- Operations at Grasberg mine suspended after safety issues

- Falling LME stocks, China’s steady imports support prices

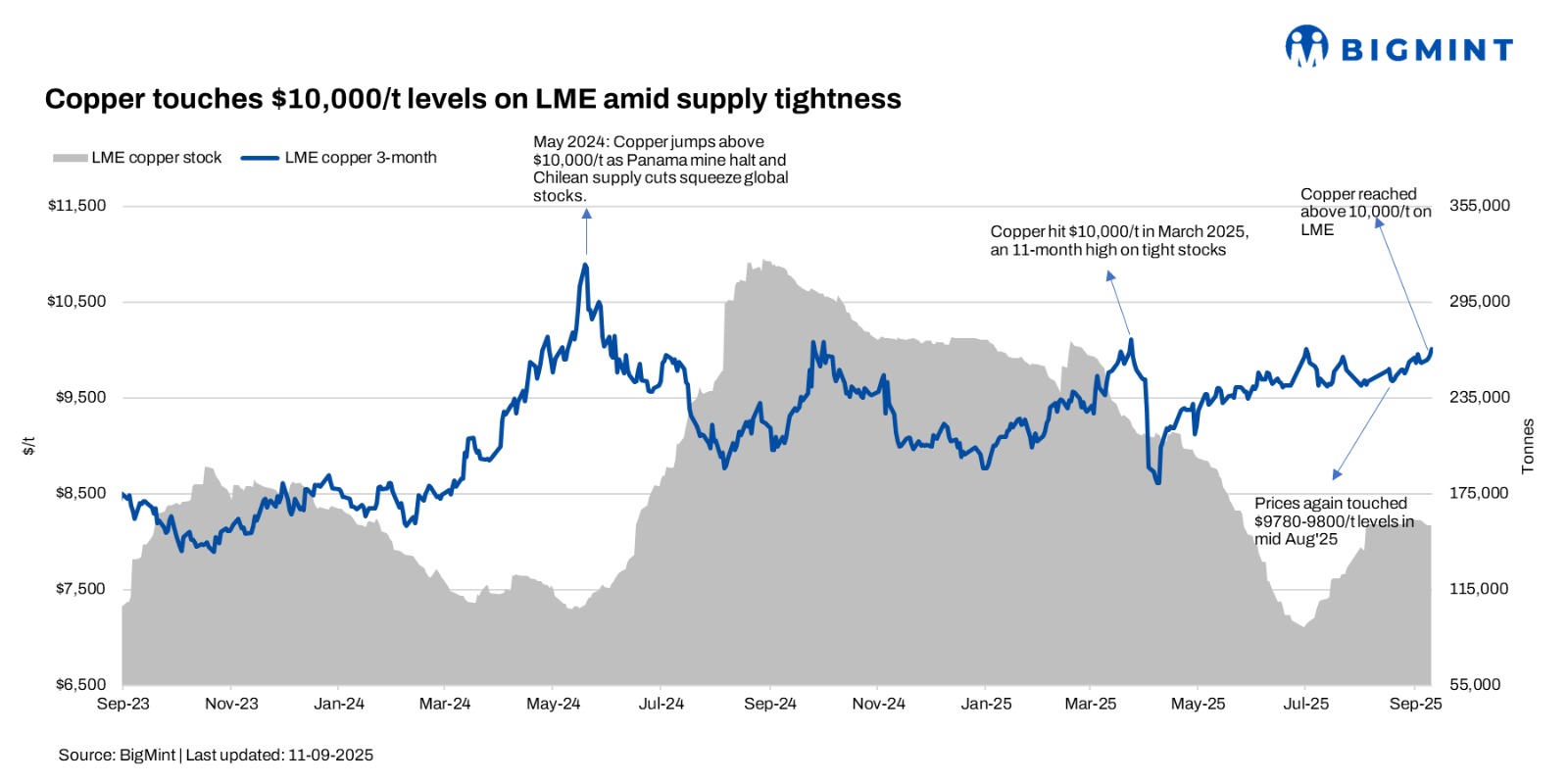

Copper prices on the London Metal Exchange (LME) climbed past $10,000/tonne (t) this week, as supply worries intensified. The immediate trigger came from Freeport-McMoRan’s Grasberg mine in Indonesia, where operations were suspended after safety issues forced worker evacuations. Grasberg is one of the world’s largest copper mines, so the halt quickly rattled markets.

At the same time, LME inventories fell to 155,050 t on 10 September, from 157,950 t a week earlier. Cancelled warrants, especially in South Korea, signalled that more metal was leaving warehouses, leaving buyers scrambling for supply.

Demand factors also added support. China’s steady imports, a weaker US dollar, and expectations of US interest rate cuts boosted copper’s investment appeal. Producer price data also pointed to healthy industrial demand.

On the balance side, the global copper surplus shrank sharply — to just 36,000 t in June compared to 79,000 t in May. In the first half of 2025, the surplus was 251,000 t, down from 395,000 t a year earlier. This shows supply and demand are moving closer to balance.

W-o-w, LME cash copper eased slightly to $9,847/t on 10 September, versus $9,881/t a week earlier. Still, with falling stocks and mine disruptions, the market remains tight.

Outlook

In the short term, copper prices are expected to remain firm above the $10,000/t mark as mine disruptions and falling LME inventories tighten supply. The suspension at Freeport-McMoRan’s Grasberg mine has intensified fears of further shortages, while cancelled warrants and lower stock levels highlight persistent market tightness. On the demand side, steady Chinese buying, a softer US dollar, and expectations of US rate cuts are providing additional support.

Analysts, including Goldman Sachs and JP Morgan, note that while prices may show volatility, the balance of risks in the coming weeks tilts toward continued strength, with supply shocks likely to keep the market elevated.

The Federal Open Market Committee (FOMC), which decides whether to cut interest rates, is scheduled to be held on the 16th and 17th of next week. If the expectation of interest rate cuts recedes by then, there is a high possibility that the upside will turn around and the upside will become heavier. Whether it will be a factored scenario will attract market attention, especially speculators.

Leave a Reply