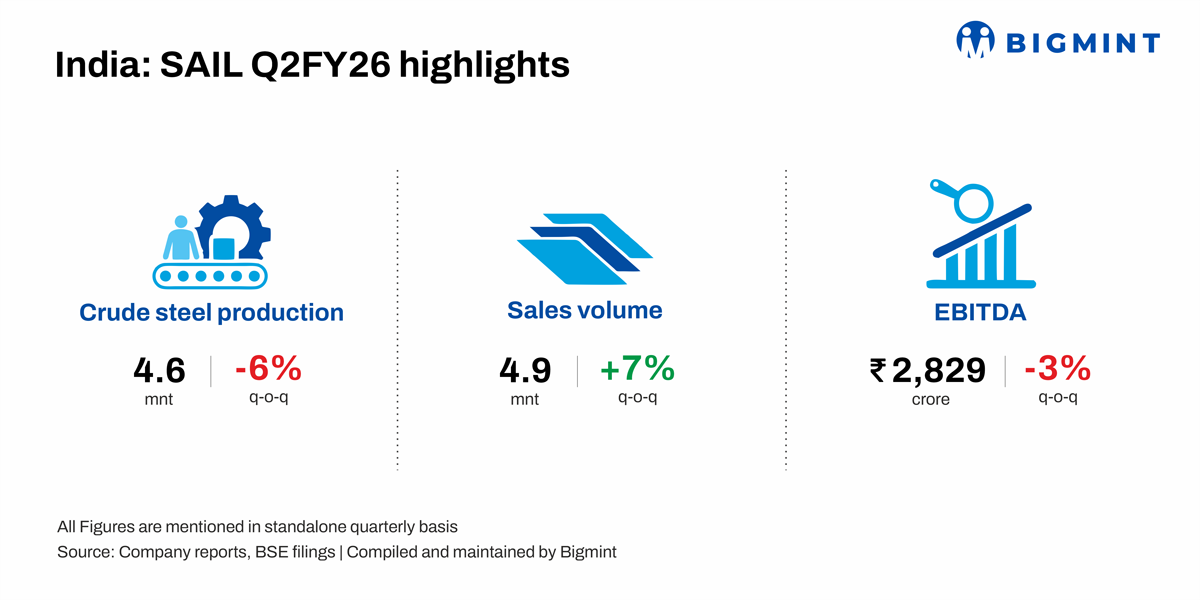

Crude steel production dips q-o-q: The company’s crude steel output fell 6% q-o-q to 4.6 mnt in Q2FY’26 from 4.9 mnt in Q1FY’26. Y-o-y, production was down 4% from 4.8 mnt in Q2FY’25.

Saleable steel production inches up q-o-q: Saleable steel production rose 4% q-o-q to 4.9 mnt in Q2FY’26 compared with 4.7 mnt in Q1FY’26, and increased 7% y-o-y from 4.6 mnt in Q2FY’25.

Sales volumes rise q-o-q: Sales volumes grew 7% q-o-q to 4.9 mnt in Q2FY’26 from 4.6 mnt in the previous quarter and surged 20% y-o-y from 4.1 mnt in Q2FY’25.

EBITDA declines q-o-q: EBITDA decreased 3% q-o-q to INR 2,829 crore in Q2FY26 from INR 2,925 crore in Q1FY26 and was down 11% y-o-y from INR 3,174 crore in Q2FY25.

Revenue from operations up y-o-y: Revenue from operations increased 8% y-o-y to INR 52,625 crore in Q2FY26 from INR 48,672 crore in Q2FY25, though it was marginally lower on a q-o-q basis.

Inventory levels: Finished steel inventory stood at around 1.9 mnt as of 30 September 2025. Process stock reduced slightly, with opening inventory at 2.72 mnt and closing at 2.69 mnt.

Capex and debt position: The company incurred a capex of INR 3,375 crore in H1FY26, exceeding its target, and aims to surpass INR 7,500 crore for the full year. The company plans to further reduce debt to create financial flexibility for upcoming expansion projects.

Net sales realisation (NSR): Despite lower steel prices, improved sales of by-products and scrap supported overall realizations in Q2. The average NSR declined by around INR 2,700/t q-o-q, led by a drop of INR 5,500/t in long product prices and INR 1,700/t in flat product prices. However, the company expects realizations to improve from mid-November, in line with seasonal trends.

Coking coal prices: Imported coal prices averaged around INR 17,300/t in October, up INR 700/t from August levels due to rupee depreciation against the USD. The coal index increased from 187 in September to 194 in October, reflecting firm market conditions. The average coking coal cost in Q2 stood at INR 17,400/t, while imported coal averaged INR 18,150/t. Prices are expected to remain elevated in Q3 amid improving demand, possibly reaching INR 18,000/t.

Expansion projects: The company is progressing with its 4.5 mnt capacity expansion at ISP (IISCO) involving an investment of about INR 33,000 crore. Most major packages have been finalized, with the remaining to be placed in the next few months. Design and engineering work will follow, with major capex outflows expected from FY’27 onward.

Leave a Reply