- Trading activity improves on expected mill price hikes

- Propane, RLNG supply concerns may impact production

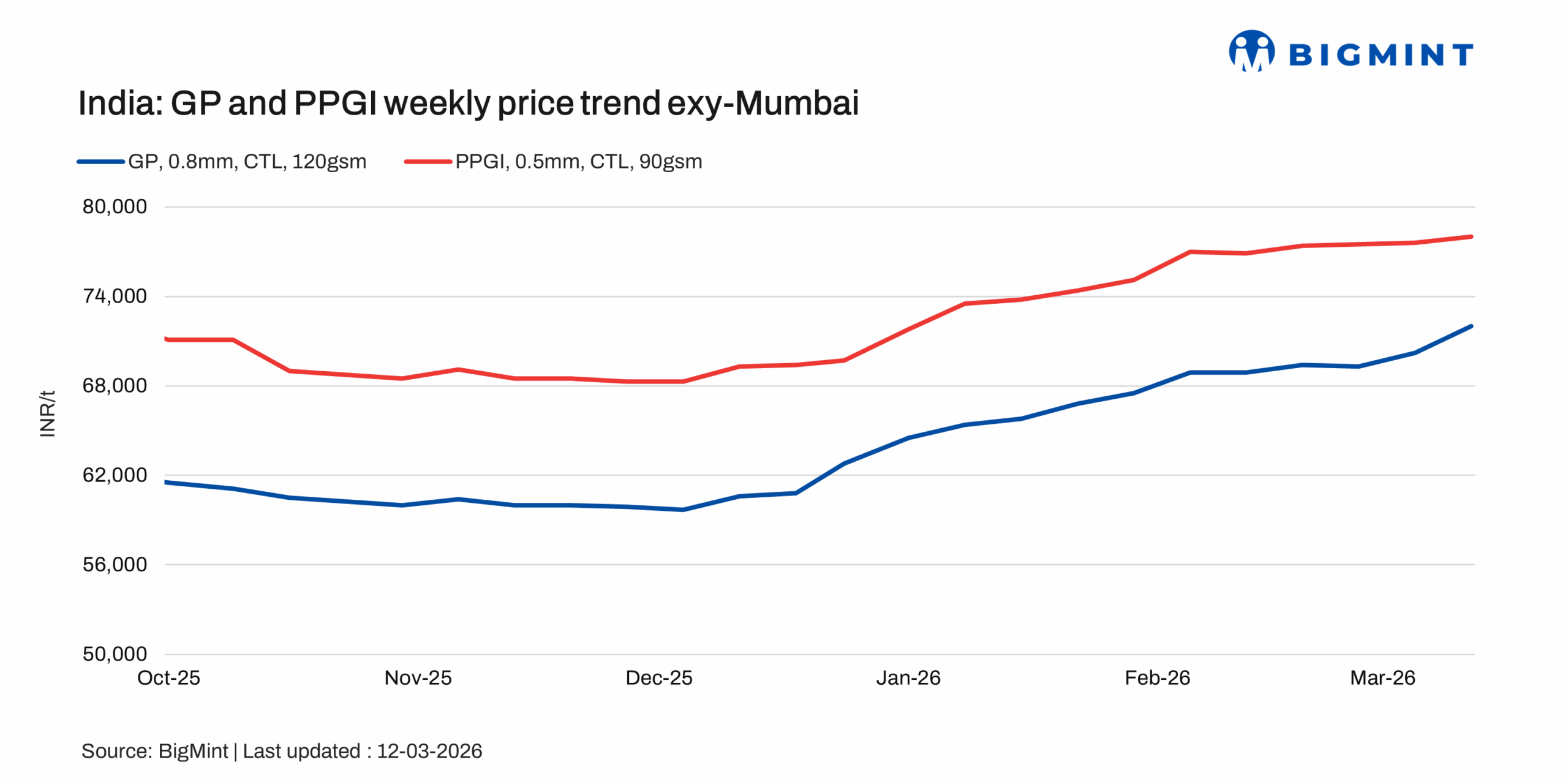

Indian coated flat steel prices moved up w-o-w across segments, supported by recent mill price hikes and tight supply conditions. Prices of galvanised plain (GP) increased by INR 600-1,800/t w-o-w, while pre-painted galvanised iron (PPGI) prices rose by INR 400-1,100/t. Galvalume (BGL) witnessed a sharper increase of INR 1,500-2,800/t during the same period.

Market participants attributed the upward movement primarily to recent list price revisions by mills and supply constraints in certain pockets. Although overall buying activity remained moderate, the market is gradually adjusting to higher price levels, and price absorption may improve in the coming week.

Additionally, mills are reportedly considering further price increases, citing rising uncertainty in global markets amid escalating geopolitical tensions linked to the Iran-Israel conflict, which could impact raw material costs, freight, and overall market sentiment.

Price update

GP coil prices increased by INR 1,800/t w-o-w to INR 72,000/t ($779/t) exy-Mumbai, compared with INR 70,200/t ($759/t) last week. Market offers were largely reported in the range of INR 71,500-72,500/t ($744-784/t), reflecting improved mill realisations despite moderately cautious trade sentiment.

PPGI prices also strengthened. Exy-Mumbai prices increased by INR 400/t w-o-w, with market offers largely heard in the range of INR 77,500-78,500/t ($838/t). Meanwhile, exy-Delhi prices saw a sharper rise of INR 1,100/t w-o-w to INR 77,600/t ($839/t), while market offers were reported in the range of INR 76,500-78,500/t ($828-849/t).

BGL prices recorded a notable increase. Exy-Mumbai prices rose by INR 1,500/t w-o-w to INR 82,700/t ($950/t), with market offers largely heard at INR 81,000–82,000/t ($876-887/t). In Faridabad, prices increased more sharply by INR 2,800/t w-o-w to INR 81,500/t ($882/t), with offers also reported around INR 81,000-82,000/t ($876-887/t), supported by relatively tight availability.

Market updates

Demand conditions showed moderate improvement during the assessment period, with trading activity picking up across markets. Market participants reported better buying momentum, largely driven by expectations of further mill price increases, which prompted traders and end-users to procure material in advance. As a result, near-term procurement activity strengthened and market sentiment improved marginally.

In the western and northern regions, buying interest remained relatively healthy, with improved enquiries and trading volumes. Participants indicated that a portion of the demand was speculative in nature, as buyers sought to secure material ahead of potential price hikes by mills.

However, market participants also highlighted growing concerns over raw material availability, particularly propane and RLNG (re-gasified liquefied natural gas). Propane gas availability was reported to be extremely limited, with market sources suggesting that, at current consumption levels, available supplies may last for only around two weeks.

Additionally, one of the major domestic mills has flagged concerns regarding potential disruptions in RLNG and propane supplies, which could impact plant operations and downstream production. Market participants are therefore closely monitoring the situation.

While demand has shown some improvement and trading activity has strengthened, participants noted that the market remains watchful of supply-side developments, particularly in relation to energy and gas availability, which may influence production levels and price trends in the coming weeks.

Raw material prices

Domestic zinc prices softened slightly during the assessment period. Zinc ingot (99.995%) prices were assessed at INR 3,34,000/t ($3,839/t) in the latest assessment, down by INR 2,000/t w-o-w from INR 3,36,000/t ($3,862/t) reported last week. Despite the marginal correction, zinc prices remain relatively elevated, continuing to provide cost support to coated flat steel prices.

At the trade level, flat steel prices in India strengthened across regions, with hot-rolled coil (HRC) prices reaching a 28-month high. Market assessments indicated HRC prices in the range of INR 53,000–56,200/t ($610–646/t), while cold-rolled coil (CRC) prices were heard at INR 58,100–63,500/t ($668–730/t) across major markets.

According to the latest bi-weekly benchmark assessment by BigMint, HRC (IS2062, Gr E250, 2.5–8 mm/CTL) prices increased by INR 1,000/t ($11/t) w-o-w to INR 55,500/t ($638/t) as of 10 March, compared with INR 54,500/t ($626/t) in the previous week.

Similarly, CRC (IS513, Gr O, 0.9 mm/CTL) prices were assessed at INR 61,500/t ($707/t), rising by INR 1,000/t ($11/t) w-o-w from INR 60,500/t ($695/t) in the previous assessment. These prices are ex-Mumbai for the distributor-to-dealer segment and exclude 18% GST.

Outlook

Market sentiment has turned firmer following recent price hikes, with improved trading activity driven by expectations of further mill-led increases. Major mills are also planning to raise coated flat steel prices by around INR 2,000-2,500/t in the upcoming round of revisions. In the near term, prices are likely to remain supported as the market adjusts to higher levels. Moreover, potential disruptions in propane and RLNG supplies could impact production and influence supply conditions, lifting prices further. The pace of demand and price absorption will remain key factors determining market direction in the coming weeks.

Leave a Reply