- Chinese iron ore prices surge on pre-Golden Week restocking

- Indian coking coal tags firm amid Australian supply concerns

- Chinese HRC exporters slash offers amid regulatory worries

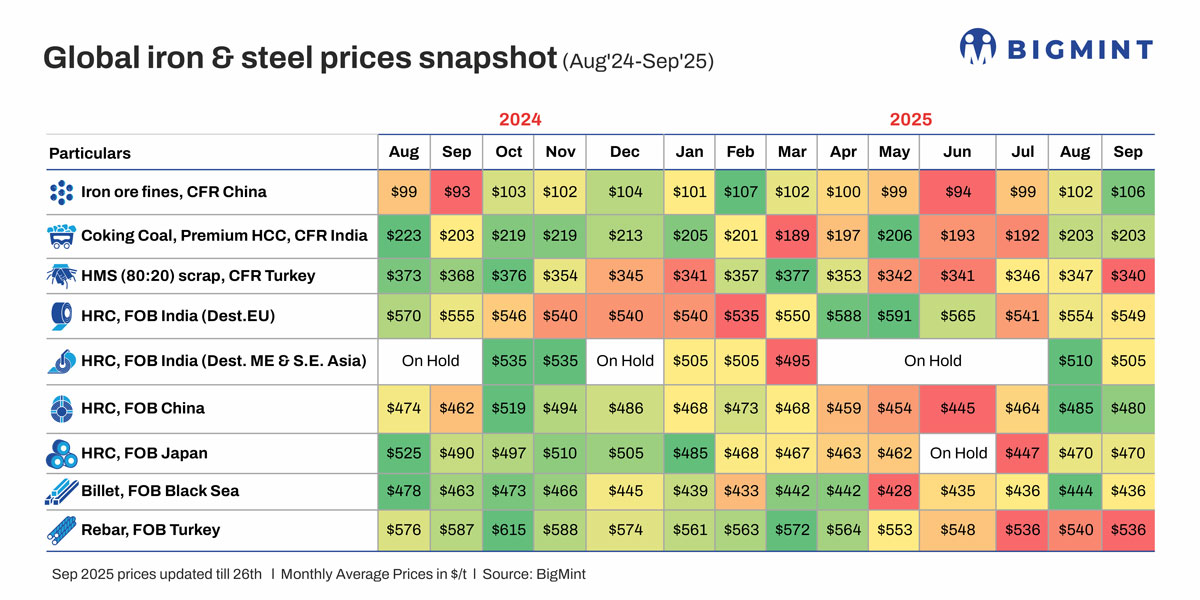

Morning Brief: Global steel and raw material prices declined for the most part in September 2025, with Chinese iron ore fines (up $4/t m-o-m), Indian imported coking coal (stable m-o-m), and Japanese hot-rolled coils (HRCs) (stable m-o-m) being the few exceptions.

Overall, for most finished steel commodities, markets witnessed sluggish offtake, which led to the downtrend in pricing last month. Trade protectionist measures kept buyers in a guarded mode, while competitive export pricing from China continued to capture demand.

Snapshots of price movements in Sep’25

Chinese iron ore fines surge on restocking interest: Chinese iron ore fines (Fe 62%) prices increased by $4/tonne (t) m-o-m to a monthly average of $106/tonne (t) CFR in September. At the beginning of the month, positive sentiment, such as the anti-involution policy, pushed prices higher, with medium-grade fines attracting robust interest, while tight margins led mills to avoid costly high-grade ore.

Additionally, towards the month-end, ahead of the Golden Week holidays (1-8 September), demand improved on mill’s restocking spree. However, the rebound in trade was weaker than expected, given the continuing debt crisis in the real estate segment.

Imported coking coal remains flat in India amid weak demand: Premium hard coking coal (PHCC), CFR India, prices remained stable m-o-m at $203/t. Australian FOB prices were at a monthly average of $187/t, a marginal $1/t increase compared to $186/t. Prices were supported by high Chinese domestic coal tags and supply concerns in Queensland, including BMA’s planned Saraji mine shutdown.

However, weak demand, a monsoon-led steel slowdown, and ample supply prevented any price gains.

Turkish imported scrap slides amid weak steel offtake: Imported HMS 80:20 prices into Turkiye dropped by $7/t m-o-m to $340/t CFR, with weak steel sales in the summer, both locally and overseas, fostering cautious sentiment. Soft collection rates also made EU-origin cargoes cheaper, while rising freight costs and currency fluctuations weighed on demand.

While prices rebounded in the final week, supported by tighter supply, rising freight, and October bookings, the hike was not enough to offset the price corrections earlier in the month.

Indian HRC offers to EU drop on CBAM pressures: BigMint’s India HRC export index for the EU eroded by $5/t m-o-m to $549/t FOB amid cautious sentiment due to the Carbon Border Adjustment Mechanism (CBAM), which is due to take effect from January 2026.

Buyers stayed on the sidelines due to uncertainty regarding the tax liabilities under the CBAM regime and risks of potential new safeguard measures being implemented. Indian mills also pushed to complete their export quotas because of the CBAM factor. Additionally, sufficient supply and weak end-user demand kept prices on a downward trajectory.

Indian HRC offers to Middle East, SE Asia slip: Indian mills’ HRC offers to the Middle East and Southeast Asia declined by $5/t m-o-m to $505/t in September. CFR values for the Middle East ranged within $530-540/t, generating a muted response from buyers. Meanwhile, following a recovery in domestic demand in Vietnam, Indian HRC export offers to the country resumed at $505-515/t CFR Ho Chi Minh City (HCMC), but besides a 30,000-t deal, trading activity has been limited due to competitive Chinese offers ($495/t CFR HCMC).

Chinese exporters trim HRC offers amid regulatory concerns: China’s HRC export offers also dropped by $5/t m-o-m to $480/t FOB, as demand weakened. Authorities in Vietnam, where certain sizes of Chinese HRCs face an anti-dumping duty, reportedly accepted an application to investigate whether Chinese exporters are circumventing the duties by ramping up shipments of wider-width coils. Notably, Vietnam is the single-largest destination for Chinese steel exports.

Additionally, the imminent implementation of stricter export checks from 1 October, aimed at combating tax evasion, likely led to an urgency to ship material, while buyers remained cautious about procuring material amid a lack of clarity regarding the implications of the new norms.

However, strong raw material prices helped cap the decline.

Stagnant demand keeps Japanese HRC export offers stable: Japanese HRC export offers remained stable m-o-m at $470/t m-o-m, as weak demand continued to batter prices. Overall, Japanese HRC export volumes dropped by around 7% y-o-y in January-August 2025.

Subdued demand weighs on Black Sea billet prices: CIS-origin billet prices slid by a sharp $8/t m-o-m to $436/t FOB Black Sea in September amid currency depreciation, subdued demand from Turkiye due to limited interest in rebar exports, and competitive pricing by Ukrainian sellers. Additionally, the decline in scrap prices also reduced cost support, while Egypt’s imposition of provisional safeguard duties (16.2% ad valorem) on billet imports impacted demand.

Turkish rebar prices slip amid weak demand cues: Turkish rebar export prices slipped by $4/t m-o-m to $536/t FOB, as demand remained soft in key markets amid bearish global sentiment. Even domestic demand failed to provide a cushion, with the Turkish central bank’s interest rate cuts unsuccessful in boosting procurement, mills’ capacity utilisation rates remaining low, and liquidity shortages besetting the market. However, rising costs of scrap — due to higher freights — limited the price correction to a certain degree.

Outlook

Global steel and raw material prices may remain subdued in the near term, with some brief spikes. Although iron ore demand in China is set to sustain, prices may trend lower due to sufficient market supply, ample inventories with buyers following pre-Golden Week restocking, and tepid steel demand.

Meanwhile, coking coal could rise on tight supply and increased procurement by Indian mills, with expectations of a post-festive season demand pick-up expected to boost production enthusiasm. On the other hand, tight supply may keep Turkish scrap prices firm.

As for HRCs, the absence of China from the global market during the Golden Week holidays may encourage procurement from other origins. The Chinese government’s attempts to prune output may also support pricing, but so far, there has been limited concrete progress on this front. As such, with demand remaining cool and inventories elevated, pricing worries may continue for global exporters.

Leave a Reply