Chinese prices of metallurgical coke will likely ease further over the first half of April 2024 and then hold steady or even increase moderately during the remainder of the month, Mysteel suggested in its monthly outlook report.

The prediction takes account of the light buying interest for feed coke among steel producers, most of whom were now maintaining low feed stocks to mitigate their risks and sustain their current profitability now that steel margins have risen slightly, the report said.

The margins of Chinese steelmakers have improved recently following the mills’ success last month at persuading independent coke producers to accept three successive selling price cuts totalling Rmb 300-330/t ($41.5-45.6/t), as reported. This also meant that those Chinese steelmakers without inhouse coking facilities have won no fewer than seven price reductions from the met coke sellers so far this year.

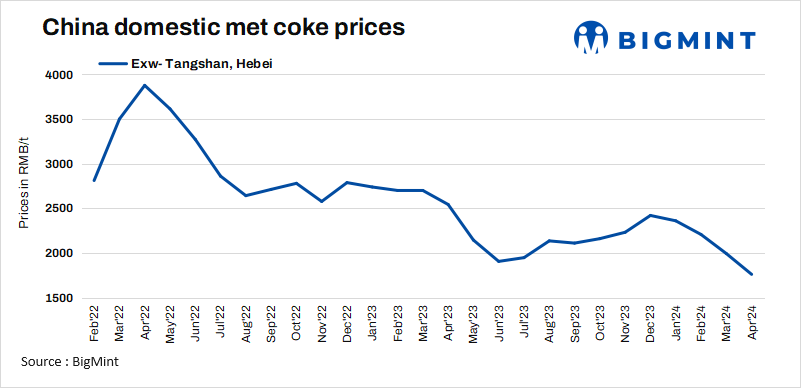

Consequently, as of 1 April, China’s national composite coke price under Mysteel’s assessment had plunged by a significant Yuan 304/t on month to Rmb 1,789.9/t including the 13% VAT.

The report raised the possibility of leading mills seeking an eighth price reduction this week, with the mills likely to argue this was needed to alleviate some of the cost pressure they’re suffering from the sluggish performance of finished steel prices.

Should the coke producers concede again, the report remarked that coke prices might stabilise briefly or even climb moderately in the latter half of the month, driven by an uptick in coke demand from domestic steelmakers. This aligned with expectations for a rise in hot metal output among these steel firms, though the increase might not be very large, the report said.

In fact, since late March some domestic steel mills have started lifting steel production in response to the steady declines in prices of steelmaking raw materials, though the pace of the rise remained slow. Nonetheless, the strategy has prompted them to procure enough coke to meet their additional production needs, Mysteel Global noted from the report.

For example, Mysteel’s survey among 247 Chinese steel mills showed that they produced 2.21 mnt/day of hot metal on average as of 28 March, higher than 0.2% compared to two weeks earlier.

The report suggested that output at these sampled mills could increase further to 2.26-2.3 mnt/day on average in April, potentially boosting their demand for coke accordingly.

In terms of coke availability, domestic coke supply declined steeply last month and may remain stable at low levels for the rest of this month. This was largely attributed to the fact that most coke producers across the country had trimmed production to avoid deeper losses.

For example, Mysteel’s parallel survey conducted among 30 merchant coke producers nationwide showed that as of 28 March, these coke makers were losing a large Rmb 155 on average on every tonne of met coke they sold, much larger than the losses observed in January-February.

In general, although the domestic coke market still faces some downward pressure, the decline in prices will not be so significant as the demand for coke among steelmakers mills could gradually improve, according to the report. It also noted that Chinese coke prices may even enjoy a mild rebound by month-end if the gain in steel output exceeds forecasts.

Note: This article has been written in accordance with an article exchange agreement between Mysteel and BigMint.