- Exports to Japan drop 24% m-o-m amid tepid steel demand

- Prices rise as weather, logistical constraints tighten supply

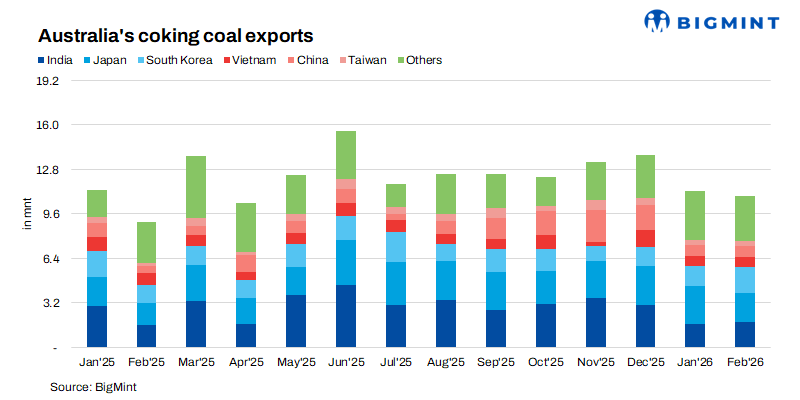

Australia’s coking coal exports stood at 10.89 million tonnes (mnt) in February 2026, registering a 2.9% m-o-m decline from 11.21 mnt in January. The marginal fall primarily reflected softer downstream steel demand across several Asian markets, coupled with seasonal production adjustments and weather-related logistical constraints that typically disrupt mining and port operations during the early part of the year.

Despite the monthly dip, exports remained 21.1% higher y-o-y, indicating that overall annual demand for Australian metallurgical coal remains relatively stable, supported by sustained blast furnace operations in major steel-producing economies.

Mixed import trends across key Asian buyers

Import demand across Asia displayed diverging trends, reflecting varied steel sector performance among key consuming nations.

India continued to be a major destination for Australian coking coal, with imports rising 8.1% m-o-m to 1.86 mnt, supported by steady procurement from domestic steelmakers and ongoing blast furnace utilisation.

In contrast, Japan’s imports declined sharply by 23.8% m-o-m to 2.05 mnt, amid continued steel production cuts and subdued domestic demand. Structural challenges in Japan’s industrial sector and slower manufacturing activity continued to weigh on raw material consumption.

China’s imports increased by 8% m-o-m to 0.81 mnt, although demand for Australian material remained relatively restrained. Policy-led supply adjustments, stricter import management, and weak steel sector activity limited buying interest. In addition, improved domestic coal availability and stronger inflows from Mongolia reduced reliance on Australian cargoes.

Meanwhile, South Korea recorded a notable 25.9% m-o-m increase in imports to 1.85 mnt, suggesting stronger blast furnace operations and possible restocking activity by steel producers.

Among smaller buyers, Taiwan’s imports declined 7.3% m-o-m to 0.38 mnt, while Vietnam registered a modest 1.4% m-o-m increase to 0.73 mnt, reflecting relatively steady steel production in the region.

Overall, the regional demand landscape pointed to uneven steel sector momentum, with several markets experiencing demand moderation at the beginning of the year.

Port-wise shipment trends show varied performance

Export performance across major Australian coal terminals showed mixed operational trends during the month.

Shipments through Dalrymple Bay Coal Terminal (DBCT) increased 20.6% m-o-m to 3.69 mnt, while Hay Point recorded a 3.2% m-o-m rise to 2.57 mnt, indicating improved loading activity at these key terminals.

In contrast, Abbot Point exports declined 12.2% m-o-m to 0.79 mnt, reflecting weaker shipment volumes. Similarly, Gladstone experienced a 19% m-o-m fall to 3.7 mnt, suggesting reduced vessel loading and operational slowdowns during the month.

Among smaller terminals, Port Kembla and Newcastle handled 0.08 mnt and 0.06 mnt, respectively.

Coking coal prices strengthen amid supply constraints

Australian coking coal prices firmed in February, increasing by approximately $14/t m-o-m compared with January levels. The price recovery was primarily supported by supply-side disruptions that tightened spot availability in the market.

Seasonal weather disturbances and logistical bottlenecks impacted mining and port operations, restricting cargo availability and lending upward support to prices. This occurred despite relatively subdued steel demand across several key importing regions.

Outlook

Australian coking coal exports are expected to remain stable, supported by steady demand from India and South Korea, though weaker steel activity in Japan and China may limit growth. Improved weather and smoother port operations could aid shipments, while price trends will depend on steel production levels and spot market supply.

Leave a Reply