- India’s portside thermal coal inventories inch up w-o-w

- RB2 coal offers rise marginally, RB3 offers edge down

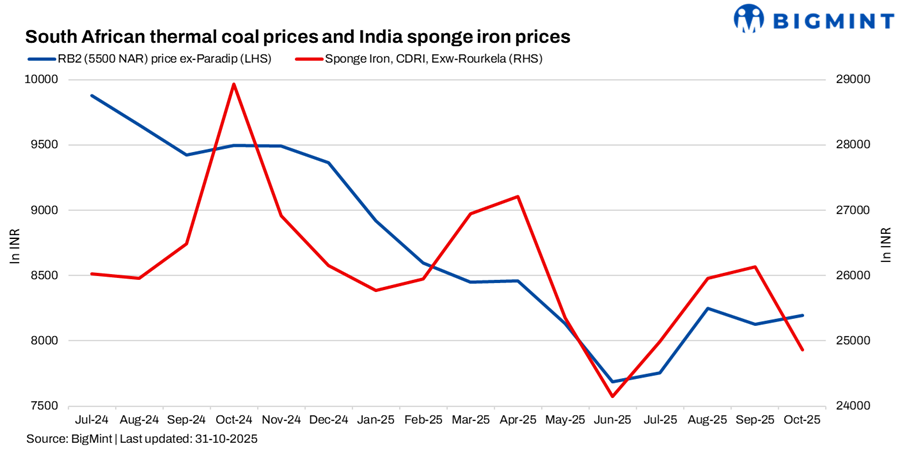

South African portside thermal coal offers in India remained largely unchanged w-o-w, with RB2 (5500 NAR) assessed at INR 8,200/t and RB3 (4800 NAR) at INR 7,100/t across Paradip, Vizag, and Gangavaram. Post-festive sluggishness and cyclone-related disruptions along the east coast kept trade activity muted. Most buyers, having restocked earlier, stayed cautious as industrial consumption remained subdued.

Why have inquiries for South African coal dropped?

- Increase in stocks at Indian ports – India’s portside thermal coal inventories inched up 1.2% w-o-w to 13.33 million tonnes (mnt) in week 43 from 13.17 mnt in week 42.

- India’s sponge iron output hits 7-month low in Sep – India’s sponge iron output dropped to a 7-month low of 4.71 mnt in September reflecting production curtailment due to weaker end-user consumption and reduced coal intake. With limited enquiries and logistical delays in lifting earlier cargoes, coal procurement remained minimal despite marginal price gains.

- Sponge iron prices rise but trade activities remain limited – In the sponge iron market, BigMint’s C-DRI index (ex-Rourkela) climbed by INR 700/t w-o-w to INR 24,700/t. Yet, the sentiment remained cautious, with buyers refraining from bulk procurement at higher levels due to existing inventories and logistical delays in lifting previously booked cargoes.

- Improved bookings in recent domestic coal auctions – Domestic coal prices, however, firmed up after SECL allocated 728,000 t through its auctions held on 24-25 October. The 5,000 GCV grade rose to INR 6,350/t ex-Bilaspur, while 4,500 GCV edged up to INR 5,200/t, reflecting gains of INR 50-100/t w-o-w. SECL allocated around 728,000 tonnes of coal through auctions on 24-25 October 2025.

- Coal FOB offers from South Africa remain range-bound – On the export front, South African RB2 offers edged up by $0.5/t w-o-w to $72/t FOB, while RB3 slipped by $1/t to $59/t. Offers from RBCT stayed firm amid cargo shortages and limited fixing activity ahead of the year-end Christmas holidays. Panamax freight rates on the South Africa-India route remained steady at $14.8/dmt. Market participants cited subdued demand and muted buying sentiment, keeping freight levels capped despite steady vessel availability.

Outlook

The Indian coal market remains directionless as muted industrial activity and cyclone-related disruptions offset recent price gains. With sponge production cuts and subdued demand from the manufacturing sector, near-term trade momentum is likely to remain slow. Portside offers are expected to stay rangebound until clearer demand cues emerge in November, supported by stabilising weather and improved logistics.

Leave a Reply