- Tariff cuts, QCO shifts accelerate India’s scrap pivot

- Domestic deficit of 0.45-0.55 mnt sustains import reliance

- Rising demand driving domestic smelting, processing capacity expansion

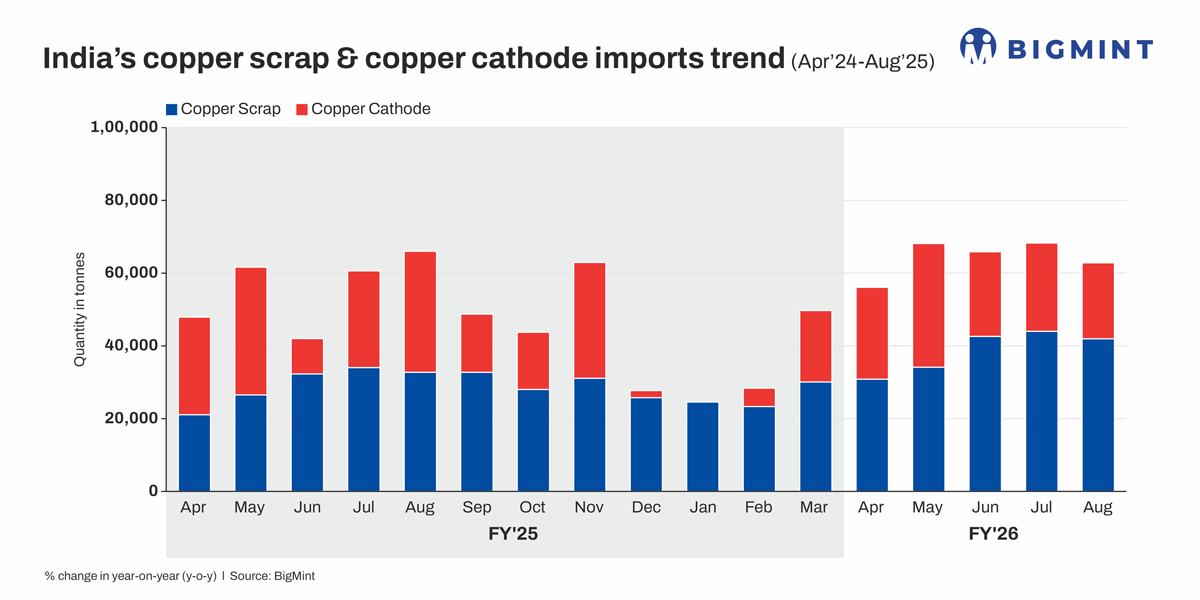

Morning Brief: India’s copper trade in the first five months of FY’26 reflects a decisive shift toward scrap, underpinned by policy changes, higher global prices, and domestic supply gap. Scrap imports climbed 32% y-o-y to 193,525 tonnes (t) in April-August 2025 compared with 146,707 t a year earlier. The m-o-m inflows also showed strong momentum, rising from 21,058 t in April 2024 to nearly 42,000 t in August 2025.In contrast, copper cathode imports fell 3% to 127,569 t over the same period, weighed down by regulatory bottlenecks and reduced cost competitiveness.

Why are buyers shifting from cathode to scrap?

LME copper averaged $9,800-10,200/t between June and August, almost 12% higher than last year. Elevated international prices squeezed cathode affordability, widening the spread between refined cathodes and scrap. Buyers, especially secondary smelters and wire rod producers, increasingly opted for scrap as a cheaper and more flexible input. This substitution effect was most visible during the June-August window, when cathode inflows slowed and scrap shipments surged to fill the gap.

On the domestic front, MCX copper averaged INR 908/kg between June and August, up about 11% from an average of INR 818/kg in the same period of 2024.

The government’s Quality Control Order (QCO) has been a significant drag on cathode imports. The requirement for BIS certification on refined copper has led to approval delays, cargo clearance bottlenecks, and higher compliance costs. Importers report that the process added both time and expense to cathode shipments, creating volatility in supply during peak demand months. Scrap, by contrast, is not subject to the same regulations, giving it a structural advantage as a feedstock.

Tariff advantage for scrap

Scrap also benefits from a favourable tariff regime. The reduction of import duty from 5% to 2.5% in 2021, along with Budget 2025 discussions to potentially eliminate the concessional duty, has lowered procurement costs. This policy backdrop, coupled with ready availability from the Middle East and US, has accelerated India’s pivot to secondary raw materials.

Domestic supply-consumption scenario

On the supply side, India remains structurally short of refined copper. Hindalco’s Dahej smelter accounts for the bulk of output, while Hindustan Copper and Vedanta add smaller volumes. Even so, total domestic refined copper capacity of about 1 million tonnes (mnt) annually falls well short of demand, leaving a persistent deficit of 0.45-0.55 mnt.

The Adani Kutch smelter project, once operational, is expected to partly bridge this gap, but in the near term, scrap imports remain the most reliable cushion against shortages.

Demand has been robust across end-use industries. The electrical sector continues to lead consumption, supported by grid expansion and transmission upgrades. Infrastructure spending ahead of the monsoon boosted procurement in Q1FY’26, while the automotive and EV sectors added incremental demand.

Cable and wire rod manufacturers in Gujarat and Maharashtra have scaled up capacity, sourcing a higher share of raw materials through imported scrap. Smaller recyclers and mid-tier processors are also expanding sorting and pretreatment infrastructure to align with BIS norms and meet the rising demand for quality-assured scrap.

Upcoming expansions in India

JSW Group is planning a 0.5 mnt per annum copper smelter in Odisha by 2028-29, with aspirations to scale to 1 mnt by 2033-34.

Hindalco under the Aditya Birla Group has committed INR 45,000 crore over the next three to four years across its aluminium, copper, and speciality alumina businesses, including new copper recycling plants and downstream product lines.

Adani and MetTube have entered into a JV to boost domestic copper tube production for use in air-conditioning, renewable energy, and smart construction applications. Precision Wires India is investing INR 33 crore to expand copper rod manufacturing capacity at its Zaroli and Valvada plants.

Outlook

India’s copper demand is projected to rise to 3-3.3 mnt by 2030, nearly double that of current levels. Domestic scrap generation is expected to remain limited at 430,000-530,000 t annually, keeping the country reliant on imports for both scrap and refined copper. With mine supply risks in Chile, Peru, and potentially Indonesia, scrap’s role is likely to strengthen further.

At the same time, rising demand will push refiners and manufacturers to expand domestic smelting and processing capacity, as seen with Adani’s Kutch expansion and Hindustan Copper’s mine development plans.

In the near term, scrap imports are expected to remain elevated through FY’26, supported by policy advantage, price spreads, and robust consumption. Cathode inflows, meanwhile, will continue to face headwinds from QCO compliance and elevated global copper prices.

Leave a Reply